Sunday May 24, 2026

Sunday May 24, 2026

Monday, 13 November 2017 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The downward trend in secondary market bond and bill yields, witnessed during the previous week, continued during the week ending 10 November as well.

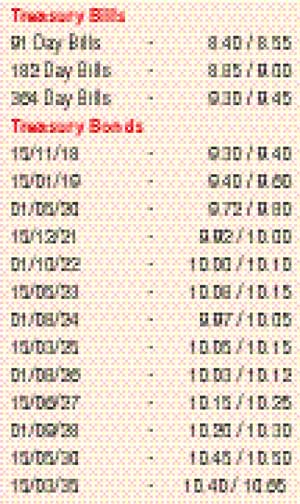

Yields of the foreign favoured maturities of 01.08.24, 01.08.25, 01.08.26 and 15.06.27 decreased to weekly lows of 10.00%, 10.08%, 10.10% and 10.22% respectively against its previous week’s closing levels of 10.15/20, 10.20/22, 10.15/25 and 10.20/30.

Furthermore, the 01.05.20, three 2021s (i.e. 01.03.21, 01.05.21 and 15.12.21) and 15.05.30 maturities dipped to lows of 9.75%, 9.90%, 9.95% each and 10.50% respectively, while on the shorter end, the 01.06.18 maturity and two 2019 maturities (i.e. 01.7.19 and 15.09.19) were seen dipping to lows of 9.00% and 9.60%.

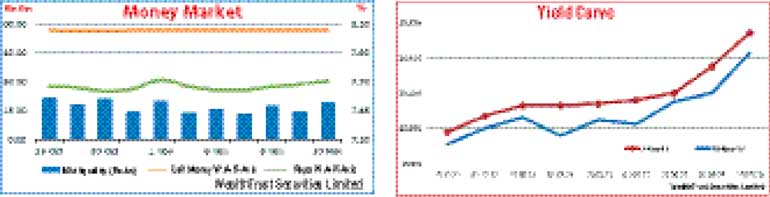

In the secondary bill market, considerable buying interest resulted in yields of bills maturing in January, February, March, July, August and September 2018, dipping to lows of 8.45%, 8.54%, 8.64%, 9.10%, 9.20% and 9.30% respectively. Furthermore, at the weekly primary auction, the weighted average yields of all three maturities decreased further.

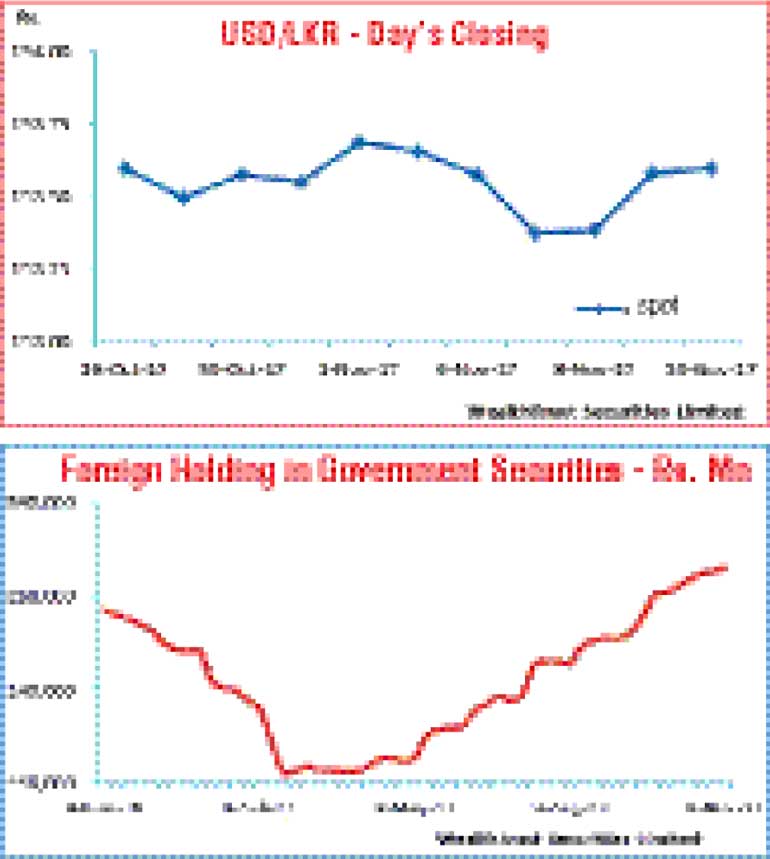

The foreign holding in rupee bonds continued to increase, recording an inflow of Rs. 1.6 billion for the week ending 8 November and the total outstanding increasing to Rs. 304.89 billion.

The daily secondary market Treasury bond/bill transacted volume for the first four days of the week averaged Rs. 6.94 billion.

In money markets, the overnight call money and repo rates remained steady to average at 8.15% and 7.66% respectively, with the Open Market Operations (OMO) Department draining out liquidity throughout the week on an overnight basis at a weighted average of 7.25%. The average net surplus liquidity in the system stood at Rs. 15.69 billion while the Central Bank of Sri Lanka’s Treasury bill holding stood at Rs. 39.36 billion.

Rupee closes mostly unchanged

The rupee on spot contracts was seen appreciating to intraweek highs of Rs. 153.36 during the week against its previous week’s closing levels of Rs. 153.60/68 on the back of selling interest by banks and inward remittances. However, it lost value once again towards the later part of the week to close at Rs. 153.55/65 on the back of importer demand.

The daily USD/LKR average traded volume for the four days of the week stood at $ 72.13 million.

Some of the forward dollar rates that prevailed in the market were one month - 154.40/50; three months - 156.20/30 and six months - 158.75/90.