Thursday May 28, 2026

Thursday May 28, 2026

Wednesday, 5 February 2020 00:25 - - {{hitsCtrl.values.hits}}

Alpen Capital (ME) Ltd., Dubai-headquartered investment banking advisory firm, announced the publication of its latest report titled ‘Sri Lankan Banking and NBFI Sector’. This report provides a comprehensive overview of the Sri Lankan Banking and Non-Banking Financial Institutions (NBFI) sectors, highlighting the strengths, opportunities and challenges for a diverse group of investors (investment funds, corporate institutions, etc.) looking for investment opportunities in Sri Lanka. It also profiles some of the key firms within these sectors.

“Alpen Capital forayed into Sri Lanka in 2015 and since then witnessed remarkable success, in both of its equity and debt advisory services, arranging more than $ 500 million of bilateral loans, club loans and syndications for banks and finance companies as well as advising clients on regional cross border mergers and acquisitions. We continue to believe in the tremendous growth potential of the country and anticipate immense opportunities for investors,” said Alpen Capital Executive Chairman Rohit Walia.

The Central Bank of Sri Lanka is closely monitoring the Banking and NBFI sector by adopting international regulatory standards, which has increased investors’ confidence in these sectors. Highly professional individuals who manage the banks and top-tier NBFIs have ably led the sector through challenging times and successfully fulfilled the expectations of investors. We expect the outlook of these sectors to improve and through this report intend to showcase them,” Alpen Capital Senior Director Dilip Samanthilaka said.

Sri Lanka’s economic growth which has seen a slowdown in recent years due to external factors is expected to improve as a result of easing of monetary policy by the Central Bank as well as fiscal expansion. IMF has projected real GDP growth to strengthen to 3.5% in 2020.

External vulnerabilities in meeting large external debt service payments have been foremost among Sri Lanka’s economic challenges. Despite the downgrade in sovereign ratings, Sri Lanka has retained the ability to raise sovereign bonds and raised them twice in 2019, with both bond issuances being healthily oversubscribed. Sri Lanka has managed to maintain inflows of around $ 1-2 billion over the last few years.

The country retained stable fundamentals despite economic challenges in the recent past. Growth was driven by an increasingly important services sector, and achieved relatively high-levels of GDP per capita.

Banking sector

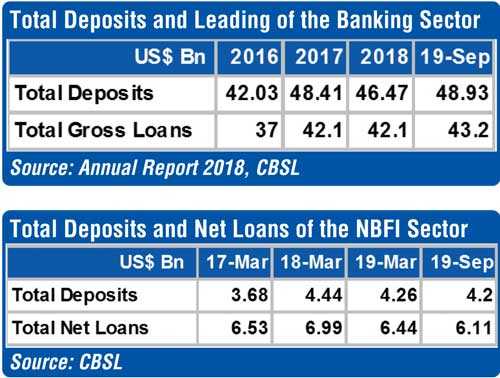

Licensed Commercial Banks (LCBs), which represent a major component of the banking system, had a total asset base of $ 58 billion and asset share of 87.6% as at September 2019.

In 2019, Year-on-Year (YoY) growth in credit to the private sector decelerated significantly to 4.4% from 16.2% in the previous year. However, lending rates at financial institutions remained at an elevated level over the period. To tackle this, the CBSL has reduced policy rates and imposed a cap on bank lending rates in September 2019. As a result of CBSL’s action as well as the government stimulus measures, the CBSL expects credit growth to gradually recover in 2020.

The CBSL has initiated drafting a new Banking Act to be enacted in 2021. The Act will look into areas of strengthening the governance of banks as well as regulations related to digitalisation of the sector.

The sector has adopted internationally accepted BASEL III regulatory framework and SLFRS 9 – the Sri Lankan equivalent of IFRS 9, pertaining to the accounting of loan losses. These measures will enhance resilience against headwinds in the future.

The banking sector has immense growth opportunities in different segments. Amongst them is the adoption of technology to provide digital financial services to their customers as well as attract a strong client base. A high yielding SME segment presents diversification opportunities which can be a lucrative market for the sector. Additionally, as the valuations of the banking sector are currently low, it presents an attractive buying opportunity for investors, which would support banks in accumulating more capital.

Challenges

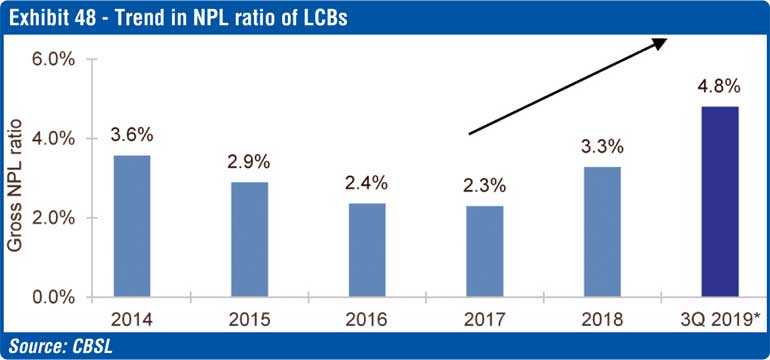

Rising Non-Performing Loans (NPLs) and impairment costs have eroded profits in 2019: Sluggish economic growth, lacklustre weather conditions in the form of droughts and floods during 2016 and 2017, political crises in late 2018, Easter Sunday attacks and slowdown in the construction and SME sectors, resulted in the gradual increase in NPL ratios from 2018. However, NPLs still remain much lower than some regional peers including Pakistan, Bangladesh and India.

