Sunday Jul 12, 2026

Sunday Jul 12, 2026

Tuesday, 16 May 2017 00:10 - - {{hitsCtrl.values.hits}}

The Government recently announced that the economic growth for 2016 was 4.4%. Considering the steadily-deteriorating macro-fundamentals throughout 2015 and 2016, many were surprised about this officially reported growth figure, since such figure did not seem to be in sync with the country’s other connected macro-indicators.

With the release of the Central Bank Annual Report for 2016 (AR 16), the supporting data and information has been made available in the public domain, and therefore the underlying numbers and logic in respect of the computation of growth for the year 2016 could now be critically analysed. Consequent to such a detailed study, many shocking facts and data have come to light which suggest that several instances of gross manipulation of figures and data have apparently taken place with the probable intention to “window-dress” the growth numbers for the years 2016, 2015 and 2014 in order to portray the present administration in a more favourable and beneficial light.

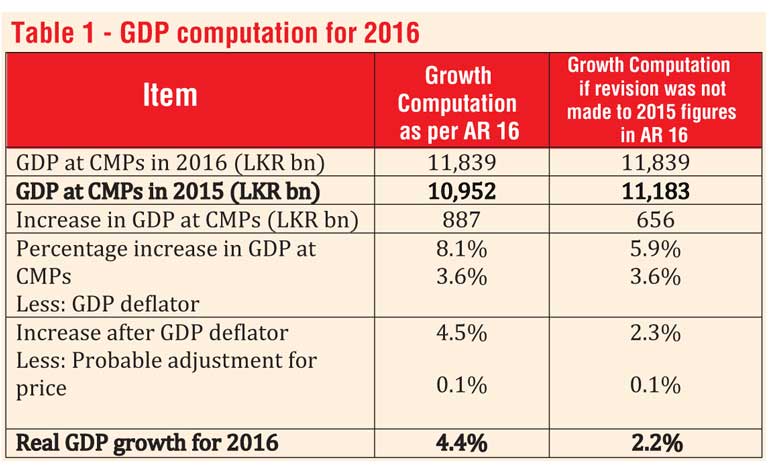

As per AR 16, the Gross Domestic Product (GDP) at Current Market Prices (CMPs) for 2016 has been reported at Rs. 11,839 billion, while the GDP at CMPs for 2015 has been stated at Rs. 10,952 billion. Accordingly, the increase in GDP at CMPs for 2016 has been reported as Rs. 887 billion, which is a percentage increase of 8.1%. Thereafter, by deducting the reported GDP deflator of 3.6% and making a further adjustment of 0.1%, real growth for 2016 has been reported as 4.4%.

It would be observed however, that the GDP at CMPs for 2015 as per the Central Bank Annual Report for 2015 (AR 15) was Rs. 11,183 billion, which was Rs. 231 billion higher than the value of Rs. 10,952 billion used in the 2016 GDP computation. Accordingly, if the GDP at CMPs for 2015 as per AR 15 (the “base” value for the computation of the 2016 growth rate) had not been revised by this initial “adjustment”, the increase during 2016 would have been only Rs. 656 billion. (i.e, 11,839-11,183). In that event, the percentage increase in GDP at CMPs in 2016 would have been only [(656÷11,183) x 100], or 5.9%. From such figure, had the GDP deflator of 3.6% and a further adjustment of 0.1% been deducted, the Real Growth for 2016 would have been only 2.2%. The details of such computation are set out in Table 1.

As per the computation at Table 1, it would be seen that the “creation” of the higher growth rate for 2016 was achieved through the convenient “shifting” of Rs. 231 billion of GDP at CMPs from 2015 to 2016. However, such adjustment, in turn, also reduced the GDP at CMPs for 2015 from Rs. 11,183 billion to Rs. 10,952 billion, which would have meant that the GDP at CMPs for 2015 would have suffered a reduction of the identical amount, causing a sizeable dent to the 2015 growth numbers. Therefore, in order to at least partially offset such reduction so as to avoid attention to the exercise, another “creative” downward revision seems to have been made to the GDP at CMPs for 2014 as well.

