Saturday Jul 04, 2026

Saturday Jul 04, 2026

Monday, 6 December 2021 03:06 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

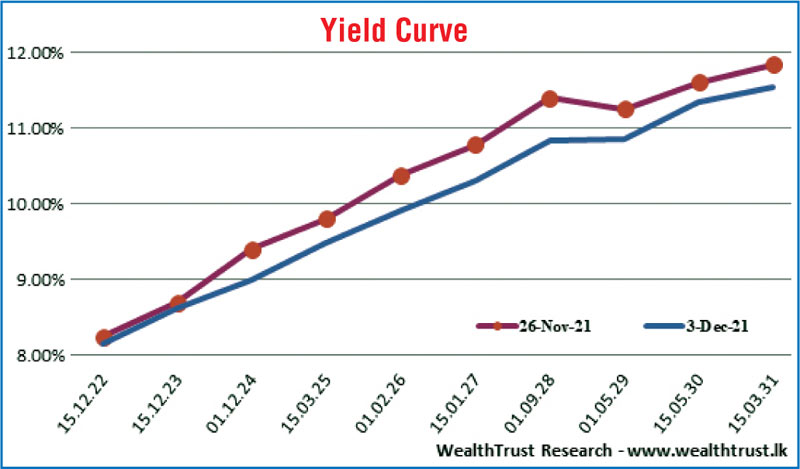

The secondary bond market yield curve recorded a shift downwards during the week ending 3 December, on the back of renewed buying interest driven by the continued positive outcomes of primary auctions.

The secondary bond market yield curve recorded a shift downwards during the week ending 3 December, on the back of renewed buying interest driven by the continued positive outcomes of primary auctions.

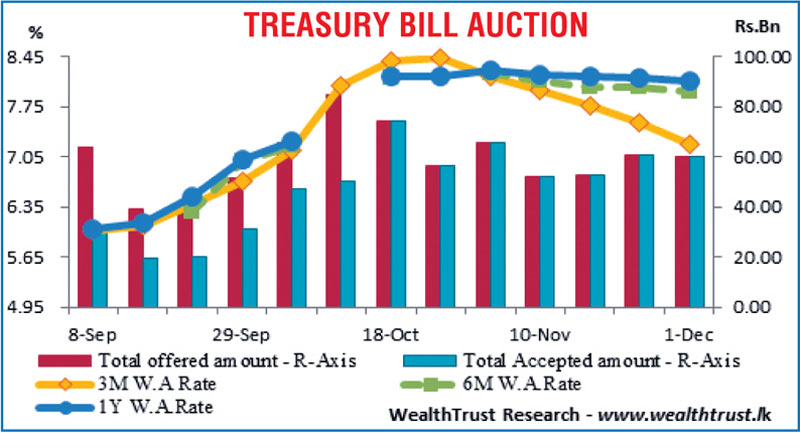

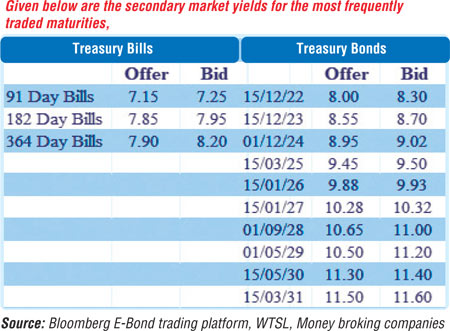

At the weekly Treasury bill auction, the total auctioned amount of Rs. 60 billion was fully subscribed for the seventh consecutive week, while the weighted average rate of the 91-day bill decreased by a further 30 basis points to 7.23%. The weighted average rates of the 182-day and 364-day bills decreased by five and four basis points respectively, while the accepted amount on the 182-day maturity was seen exceeding the 91-day for the first time in 29 weeks.

At the Treasury bond auctions, the total offered amount of Rs. 30 billion was fully accepted in its first phase of the auctions, while the weighted averages were recorded marginally below its secondary market rates, while a further amount of Rs. 3 billion was successfully issued under the Direct Issuance window on the 15.05.2030 maturity.

