Thursday Jul 16, 2026

Thursday Jul 16, 2026

Monday, 26 August 2019 00:56 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

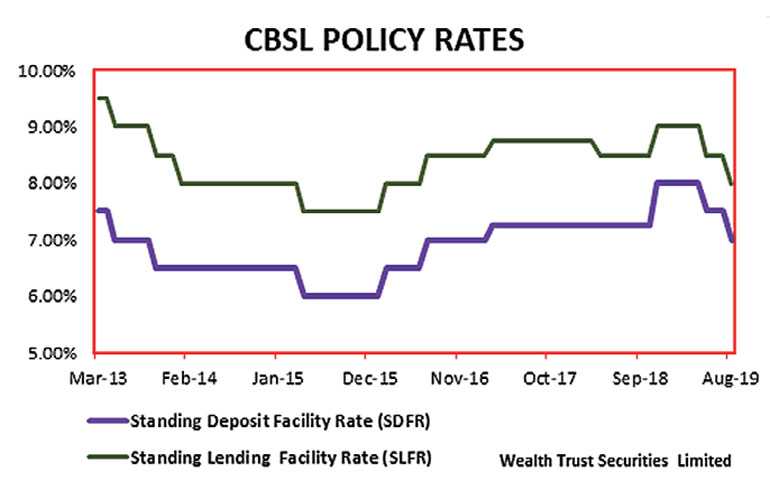

The Central Bank of Sri Lanka was seen reducing its policy rates by 50 basis points at its fifth monetary policy announcement on 23 August, recording its second policy cut for the year 2019 following the cut of 50 basis points in May 2019.

The new Standing Deposit Facility Rate (SDFR) and Standing Lending Facility Rate (SLFR) stand at 7% and 8% respectively.

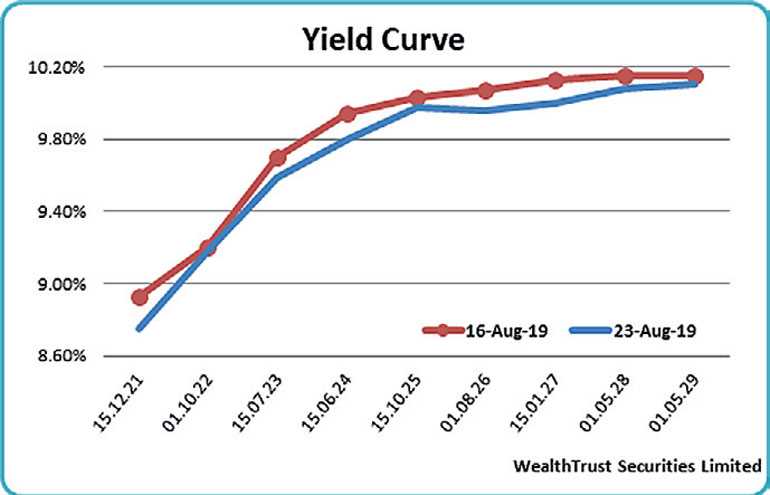

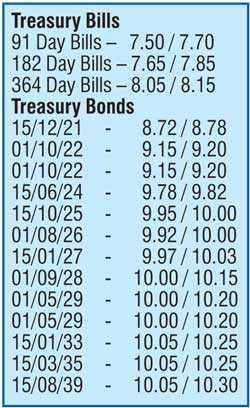

In the secondary bond market, yields were seen seesawing during the week ending 23 August as continued selling interest during the early part of the week saw yields increasing on the liquid maturities of 2021s (i.e. 01.08.21, 15.10.21 and 15.12.21), 2023s (i.e. 15.07.23 & 15.12.23), 2024s (i.e. 15.03.24 and 15.06.24) and 15.01.27 to intraweek highs of 9.15%, 9.00%, 9.20%, 9.85%, 9.90%, 10.02%, 10.04% and 10.22% respectively.

