Wednesday Jul 01, 2026

Wednesday Jul 01, 2026

Monday, 18 January 2021 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The bullish sentiment in the secondary bond market continued for a second consecutive week ending 15 January as well, boosted by the bullish outcomes of the primary auctions conducted during the week. At the T-Bond auctions, the total offered amount was fully subscribed for the first time since July 2020 while the T-Bill auction was fully subscribed for a second consecutive week.

The bullish sentiment in the secondary bond market continued for a second consecutive week ending 15 January as well, boosted by the bullish outcomes of the primary auctions conducted during the week. At the T-Bond auctions, the total offered amount was fully subscribed for the first time since July 2020 while the T-Bill auction was fully subscribed for a second consecutive week.

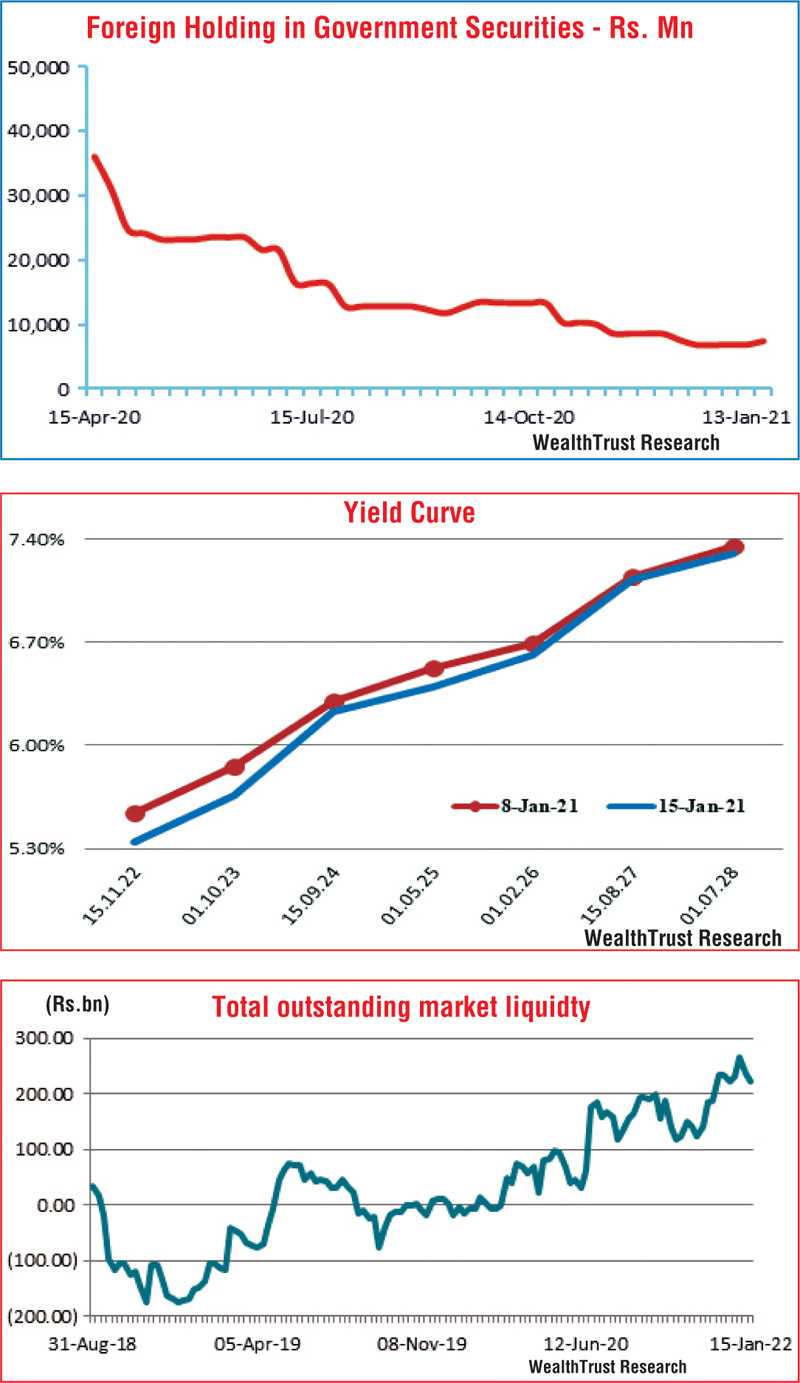

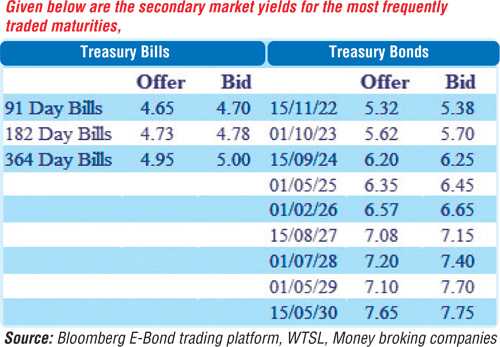

A majority of activity was witnessed on the liquid short to mid-term maturities of 2022’s (i.e. 15.11.22 and 15.12.22), 2023’s (15.01.23 and 01.10.23) and 2024’s (i.e. 15.09.24 and 01.12.24) as its yields were seen dipping to over two month lows of 5.35%, 5.32%, 5.40%, 5.63%, 6.18% and 6.22%, respectively, against its previous weeks closing levels of 5.52/55, 5.52/55, 5.53/57, 5.85/87, 6.28/32 and 6.35/40. In addition maturities of 15.10.21 and other 2022’s (i.e., 15.03.22, 01.07.22 and 01.10.22) and 2023’s (i.e. 15.03.23, 15.07.23 and 15.12.23) traded at levels of 4.90%, 5.10% to 5.35% and 5.50% to 5.87% as well. The mid to long end maturities of 01.05.25, 01.02.26, 15.08.27 and 15.05.30 traded at lows of 6.32%, 6.55%, 