On the back of increased activity, considerable buying interest on the liquid maturities 01.12.24, 15.03.25, 15.01.26, 15.01.27, 01.09.28, 15.05.30 and 15.03.31 saw its yields dip to lows of 9%, 9.48%, 10.02%, 10.30%, 11.15%, 11.50% and 11.78% respectively against its previous weeks closing levels of 9.35/45, 9.70/90, 10.30/45, 10.70/85, 11.30/50, 11.50/70 and 11.80/88. Furthermore, 2023’s (i.e., 15.05.23, 15.07.23, 01.09.23 and 15.12.23) and other 2024’s (i.e., 15.03.24 and 15.09.24) were seen changing hands from highs of 8.75% and 9.30% respectively to lows of 8.35% and 8.95%. In secondary market bills, December 2021, January to March 2022 and June 2022 maturities changed hands at levels of 6.75%, 7% to 7.40% and 7.64% to 7.93% respectively.

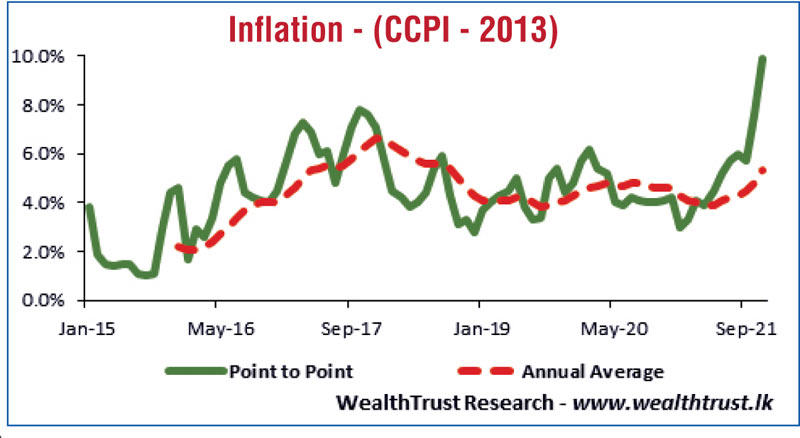

This was in the backdrop of the Colombo Consumer Price Index (CCPI - Base 2013=100) increasing to its highest level since its rebase in January 2015, to record 9.9% on its point-to-point for November when compared against its previous month’s figure of 7.6%. The foreign holding in rupee bonds decreased marginally to Rs. 1.75 billion for the week ending 1 December, while the daily secondary market Treasury bond/bill transacted volumes for the first four trading days of the week averaged Rs. 15.44 billion.

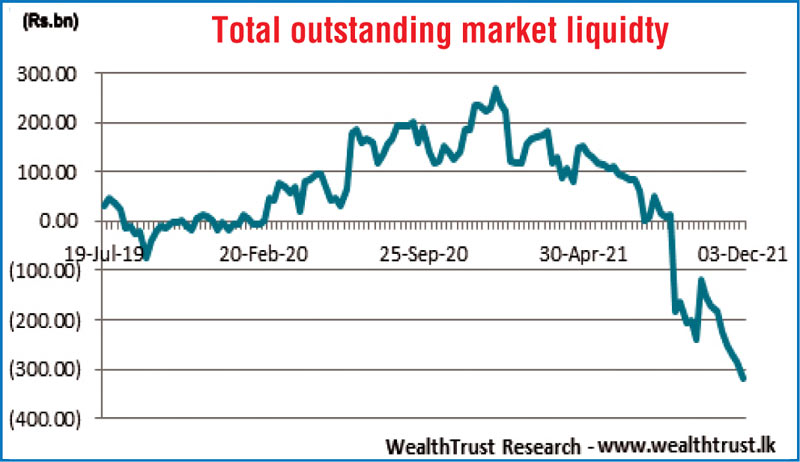

In money markets, the total outstanding liquidity deficit continued to increase during the week to register at Rs. 319.30 billion by the end of the week against its previous week’s Rs. 282.99 billion, while CBSL’s holding of Gov. Securities continued to decrease to record Rs. 1,414.67 billion against its previous week’s Rs. 1,433.91 billion. The weighted average rates on overnight call money and repo were 5.92% and 5.96% respectively for the week.

The Domestic Operations Department (DOD) of the Central Bank was seen draining out liquidity during the week by way of overnight to seven-day repo auctions at weighted average yields ranging from 5.97% to 5.99%. Furthermore, an amount of Rs. 7.10 billion was sold by way of outright sales of Treasury bills for periods ranging from 77 days to 98 days at weighted averages ranging from 7.08% to 7.23%.

USD/LKR

In the Forex market, the USD/LKR rate on spot contracts continued to trade at Rs. 203 during the week while overall activity remained moderate.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 66.96 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)