Tuesday Jun 16, 2026

Tuesday Jun 16, 2026

Tuesday, 9 May 2017 00:20 - - {{hitsCtrl.values.hits}}

The guidelines for Public Debt Management, published jointly by the World Bank and the International Monetary Fund (IMF) defines public debt management as the process of establishing and executing a strategy for managing government debt in order to raise the required amount of funding at the lowest possible cost over the medium to long run, consistent with a prudent degree of risk.

Over the years, the practice of public debt management has undergone numerous changes. Governments around the world have implemented many structural reforms in the area of public debt management with the aim of reducing vulnerability of government balance sheets to financial shocks. The experience from those countries suggest that such reforms have resulted in increasing its resilience to financial shocks and improving the efficiency of debt management operations. The World Banks has provided technical assistance to many member countries in overcoming the systemic weaknesses of public debt management.

Review of examples of such reforms and their subsequent benefits to those countries are helpful for us in understanding the need of undertaking reforms in public debt management. A representative from the Colombian Government Treasury, made a presentation at the 2017 Government Bond Market Conference, held at the World Bank headquarters in Washington DC and shared their experience on the above subject. (Online link to the presentation: http://pubdocs.worldbank.org/en/805121493405002015/bonds-conf-2017-Ana-Carolina-Diaz-The-Design-of-issuance-calendars-and-the-impact-on-secondary-markets-Colombia.pdf).

Accordingly, this paper intends to study the lessons that are to be learned from the experience of public debt reforms in Colombia. The Republic of Colombia is a country situated in the northwest of South America. Sri Lanka and Colombia share several similarities in terms of being under colonial rule, tropical weather and a democratic government with presidential system.

Colombia went through a series of improvements in their system of public debt management with technical assistance from the World Bank. Prior to the said reforms that had started in 2003, the country had inherited fragmented institutional arrangements for public debt management – with responsibilities divided between the Ministry of Finance and the Directorate of Public Credit.

Formalising the institutional framework of the Debt Management Strategy

An evaluation of the existing institutional arrangements carried out by experts from the World Bank had uncovered that the country had lacked an overall strategy for domestic debt market development, including the issuance of both short and long-term debt, because each directorate had different priorities.

On the advice of the World Bank, Colombia undertook consolidation of debt management and treasury functions in order to reduce the coordination and information requirements, eliminate the duplication of functions, strengthen accountability and thereby facilitating the development of a strategy for managing the aggregate domestic debt portfolio through the formation of a debt management unit (DMU) named as the Directorate of Public Credit and National Treasury.

Medium-Term Debt Management Strategy (MTDS)

According to the World Bank, the Medium-Term Debt Management Strategy (MTDS) is a plan that the government intends to implement over the medium term (three to five years) in order to achieve a composition of the government debt portfolio that captures the government’s preferences with regard to the cost-risk tradeoff. Objectives of public debt management is to meet the financing needs and payment obligations at its lowest possible cost consistent with a prudent degree of risk.

The MTDS plan helps to document and establish an operational framework for achieving the above objective. The Colombian MTDS focuses on achieving a public debt portfolio comprising 65% of local debt and 35% of foreign currency debt which will optimise the overall cost of the debt portfolio while minimising the market risk (both interest rate and exchange rate) and refinancing risk. It further focuses on avoiding the bunching of debt maturities while maintaining the upper bound for annual amortisations at 10% of total outstanding debt.

Publishing of the Auction Calendar with issuance of Benchmark Securities

The Debt Management Unit (DMU) publishes an auction calendar for the issuance of domestic debt instruments on the website of the Ministry. This auction calendar is a time schedule of all the auctions that will be realised during the following year. At the beginning of the year, the On-The-Run Bonds are announced to the market (Primary Dealers or PDs), while the amount per auction (not per bond) is announced to the market at the beginning of every quarter.