7.10% and 7.65%, respectively, against its previous weeks closing level of 6.50/55, 6.65/72, 7.10/18 and 7.70/90, reflecting a downward shift of the overall yield curve for a third consecutive week. However, selling interest at these levels resulted in yields increasing marginally from its weekly lows towards the latter part of the week.

In the secondary bill market, April 2021, July 2021, September 2021, October 2021 and January 2022 changed hands at levels 4.60% to 4.71%, 4.78%, 4.80%, 4.90% to 4.93% and 4.98%, respectively,.

Meanwhile, the foreign holding in Rupee bonds increased once again, recording an inflow of Rs. 550 million for the week ending 13 January.

The daily secondary market Treasury bond/bill transacted volumes for the first three trading days of the week averaged Rs. 26.03 billion.

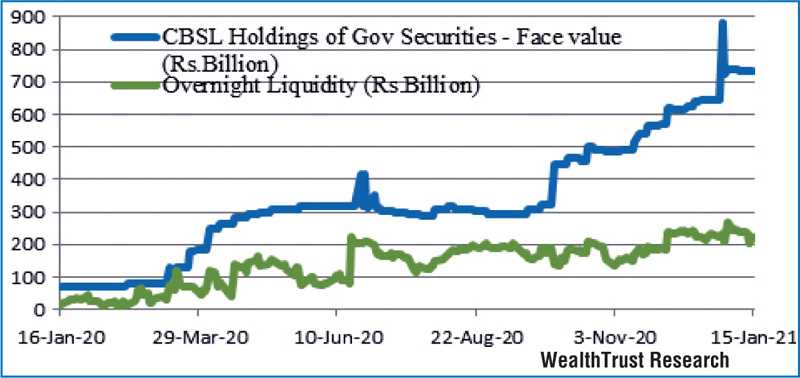

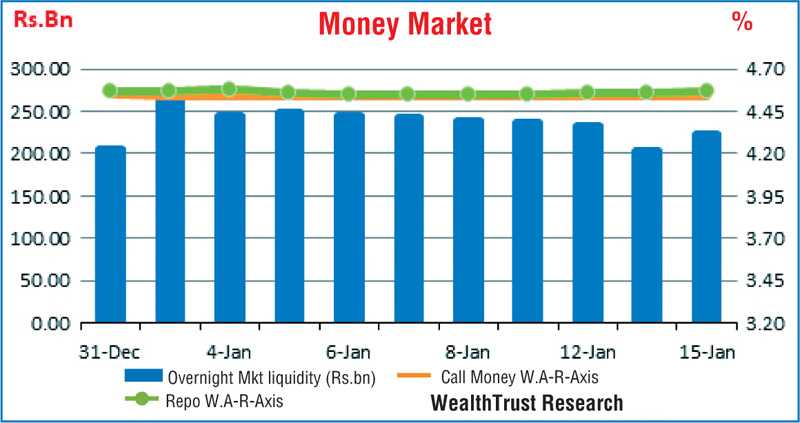

In the money market, the total outstanding market liquidity decreased to a surplus of Rs. 222.45 billion against its previous week’s amount of Rs. 238.35 billion while the CBSL’s holding of government securities remained steady at Rs. 731.25 billion. The weighted average rates on overnight call money and repos remained mostly unchanged to average at 4.54% and 4.56%, respectively, for the week.

Rupee depreciates

In the Forex market, The USD/LKR rate on spot next contracts was seen depreciating during the week to close the week at Rs. 193/195 against its previous day’s closing of Rs. 190.50/192 due to the demand by banks.

The daily USD/LKR average traded volume for the first three days of the week stood at $ 56.38 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, money broking companies)