This second “adjustment” was to reduce and re-state the GDP at CMPs for 2014 from Rs. 10,448 billion as per the AR 15, to Rs. 10,361 billion in AR 16. This move, in turn, resulted in the GDP at CMPs for 2014 reducing by LKR 87 billion, and adding such value to the GDP at CMPs for 2015. Accordingly, this second “adjustment” served to partially compensate the reduction suffered by the GDP at CMPs for 2015 due to the initial “adjustment”.

However, it would have been known that these ad hoc changes to the GDP at CMPs values for 2014 and 2015, (while serving to achieve the important outcome of higher growth for 2016), would have also led to some new issues, since those changes would have resulted in the growth figures for 2015 and 2014 having to be revised downwards quite significantly. In fact, if only the above mentioned first and second “adjustments” had been carried out, the real growth for 2015 would have crashed from 4.8% (as announced in AR 15) to 3.6%, while the real growth for 2014 would have plunged from 4.9% (as announced in AR 15) to 4.1%. Hence, a third “adjustment” has been introduced in order to maintain, or at least closely match, the already announced growth rates for 2015 and 2014, so as to not draw too much attention towards the first and second “adjustments”. It is probably that necessity that led to the third “adjustment”, which was to materially change the GDP deflator for the years 2014 and 2015, with retrospective effect!

The ‘GDP deflator’

The ‘GDP deflator’ is an economic measure of inflation and is derived by dividing the nominal GDP by real GDP. It is a vitally-important measure because the nominal GDP includes inflation, while real GDP does not. Since the GDP deflator measures the difference between real GDP and nominal GDP, it is often considered a more accurate measure for price inflation, and economists  generally prefer this ratio because, unlike pure price indices, (e.g., CPI), the GDP deflator is not based on a fixed basket of goods and services which could change with people’s consumption and investment patterns.

generally prefer this ratio because, unlike pure price indices, (e.g., CPI), the GDP deflator is not based on a fixed basket of goods and services which could change with people’s consumption and investment patterns.

In fact, for the GDP deflator, the “basket” for each year is the total set of all goods that are produced domestically, weighted by the market value of the total consumption of each of such goods. Naturally therefore, the GDP deflator, like the values for inflation, is a very important economic measure that needs to be computed with utmost care, consistency and professionalism, and is not a measure that should to be trifled with, or changed at anyone’s whims and fancies.

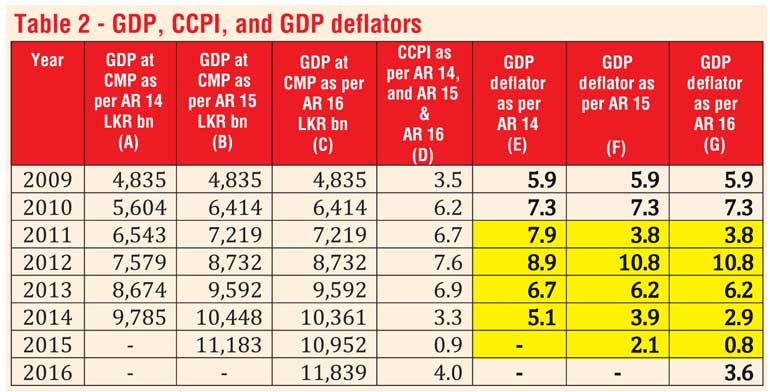

Sadly however, over the past two years, such respect has not been accorded to the GDP deflator, and this fact is evident from Table 2 which sets out the GDP at CMPs, CCPI as per the ARs, and the changing GDP deflators as per the AR 14, AR 15 and AR 16.

A study of Table 2 clearly reveals that the GDP deflator has been liberally adjusted in 2014, 2015 and 2016, notwithstanding the fact that even a slight change to the value of the GDP deflator would have a tremendous impact on the country’s real growth rate for the different years. At the same time, it would also be noted that those who were quite casually “adjusting” the value of the GDP deflator took care not to revise or adjust the average CCPI, possibly because any change to the familiar inflation rate would have led to a serious public discourse and undue attention.