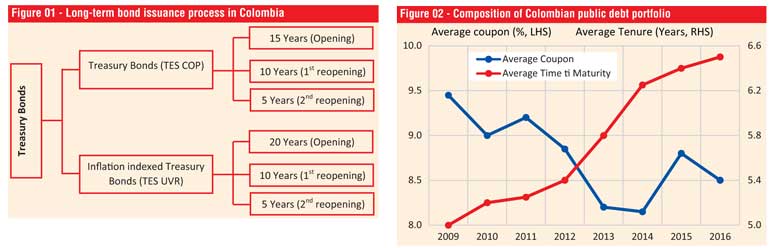

DMU issues two type of long term bonds in local currency – plain vanilla treasury bonds (TES COP) and inflation indexed treasury bonds (TES UVR). Issuances of bonds are limited to benchmark securities in each category - i.e. 5, 10 and 15 years for bonds denominated in local currency (Colombian Pesos – TES COP) and 5, 10 and 20 years for bonds denominated in Units of Real Value (TES UVR). The issue of benchmark securities not only enhances liquidity in the secondary market but also avoids the bunching of future maturities of public debt in a particular year.

The published auction calendar and the issuance of the public debt according to the published calendar enhances the transparency, predictability and the consistency of issuance of public debt. This issuance practice has reduced unwanted speculation about the amounts and bonds issued at the auction, while helping market participants (PDs) to prepare for the next auction by selling down the portfolios.

Reintroduction of treasury bills

With the resumption of issuing treasury bills, the Central Bank of Colombia (Banco de la República) discontinued the issuance of securities for monetary control purposes. The objective of the issue of treasury bills is to fulfil the requirement of a short term treasury instrument in the market.

Liability Management of Public Debt

Liability Management is the process of restructuring outstanding borrowing(s) in order to improve the composition of the public debt portfolio. The liability management function for both local and foreign denominated debt aims to improve and smoothen the maturity profile of public debt by extending the average life and minimising maturity concentration in specific periods.

Key liability management strategies such as bond Buybacks and Exchanges are widely used in the government securities markets for management of refinancing and liquidity risks. This is closely linked to the implementation of a benchmark issuance policy. Bond Buybacks enable issuers to retire an outstanding debt before its maturity date against a cash payment. Bond Exchanges achieve the same result but in combination with the issuance of new debt. Both transactions are liability management operations. They provide no additional funding, but they affect the composition of the debt portfolio by restructuring an outstanding debt.

These two functions are closely connected. On one hand, retiring illiquid off-the-run bonds from the market offers additional issuance opportunities, which enables the faster building of benchmarks. On the other hand, the gradual buyback of bonds as they approach maturity mitigates the refinancing risk and, as a result, enables the issuance of benchmarks of a larger size. The principal functions of bond buybacks and exchanges are to enhance market liquidity and to mitigate refinancing risks. Switching of debt with market participants have paved the way for Colombia to increase liquidity of securities in the secondary market and reduce refinancing risk.

Lesson to Sri Lanka

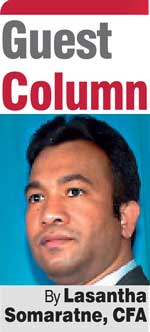

The reforms in public debt management has led to deepen the domestic government bond market in Colombia. It further resulted in broadening and diversification of the investor base for government securities through an increase in foreign investor participation in the government securities market. As a result, the share of foreign investors in Treasury Bonds had increased from approximately 6% in 2011 to 18% in 2015

The institutional framework and structure of public debt management in Sri Lanka is at least a decade behind countries in the peer group due to slow or no progress in reforms. As a result, the country has inherited unmanageable levels of debt, high interest cost and a fragile institutional framework which is not capable of dealing with challenges emerging in public debt.

The reforms in public debt could facilitate reaching towards the objective of meeting the financing needs of the government at the lowest possible cost over the medium to long term, consistent with a prudent degree of risk and thereby achieving fiscal consolidation. The outcome of the public debt reforms of Colombia are encouraging and such experience should be used as case studies and guidance for undertaking reforms in our public debt management.

(The writer is a CFA charterholder with local and international capital market experience. The views and opinions expressed in this article are those of the writer and do not necessarily reflect the official policy or position of any institution.)