Thursday Jun 11, 2026

Thursday Jun 11, 2026

Monday, 30 December 2019 01:41 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

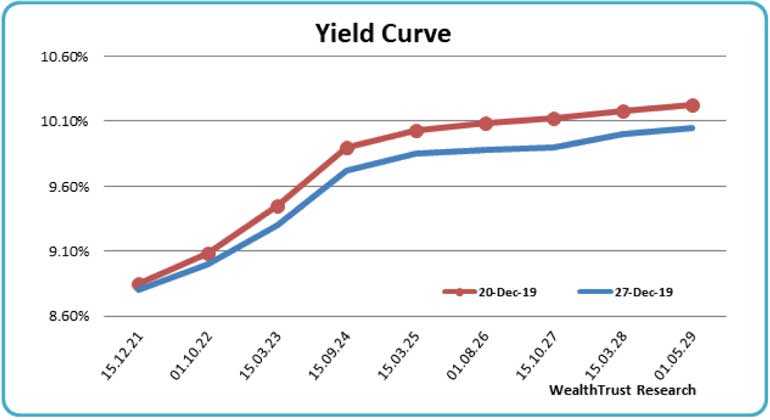

The secondary bond market was active during the short trading week ending 27 December, with yields initially decreasing prior to the monetary policy announcement and increasing once again thereafter.

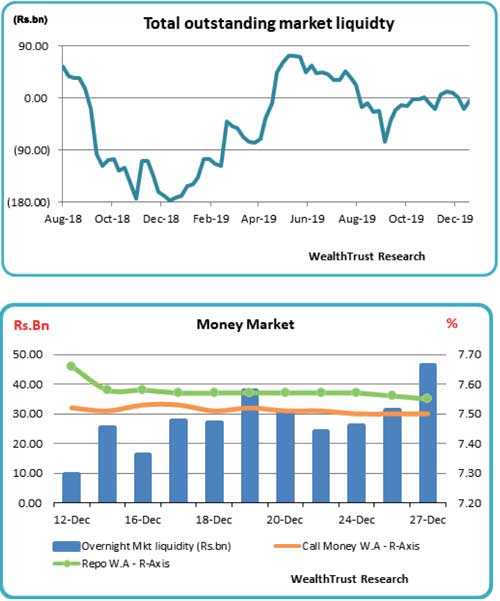

The Central Bank of Sri Lanka continued to keep the policy rates steady at 7.00% and 8.00% at its last monetary policy announcement for 2019, released on 27 December.

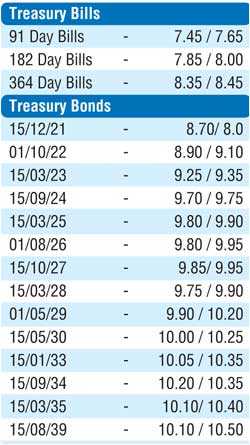

Trading mainly centred around the liquid maturities of 2023’s (i.e. 15.05.23, 15.07.23 and 15.12.23), 2024’s (i.e. 15.03.24, 15.06.24 and 15.09.24), 2026’s (i.e. 01.06.26 and 01.08.26) and 2027’s (i.e. 15.01.27 and 15.10.27) with yields decreasing to weekly lows of 9.35%, 9.38%, 9.45%, 9.57%, 9.53%, 9.55%, 9.72%, 9.70%, 9.80% and 9.88% respectively against its previous weeks closing levels of 9.45/60, 9.50/60, 9.55/70, 9.85/93 each, 9.87/92, 10.05/15, 10.05/12, 10.05/15 and 10.08/15.

The downward movement was further supported by the outcome of the weekly Treasury bill auction, where the weighted average yield of the market favourite 364-day maturity held steady at 8.45%, following a steep increase in the previous week.

Nevertheless, renewed selling interest following the monetary policy announcement resulted in yields increasing once again with the 2024’s (i.e. 15.06.24, 01.08.24 and 15.09.24), 01.08.25 and 15.01.27 maturities changing hands at levels of 9.75%, 9.85%, 9.77%, 9.90% and 9.95% respectively. However, the overall yield curve reflected a marginal parallel shift downwards when compared with the previous week.

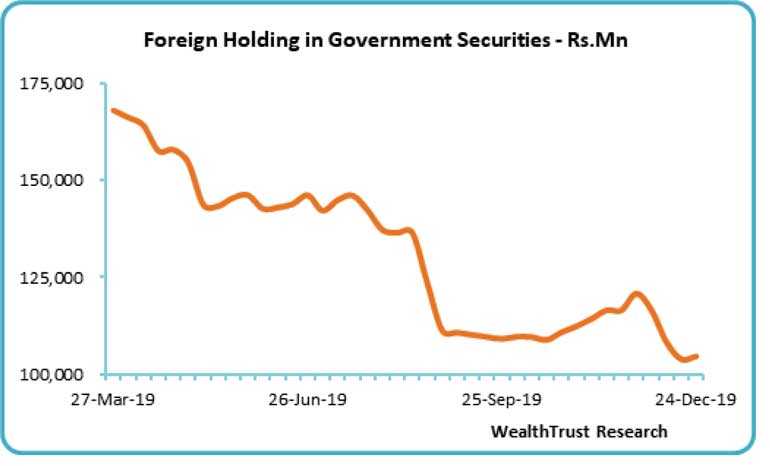

The foreign holding in rupee bonds was seen reversing its decreasing trend witnessed over the previous three weeks to record a marginal inflow of Rs. 735 million for the week ending 27 December.

The daily secondary market Treasury bond/bills transacted volume for the first three days of the week averaged Rs. 8.36 billion.

In money markets, The Open Market Operations (OMO) Department of the Central Bank was seen injecting liquidity during the week by way of overnight, five, 13 and 14-day reverse repo auctions at weighted average yields ranging from of 7.48% to 7.60%, as the overall liquidity in the system remained at a deficit of Rs. 4.30 billion. Call money and repo rates averaged at 7.50% and 7.56%.

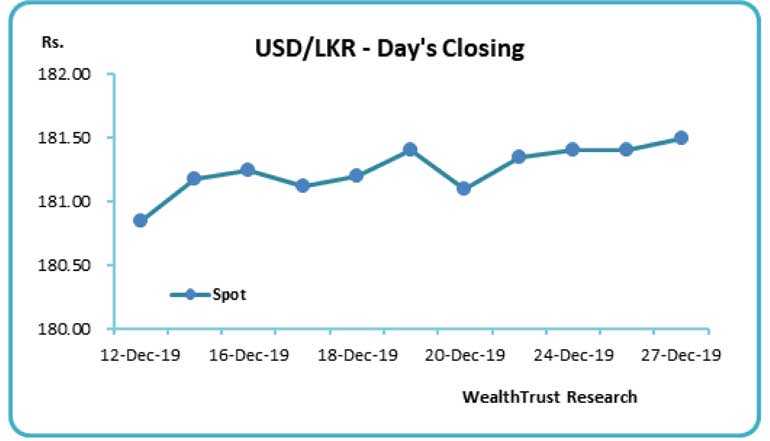

In the Forex market, the USD/LKR rate on spot contracts depreciated during the week to close at Rs. 181.45/55 against its previous week’s level of Rs.181.05/15 on the back of buying interest by banks.

The daily USD/LKR average traded volume for the first three days of the week stood at $ 92.16 million.

Some of the forward dollar rates that prevailed in the market were 1 month – 181.90/05; 3 months – 182.80/00 and 6 months – 184.35/65