From Table 2, it would be seen that as per AR 15, the GDP deflator for 2011 had been slashed from 7.9% to 3.8%, while the average CCPI has remained unchanged at 6.7%. For 2012, the GDP deflator had been increased from 8.9% to 10.8%, while the average CCPI has remained unchanged at 7.6%. For 2014, the GDP deflator had been reduced from 5.1% to 3.9%, while the average CCPI for that year has remained unchanged at 3.3%. Through all these major upward or downward adjustments to the GDP deflator which resulted in major upheavals in the Real Growth rates for 2010, 2011, 2012, 2013 and 2014, the only explanation given to justify the change was a tiny six-point font ‘foot-note’ which stated: “This series has been computed by splicing several series of implicit GDP deflators obtained with different base years. Hence, it would differ from a series compiled using the current and constant values of GDP”.

As already stated, the GDP deflator is essentially a broader measure of inflation and since the CCPI is also a measure of inflation in Sri Lanka, it stands to reason that if for some reason, the GDP Deflator needed to be adjusted, the same reason would have been equally valid to effect a revision or adjustment to the CCPI figures as well. Hence, if no adjustment had been effected to the CCPI figures, it would be very difficult to justify a huge change in the GDP deflator. Such logic leads to the inevitable conclusion that the change to the GDP deflator was effected to achieve some other ulterior purpose, and not to fulfil a professional objective or to rectify some major error. Further, it is untenable to claim that the GDP deflator could be affected by the splicing of the nominal GDP, and hence, that ‘foot-note’ explanation is also likely to be proved technically unsound.

Questionable calculations and results

Notwithstanding all these shortcomings, the reality is that a major upheaval was effected to the real GDP computations of several years via this dubious GDP deflator change as per AR 15. At that time however, the questionable calculations and results seem to have passed unnoticed and unchallenged, perhaps because the outcomes seemed to mainly relate to past figures and statistics. Nevertheless, it is likely that the comparative ease with which these major changes to vital economic numbers were effected and accepted, would have emboldened the relevant authorities to rely on the same method once again to “adjust” the past growth numbers as reported in AR 16.

Accordingly, the authorities seem to have proceeded to further revise, adjust and re-state the GDP deflators for 2014 and 2015. This time around however, the intention appears to be to simply adjust Real Growth for the two years 2014 and 2015, so as to nullify the impact of the change in growth resulting from the reduction in the GDP at CMPs, and thereby ensuring that the growth percentages for the respective years remain at the same or almost-the-same values as reported in AR 15.

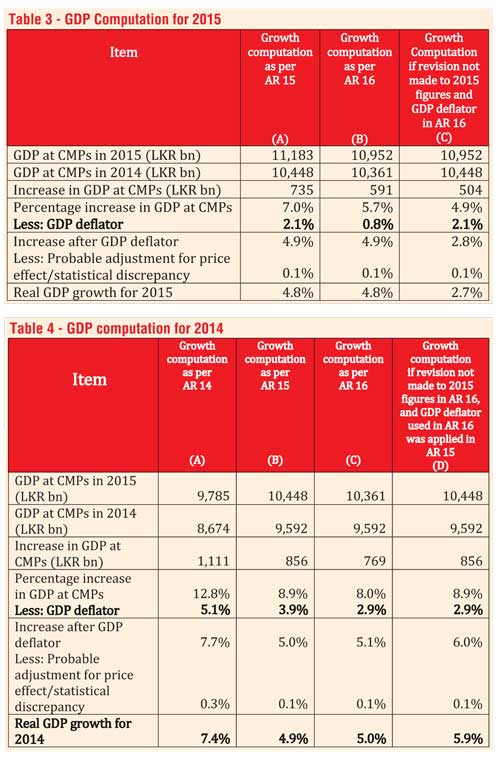

Accordingly, the GDP deflator for 2015 has been revised down from 2.1% (as announced in AR 15) to 0.8% for 2016, while the GDP deflator for 2014 has been revised down yet again from 3.9% (as announced in AR 15) to 2.9% in 2016. Incidentally, the revision in the GDP deflator for 2014 was the third occasion in 3 years that the GDP deflator has been revised in respect of 2014: from 5.1% in 2014, to 3.9% in 2015, to 2.9% in 2016!