The upward momentum was further supported by the weekly Treasury bill auction results, where weighted averages increased across all three maturities. Nevertheless, buying interest subsequent to the monetary policy announcement saw yields decreasing once again with said maturities hitting lows of 8.70%, 8.75% each, 9.50%, 9.65%, 9.80%, 9.72% and 10.00% respectively on the back of local buying interest reflecting a parallel shift downwards of the overall yield curve on week on week basis.

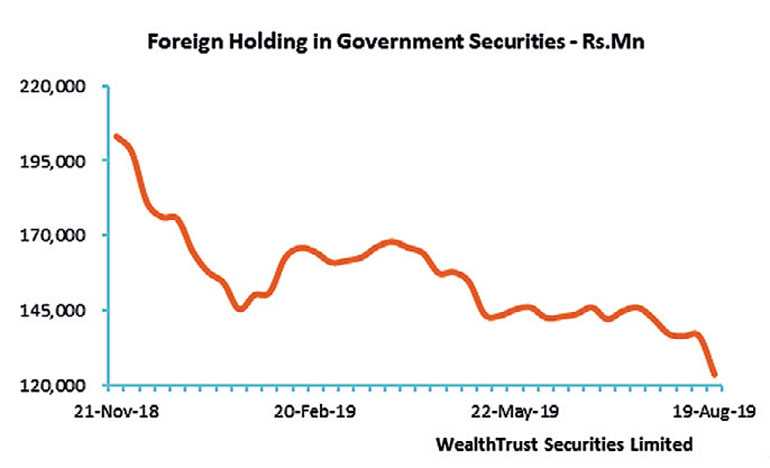

The foreign holding in rupee bonds recorded its sharpest decline in 37 weeks with an outflow of Rs. 12.87 billion for the week ending 21 August, a level last witnessed on 5 December 2018.

The daily secondary market Treasury bond/bills transacted volume for the first four days of the week averaged Rs. 11.81 billion.

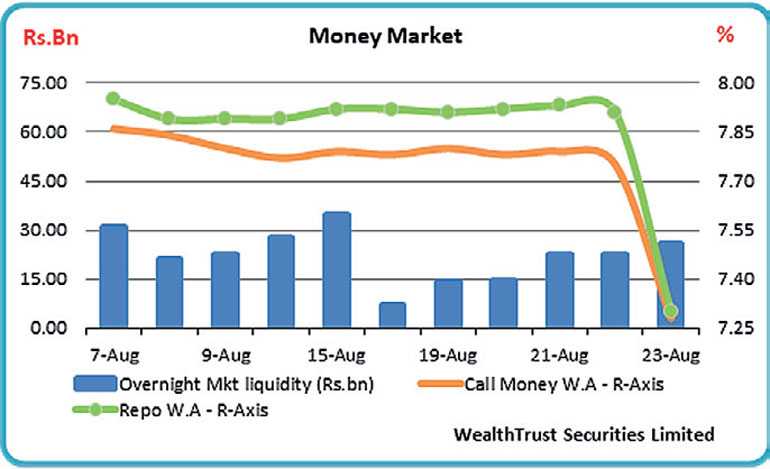

In money markets, the base rate change saw overnight call money and repo rates decreasing to average at 7.28% and 7.30% respectively on Friday against its initial four days average of 7.78% and 7.92%.

The Central Bank’s OMO department was seen infusing liquidity throughout the week by way of overnight and seven day reverse repo auctions at weighted averages of 7.31% to 7.75% as the total liquidity in the system stood at a deficit of Rs. 9.15 billion.

Furthermore, a total of Rs. 6.08 billion was injected during the week by way of outright purchases of Treasury Bills for durations ranging from 220 to 325 days at weighted averages ranging from 7.81% to 8.00% as well.

Downward trend in rupee continues

The rupee on spot contracts were seen dipping considerably to a low of Rs. 180.10 for the first time since February 2019 against its previous week’s closing levels of Rs. 177.15/25 on the back of imported demand and foreign selling in rupee bonds before bouncing back to close the week at Rs. 179.70.

The daily USD/LKR average traded volume for the first four days of the week stood at $ 72.80 million.

Some of the forward dollar rates that prevailed in the market were: one month – 180.20/50; three months – 181.00/40; and six months – 182.40/80.