Thursday Jul 09, 2026

Thursday Jul 09, 2026

Monday, 27 April 2020 01:22 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

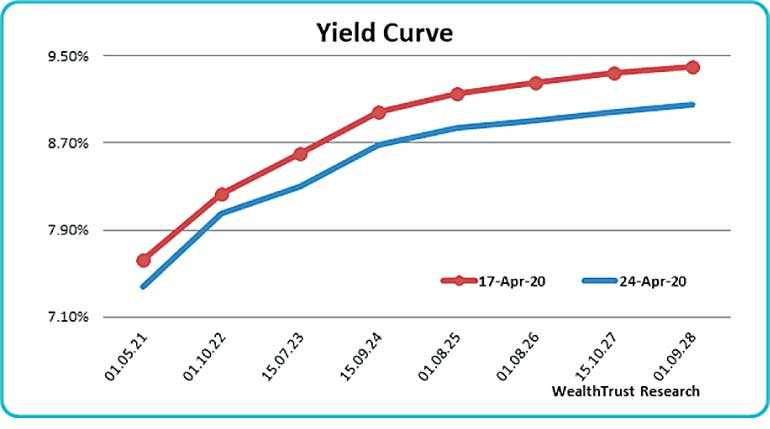

The continued positive sentiment in the secondary bond market led to aggressive local buying interest which resulted in a parallel shift downwards of the overall yields curve for the week ending 24 April.

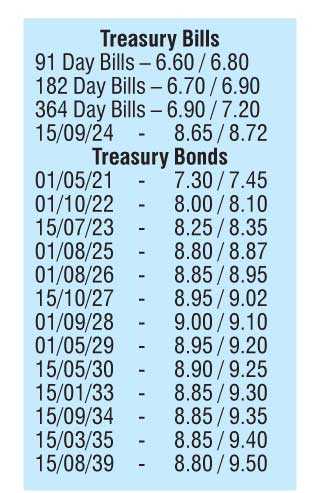

The bullish trend was further supported by the outcome of the weekly Treasury bill auctions, where a total amount of Rs. 22.13 billion was accepted against its previous weeks accepted amount of Rs. 9.91 billion and the Cabinet approval by the Government for a $ 400 million swap line with the Reserve Bank of India along with several other dollar credit lines in the pipeline.

Activity increased during the week ending 24 April, with the market favourite maturities of 2023s (i.e. 01.09.23 and 15.12.23), 2024s (i.e. 15.06.24, 01.08.24 and 15.09.24), 15.03.25 and 15.10.27 decreasing to weekly lows of 8.40%, 8.45%, 8.70%, 8.75%, 8.65%, 8.80% and 8.98% respectively against its previous weeks closing levels of 8.60/70, 8.65/75, 8.95/00, 9.00/10, 8.95/00, 9.05/15 and 9.30/37. In addition, maturities of 2021s (i.e. 01.03.21 & 01.05.21), 01.10.22 and 2023s (i.e. 15.05.23 & 15.07.23) were seen dipping to a low of 7.30%, 7.40%, 8.10% and 8.30% each as well.

The continued demand was also witnessed in the secondary bill market with July to October 2020 bills and January 2021 bills changings hands at lows of 6.70% and 7.00% respectively during the week.

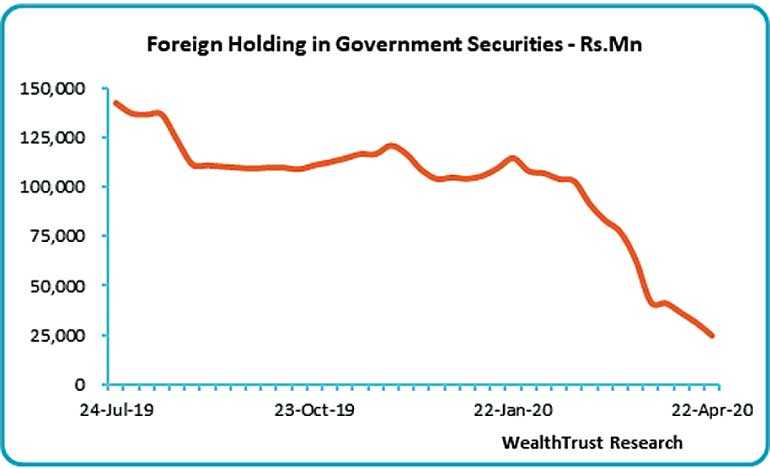

Nevertheless, the foreign component in rupee bonds decreased for a 13th consecutive week to register an outflow of Rs. 6.35 billion for the week ending 22 April, reducing its overall holding to Rs. 24.77 billion.

The daily secondary market Treasury bond/bill transacted volumes for the first three days of the week averaged at Rs. 8.42 billion.

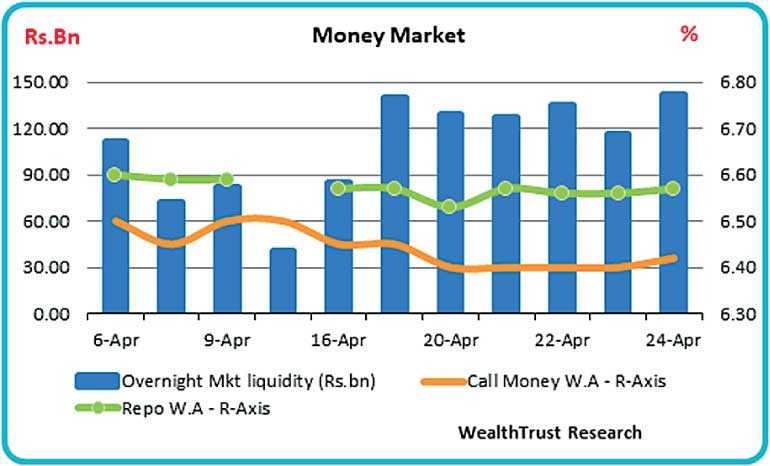

In money markets, attempts to infuse liquidity by the DOD (Domestic Operations Department) of Central Bank by way of reserve repo auctions drew no successful bids expect for Monday where only an amount of Rs. 0.5 billion was injected on an overnight basis at a weighted average rate of 6.50%.

The average net overnight liquidity was at Rs. 130.18 billion for the week while the overall net liquidity surplus stood at Rs. 82.13 billion by the end of the week. The weighted averages on overnight call money and repo rates decreased to average 6.43% and 6.56% respectively for the week.

USD/LKR

In the Forex market, the USD/LKR rate on spot contracts traded within the range of Rs. 191.72 to Rs. 196.00 during the week.

The daily USD/LKR average traded volume for the first four days of the week stood at $ 44.39 million.

(References: Central Bank of Sri Lanka, Bloomberg e-bond trading platform, money broking companies, economynext.com)