Thursday May 28, 2026

Thursday May 28, 2026

Monday, 8 April 2019 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary bond market remained bullish during the week ending 5 April 2019 with yields declining considerably across the curve on the back of substantial buying interest, which led to a parallel shift down of the overall yield curve, week on week.

The downward spiral in yields was ahead of today’s much speculated monetary policy announcement, the second for the year 2019, due at 4:30 p.m. The Central Bank of Sri Lanka kept policy rates unchanged at its announcement on 22 February while reducing its Statutory Reserve Ratio (SRR) applicable for all licensed commercial banks by a 100 basis points to 5.00% from its previous 6.00% in order to ease the prevailing liquidity shortfall at the time.

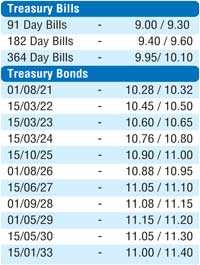

The downward rally in yields was supported by the impressive outcome of the primary bond auctions conducted during the week along with the bill auction, which saw the 364 day bill weighted average nose dive by 25 basis points to 10.15%.

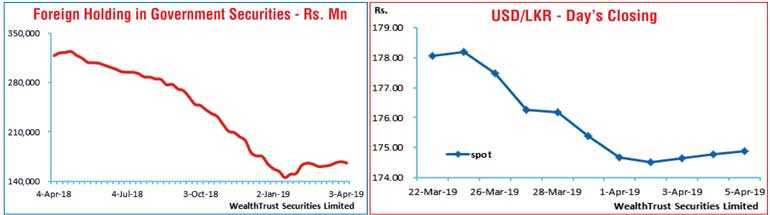

Activity in the secondary bond market increased considerably during the week across the yield curve with the liquid maturities of two 2021’s (i.e. 01.08.21 and 15.12.21), 15.03.22, 15.03.23, 15.03.24, 01.08.26, two 2027’s (i.e. 15.01.27 and 15.06.27) and 01.05.29 hitting weekly lows of 10.28%, 10.30%, 10.45%, 10.63%, 10.75%, 10.90%, 10.95%, 11.08% and 11.17% respectively against its previous weeks closing levels of 10.50/55, 10.55/58, 10.60/80, 10.83/88, 10.97/00, 11.10/20, 11.17/27, 11.25/33 and 11.38/42. This was despite the foreign holding in Rupee bonds recording an outflow of Rs. 1.8 billion for the week ending 3 April, reversing four consecutive weeks of inflows.

The daily secondary market Treasury bond/bill transacted volume for the first four days of the week averaged Rs. 15.25 billion.

In money markets, the average overnight net liquidity shortfall in the system reduced to Rs. 9.79 billion for the week against its previous week of Rs. 13.16 billion as the Open Market Operations (OMO) Department of Central Bank continued to inject liquidity during the week on an overnight basis at a weighted average yields ranging from 8.50% to 8.55%. In addition, it injected funds by way of seven to eleven day reverse repo auctions at weighted average yields ranging from 8.51% to 8.55%. The overnight call money and repo rates averaged 8.51% and 8.58% respectively for the week as the total outstanding market liquidity shortfall stood at Rs. 76.28 billion.

Rupee appreciates further

In the Forex market, the Rupee on its spot contracts appreciated further during the week to close the week at Rs. 174.80/00 against its previous weeks closing level of Rs. 175.30/50 on the back of exporter conversions and continued seasonal remittances.

The daily USD/LKR average traded volume for the first four days of the week stood at $ 75.29 million.

Some of the forward dollar rates that prevailed in the market were one month – 175.85/95; three months – 177.65/75 and six months – 180.30/45.