Saturday Jul 04, 2026

Saturday Jul 04, 2026

Monday, 19 December 2022 01:59 - - {{hitsCtrl.values.hits}}

By WealthTrust Securities

The dull sentiment in the secondary bond market witnessed over the previous week continued during the trading week ending 16 December as well. The mixed outcome at the Treasury bond auctions coupled with the uncertainties that continue to hang over the market were seen as the reasons behind the dull sentiment.

The dull sentiment in the secondary bond market witnessed over the previous week continued during the trading week ending 16 December as well. The mixed outcome at the Treasury bond auctions coupled with the uncertainties that continue to hang over the market were seen as the reasons behind the dull sentiment.

At the T-bond auctions, only Rs. 123.89 billion was accepted in total against a total offered amount of Rs. 160 billion. However, the offered amount of Rs. 70 billion on the 15.05.2026 maturity was fully subscribed at the auction while an additional Rs. 14 billion which was offered through its direct issuance window was fully taken as well. The total bids received on the 15.05.2026 maturity was Rs. 280.98 billion while it recorded a weighted average of 31.45% against its previous average of 31.69%, recorded on 29 November.

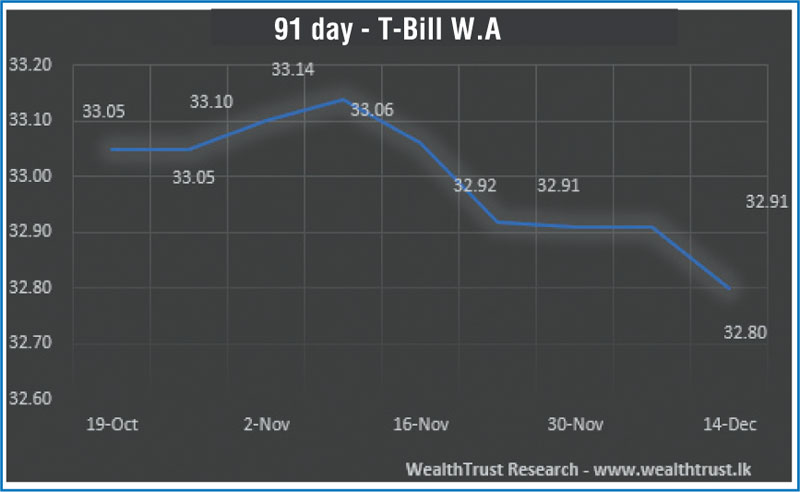

Nevertheless, the total offered amount of Rs. 98 billion at the weekly Treasury bill auction was fully subscribed at its 1st phase of the auction while a further amount of Rs. 16.89 billion was taken at its 2nd phase. The weighted average rates on all three maturities decreased as well.

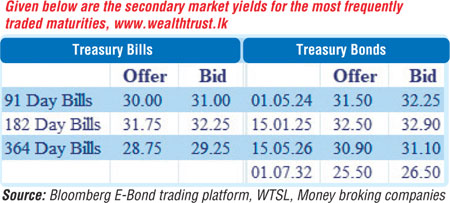

Bond market activity was witnessed mainly on the liquid maturities of 01.05.24 and 15.05.26 at levels of 31.50% to 32.20% and 30.60% to 31.05% respectively against its previous week’s closing levels of 31.90/10 and 30.50/25. In addition, the newly issued 15.01.25 along with 15.07.29 and 01.07.32 maturities traded at levels of 32.50% to 32.80%, 27.75% to 28.00% and 26.50% to 27.25% respectively as well. In the secondary bill market, January-February, March, June and December 2023 maturities changed hands at levels of 25.00% to 28.50%, 30.00% to 31.00%, 32.00% to 32.45% and 29.00% to 29.25% respectively.

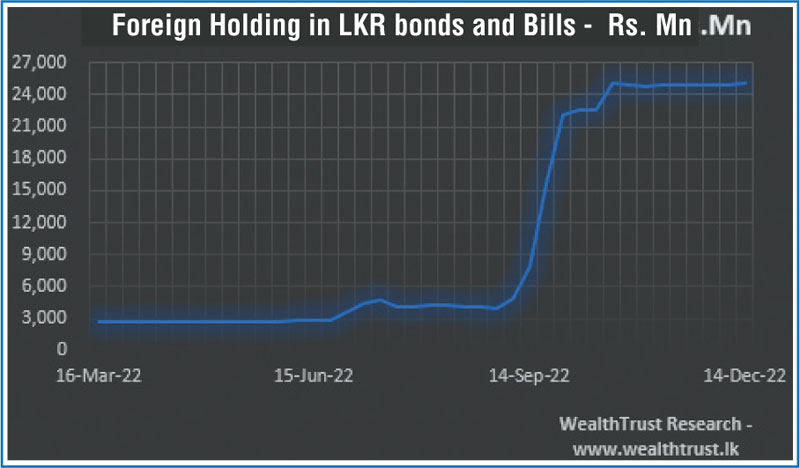

The foreign holding in rupee bonds recorded a marginal increase of Rs. 178.98 million for the week ending 14 December while the daily secondary market Treasury bond/bill transacted volumes for the first four trading days of the week averaged Rs. 31.01 billion.

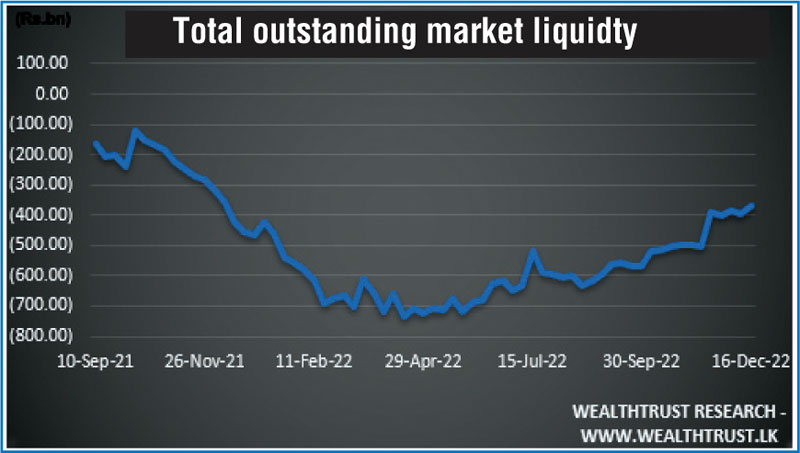

In money markets, the total outstanding liquidity deficit reduced to Rs. 370.84 billion by the end of the week against its previous week’s of Rs. 397.50 billion while CBSL’s holding of Government Securities increased to Rs. 2,602.86 billion against its previous week’s of Rs. 2,538.78 billion.

USD/LKR

In the forex market, the middle rate for USD/LKR spot contracts remained steady at Rs. 363.18 throughout the week. The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 33.58 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)