Tuesday Jun 30, 2026

Tuesday Jun 30, 2026

Monday, 2 May 2022 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

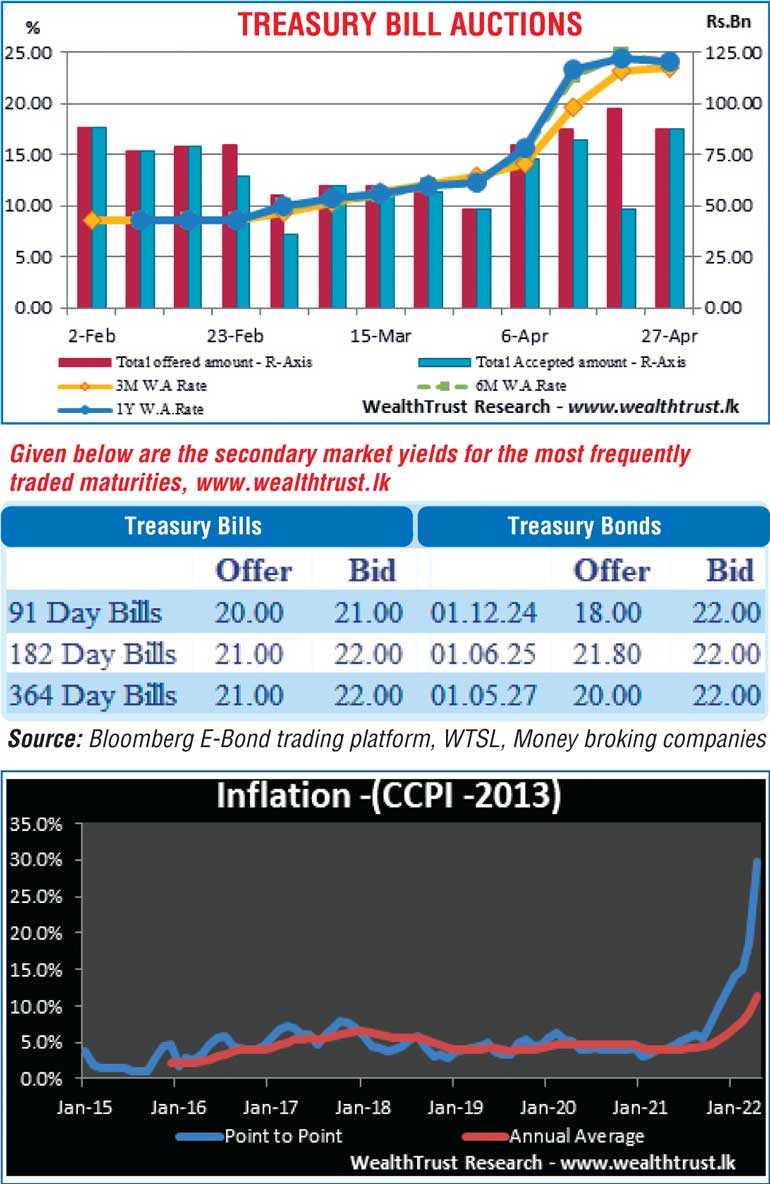

The T-bills and T-bond auctions conducted during the week ending 29 April 2022 produced inspiring outcomes while the recorded weighted averages led to an inversion of the yield curve.

The increased demand at the weekly Treasury bill auction saw its total offered amount fully subscribed for the first time in four weeks while the weighted average rates on the 182 day and 364-day maturities decreased for the first time in nine weeks.

The total accepted amount at the Treasury bond auctions increased as well, to its highest level over the past six rounds of auctions while the recorded weighted averages on the three year and five-year maturities led to the short end of the yield curve inverting as it was below the weighted averages of the three months to one-year bills.

Nevertheless, activity in the secondary bond market remained sluggish during the week as most market participants continued to be on the sidelines. The limited activity was witnessed on the very short-term maturities of 01.10.22 and 15.03.23 at levels of 25.00% to 25.15% while June, July 2022 and April 2023 maturities changed hands at levels of 18.00%, 21.00% to 22.00% and 22.00% to 22.10% respectively in the secondary bill market.

The Colombo Consumer Price Index (CCPI; Base 2013=100) for the month of April increased sharply to an all-time high of 29.8% on its point to point against its previous month’s figure of 18.7%. The annual average also increased to 11.3% against 9.1%.

This was ahead of Wednesday’s bill auction, where a total volume of Rs. 97.5 billion will be on offer, consisting of Rs. 40 billion on the 91 day, Rs. 30 billion on the 182 day and Rs. 27.5 billion on the 364 day maturities.

The foreign holding in rupee bonds remained unchanged at Rs. 2.71 billion for the week ending 27 April while the daily secondary market Treasury bond/bill transacted volumes for the first four trading days of the week averaged Rs. 20.39 billion. In money markets, the total outstanding liquidity deficit increased to Rs. 722.61 billion by the end of the week against its previous weeks of Rs. 709.11 billion while CBSL’s holding of Gov. Security’s stood at Rs. 1,864.60 billion against its previous weeks of Rs. 1,870.65 billion.

The Domestic Operations Department (DOD) of Central Bank was seen injecting liquidity by way of 14 day and 22 day reverse repo auctions at weighted average rates of 20.57% and 22.10% respectively.

The weighted average rates on call money and repo stood at 14.50% each.

Forex Market

In Forex markets, the USD/LKR rate on cash contracts traded at a level of Rs. 346.60 to Rs. 367.00 during the week while overall activity remained moderated.

The daily USD/LKR average traded volume for the four trading days of the week stood at $ 16.79 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)