Saturday Jun 06, 2026

Saturday Jun 06, 2026

Monday, 11 June 2018 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary bond market remained active during the week ending 8 June, with yields initially decreasing during the early part of the week and increasing once again towards the latter part of the week.

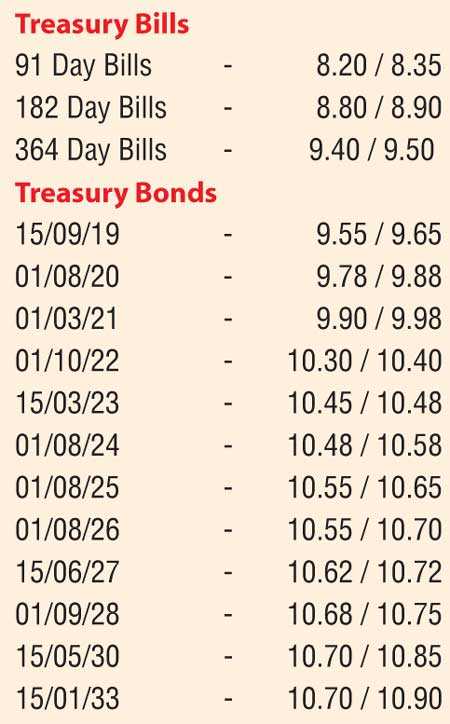

The yields of the liquid maturities of 15.03.23 and 01.09.28 were seen decreasing to weekly lows of 10.35% and 10.60%, respectively, against its previous weeks closing levels of 10.38/42 and 10.58/65. This downward trend was well-supported by the considerable decrease in the weighted average yield of the 364-day Treasury bill by 13 basis points to 9.49% at the weekly bill auction.

However, selling interest coupled with profit-taking resulted in yields increasing once again towards the latter part of the week to hit highs of 10.50% and 10.75%, respectively, to close the week marginally higher against its previous week’s closings. Activity was also witnessed of the 2019, 2021, 2024 and 2025 maturities within the range of 9.50% to 9.69%, 9.90% to 10.15% 10.47% to 10.54%, and 10.59% to 10.63%, respectively. In the secondary bill market, February, March, April and May 2019 bills were seen changing hands within the range of 9.20% to 9.54%.

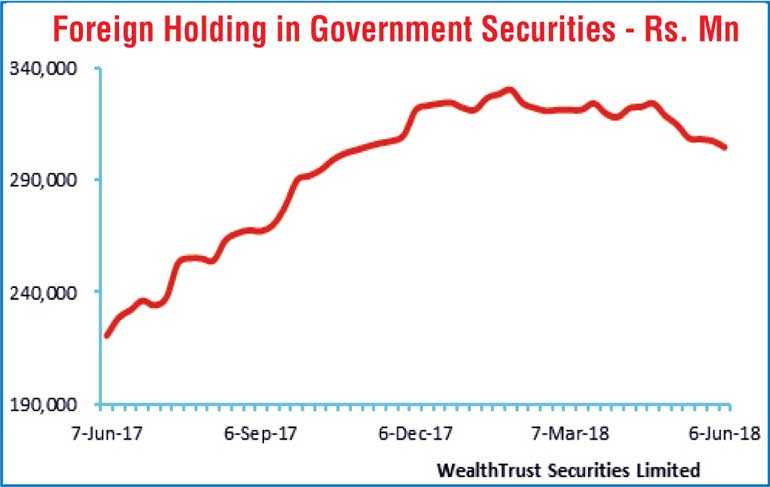

The foreign component in Rupee bonds was seen declining for a sixth consecutive week to record an outflow of Rs. 2.83 billion for the week ending 6 June. The daily secondary market Treasury bond/bill transacted volumes for the first four days of the week averaged Rs. 8.59 billion. In money markets, the OMO Department of the Central Bank was seen conducting overnight reverse repo auctions throughout the week in order to infuse liquidity at weighted average ranging from 8.47% to 8.50% as the net liquidity shortfall in the system increased to average Rs. 13.74 billion for the week against its previous week’s net shortfall of Rs. 3.87 billion. The overnight call money and repo rates averaged 8.08% and 8.12%, respectively, for the week.

The downward trend in the rupee continued for a third consecutive week as its spot contracts were seen closing the week at Rs. 158.95/10 against its previous weeks closing of Rs. 158.55/70 on the back of continued importer demand and limited export conversions.

The daily USD/LKR average traded volume for the first four days of the week stood at $ 54.01 million.

Some of the forward dollar rates that prevailed in the market were 1 Month - 159.70/90; 3 Months - 161.30/50 and 6 Months - 163.60/80.