Thursday May 28, 2026

Thursday May 28, 2026

Monday, 10 January 2022 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

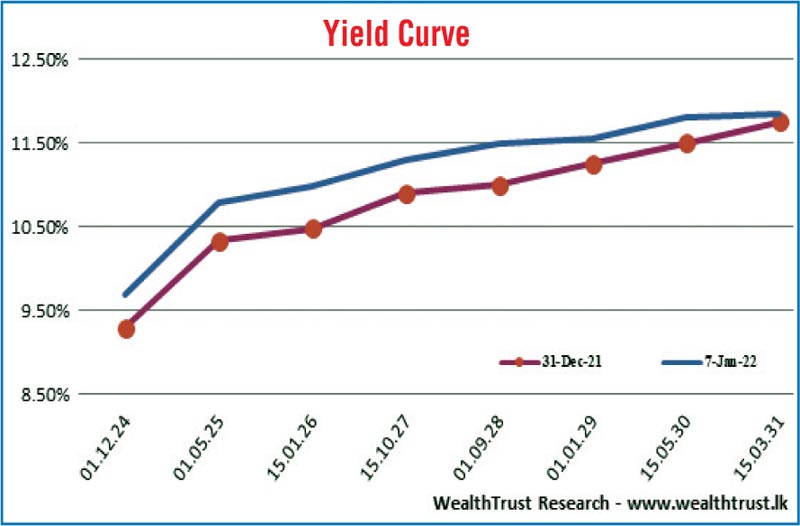

The positive momentum which was witnessed in the secondary bond market during the week ending 31 December 2021, following the unanticipated outcome of the bond auctions during that week, where all bids received for two maturities were rejected, was seen reversing to a bearish sentiment during the week ending 7 January ahead of the upcoming Treasury bond auctions due on 11 January.

The positive momentum which was witnessed in the secondary bond market during the week ending 31 December 2021, following the unanticipated outcome of the bond auctions during that week, where all bids received for two maturities were rejected, was seen reversing to a bearish sentiment during the week ending 7 January ahead of the upcoming Treasury bond auctions due on 11 January.

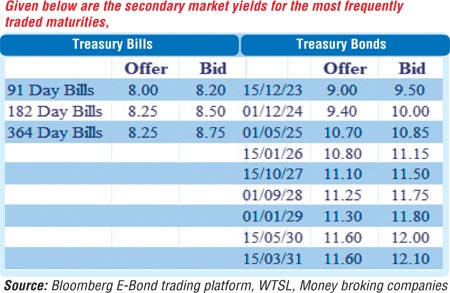

The yield of the liquid 01.05.25 maturity increased to a weekly high of 10.70% in comparison to its previous weeks closing level of 10.30/35. In addition, 01.08.25 and 15.05.30 maturities were seen trading at a level of 11.10% and 11.765% respectively as well. Furthermore, two-way quotes were seen widening and increasing across most maturities.

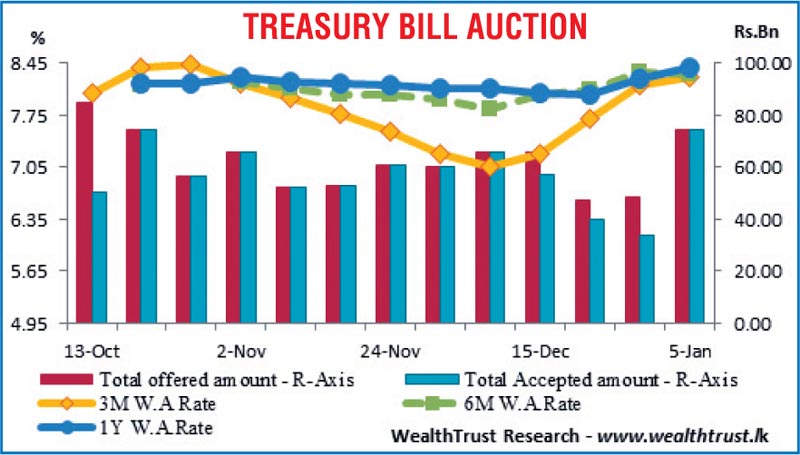

The weekly Treasury bill auction conducted during the week produced a mixed result, as the weighted average rate on the 91 day bill increased further by 10 basis points to 8.26% while the total auction was fully subscribed for the first time in four weeks.