It is also worthy to note that, with the application of the adjusted GDP deflator values, real growth for 2015 has been maintained almost miraculously at the same value of 4.8%, even after the starting and ending values of GDP at CMPs have been changed quite significantly. Please see Table 3. For comparative purposes, Column (C) shows the change in real GDP that would have taken place, if these “adjustments” had not been carried out.

It would be noted that the quiet intervention to “adjust” the real growth to 2014 is also somewhat similar, although equally controversial. As shown in Column (B) of Table 4, the re-statement and revision of the real growth for 2014 was effected by applying the same dubious methodology. Here too, it would be noted that, while the average CCPI for 2014 remained at 3.3%, the GDP deflator was first reported at 5.1% in AR 14, and later changed to 3.9% in AR 15, and finally changed to 2.9% in AR 16.

For comparative purposes, Column (D) indicates what the real growth for 2014 would have been, had the GDP deflator used in the computation for AR 16 been applied in AR 15. In such an event, the real growth for 2014 would have been recorded as 5.9%, and not 4.9%. This computation shows the shocking manner by which the GDP deflator has been misused in order to “massage” the growth numbers to achieve the desired results.

Sadly, in recent times, the Sri Lankan authorities seem to have perfected a shocking series of “creative practices” and “number massaging techniques” in order to achieve politically and/or economically desired results. Needless to say, these “creative” adjustments make a mockery of the computation of GDP in Sri Lanka since the underlying intention seems to be to “produce” figures and numbers that are desired, and not those that are based upon the hallowed principles of consistency, legitimacy and credibility. This cavalier, partisan and reckless attitude would undoubtedly be a cause of grave concern to all stakeholders, particularly because if this situation were to continue, stakeholders of the Sri Lankan economy would no longer be able to place reliance on the accuracy and objectivity of the information and statistics published by the authorities.

Epilogue 1

The “tall” story…

Little Sunil was 100 centimetres tall on his 10th birthday. When he reached his 11th birthday, he had grown to be 102 centimetres. However, his father, Nimal had taken a bet with his neighbour, Piyal, a year earlier, that Sunil would grow at least 4% by the time he reaches 11.

So, what does Nimal who works in the Ministry of Finance, do? Nimal simply “adjusts” Sunil’s height on his 10th birthday to 98, expresses the increase in height relative to the revised base height as 4 centimetres, and claims Sunil has grown by 4 centimetres, or 4.1%!

Piyal is baffled, but does not notice or understand this “adjustment”, and Nimal wins the bet.

For his brilliant statistical ability, Nimal is named the Statistician of the Year by a prestigious newspaper company!

Epilogue 2

An extract from the Counterview Magazine of 4 March, titled ‘Real GDP growth 5%; Modi Govt. “doctored” data to arrive 7% rate, revising base figure, ignoring demonetisation’.

Prof. Prabhat Patnaik, one of the topmost Indian economists, has revealed that the Government of India’s Central Statistical Organisation (CSO), while announcing 7% gross domestic product (GDP) growth for the third quarter of 2016-17 (October-December 2016), did this by “revising downwards the base upon which this growth-rate is calculated”.

Calling it a clear case of “doctoring of statistics on the part of the CSO at the behest of the Government”, Patnaik says, this manipulation automatically led to a surprise “jump in the growth rate from 6.2 to 7%”, a point noted by no other than Soumya Ghosh, who is the chief economic advisor of the State Bank of India….

The base on which this was calculated was revised downwards not once but thrice, Prof. Patnaik says, and the whole idea was to arrive at 7% rate of growth….

Concludes Prof. Patnaik, “The 7% growth rate for the third quarter of 2016-17 claimed by the government which would come down to 6.2% if the base figure is not adjusted, would come down further if the under-representation of the informal sector in GDP estimates is taken note of, and would come down still further if the effect of arbitrarily large net indirect tax collections is additionally taken note of.” In fact, it would have been 2% lower – around 5%”.... See full article at: http://www.counterview.net/2017/03/real-gdp-growth-5-modi-govt-doctored.html

(The writer is former Governor, Central Bank of Sri Lanka.)