Capital raising to meet regulatory requirements has proven to be challenging: Banks currently need much stronger capital buffers over the minimum ratios stipulated by the BASEL III international standard and additional directives by the CBSL.

Lending rate caps likely to exert pressure on margins: The recently announced caps on lending rates to drive credit growth in the economy could drive down industry interest margins in the medium term.

Catering to evolving customer needs and cyber security risks pose a challenge amid the drive to adopt new technology: With increasing adoption of technology, banks need to keep up with the needs of their customers and hiring the right talent has become crucial

NBFI sector

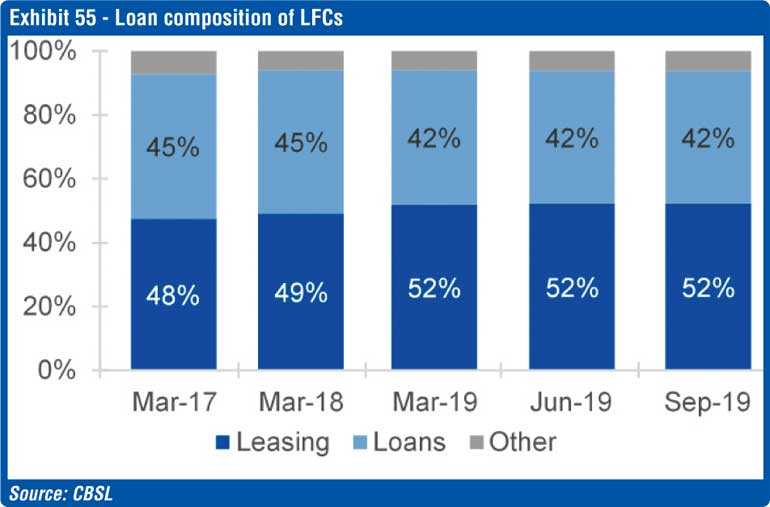

The NBFI sector consists of Licensed Finance Companies (LFCs) which accept customer deposits and provide leasing, loans and other financial services as well as Specialized Leasing Companies (SLCs) that have a narrower range of activities and not permitted to accept public deposits.

NBFIs rely on a mix of deposits from the public and borrowings primarily from commercial banks for their funding requirements. LFCs are predominately funded by customer deposits, with deposits accounting for 67% of the total funding mix. Several LFCs have raised funds from multilateral and unilateral agencies in the past.

In 2018/19 a combination of high tariffs, high depreciations and adverse macroeconomic conditions have led to sharp drop in vehicle imports and microfinance activity, which has led to a sharp reduction in loan growth.

The NBFI sectors growth potential lies in adopting technology which will help them improve customer service and reduce operational costs in the long term. Owing to a large number of NBFIs, the sector is expected to witness consolidation in the face of rising minimum capital requirements, low profitability and to reduce cost inefficiencies. Efforts by the CBSL to regulate microfinance activities by imposing tighter regulations on having a stronger capital base is expected to instil stability in the NBFI sector.

Challenges

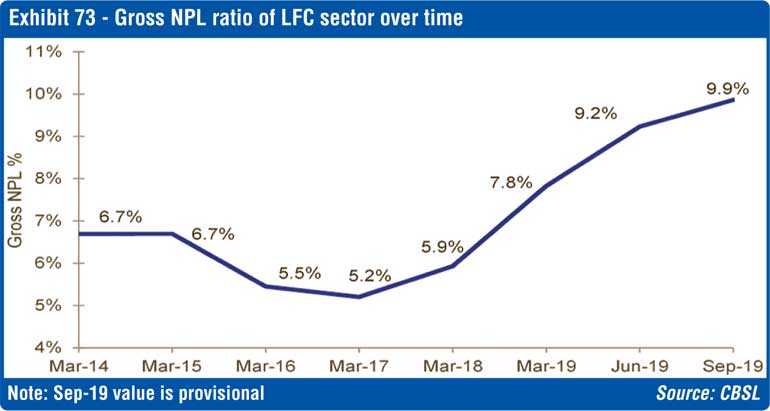

Increase in Non-Performing Loans exerts pressure on performance of LFCs: Subdued economic conditions, erratic weather patterns and the debt moratorium offered to tourism are factors to watch as they exert additional pressure on rising NPLs.

LFCs non-compliant with minimum capital requirements may face the scrutiny of the CBSL: With both banks and LFCs looking to raise substantial sums of capital in the market, it becomes increasingly difficult to attract sufficient capital to meet and sustain capital adequacy requirements.

Possible restrictions on importation of motor vehicles can curtail leasing portfolio growth: Vehicle leasing is the largest lending category of the majority of LFCs in Sri Lanka. Any limitations on vehicle imports or on lending activities for vehicle purchases has a negative impact on the industry.

High competition within and outside the sector affecting profitability: With around 42 LFCs serving a population of ~21 M the competitiveness among the firms is very high and beyond the optimum level of competition suitable for the sector.