In the secondary bill market, January, February and March 2022 maturities were traded at levels of 6.55% to 7.05%, 6.85% to 7.10% and 7.75% to 7.85% respectively during the week while yields on the latest 91 day bill was seen decreasing during post auction trading to change hands at a low of 8.00%.

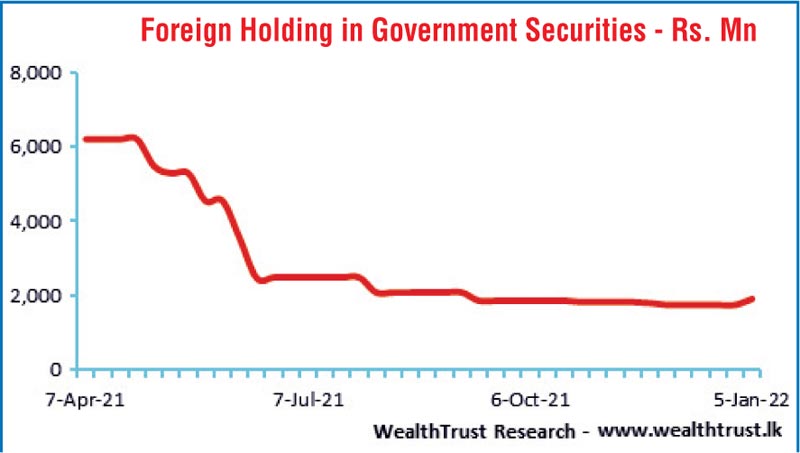

The foreign holding in rupee bonds was seen increasing during the week to record an inflow of Rs. 160.72 million for the week ending 5 January while the daily secondary market Treasury bond/bill transacted volumes for the first four trading days of the week averaged Rs. 15.97 billion.

In money markets, the Domestic Operations Department (DOD) of Central Bank was seen draining out liquidity by way of an overnight repo auction at a weighted average rate of 5.97% on Friday as the deposited amount at Central Banks Standard Deposit Facility Rate (SDFR) of 5.00% increased during the week from a low of Rs. 101 billion to a high of Rs. 141 billion.

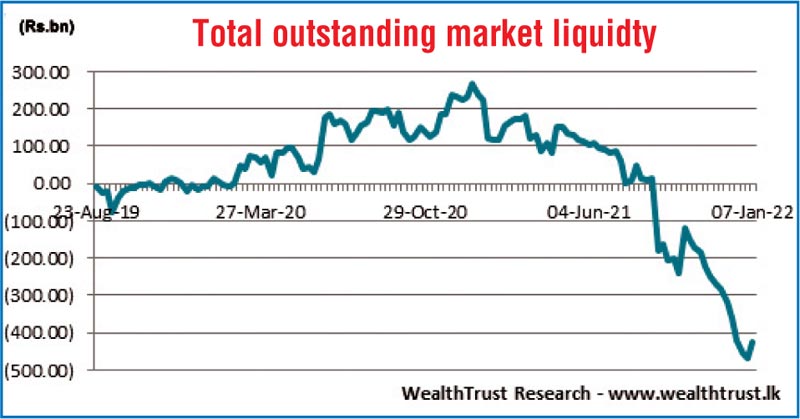

The total outstanding liquidity deficit decreased during the week to Rs. 424.45 billion by the end of the week against its previous weeks of Rs. 466.25 billion while CBSL’s holding of Government securities remained mostly unchanged at Rs. 1,416.39 billion.

The weighted average rates on call money and repo remained mostly unchanged at 5.94% and 5.96% respectively for the week as a high volume exceeding Rs. 424 billion was withdrawn on a daily basis during the week from Central Banks Standard Lending Facility Rate (SLFR) of 6.00%.

USD/LKR

In Forex markets, overall activity continued to remain moderate during the week while limited trades were witnessed on the USD/LKR spot contracts within the range of Rs. 202.97 to Rs. 203.00.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 48.36 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking

companies)