Thursday May 14, 2026

Thursday May 14, 2026

Thursday, 20 April 2017 00:00 - - {{hitsCtrl.values.hits}}

The proposed Public Private Partnership (PPP) for the Hambantota Port is under heavy criticism in the media as means to ward off the purported economic crisis; referring to the increase in the public debt stock during the last two years.

This comparison of the increase in public debt stock is misleading, as the increase in the debt stock during 2015 was largely due to the revaluation of foreign loans – it has no economic meaning since foreign loans are serviced at different points in time at the prevailing exchange rates.

Foreign loans are repaid using foreign currency proceeds available during the year of payment and conversion to local currency is only for record keeping purposes. Hence, the accounting valuation of foreign debt stock is meaningless since those figures are compared internationally in USD terms.

According to the provisional data, the public debt stock of Sri Lanka was Rs. 9,387 billion on 31 December 2016. The public debt stock has grown by Rs. 1,996 billion during the last two years. However, nearly Rs. 500 billion of the above increase was a result of the revaluation of foreign debt stock.

If the depreciation component of the exchange rate is adjusted, the increase in borrowings during 2015 and 2016 was Rs. 1,490 billion. This compares to Rs. 1,391 billion increase in public debt during 2013 and 2014. Corresponding total Government expenditure had increased by nearly Rs. 1,033 billion during the past two years.

Government expenditure during the past two years contained interest payments of Rs. 1,121 billion for the loans taken by successive governments in the past. In addition, the Budget includes a large debt service cost of State agencies which remains out of the GoSL balance sheet.

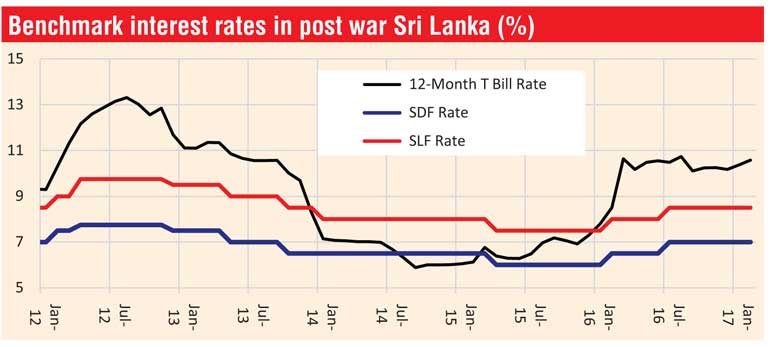

Due to an ever-growing public debt stock and gradual expiry of grace periods on loans, the interest cost of the Government is on the rise. There is no unusual increase in the interest rates which could increase debt service costs during 2015 and 2016 as illustrated in the graph, which shows the behaviour of key interest rates in post war Sri Lanka.

The GoSL is making every possible attempt to deleverage without compromising the required investments into basic infrastructure such as roads, power, water and sanitation. Public-Private Partnerships which have been successfully implemented elsewhere in the developing world, including neighbouring India, are a good alternative mechanism for funding infrastructure.

The PPP modalities such as concessionary agreements, Build-Operate-Transfer (BOT), Build-Own-Operate-Transfer (BOOT) and Build-Own-Operate (BOO) are used for new infrastructure developments. Management agreements, long-term leasing, concessionary agreements, and Takeover-Operate-Transfer (TOT) are utilised to cash-out existing infrastructure assets to raise further funding for new developments. These modalities help attract long term Foreign Direct Investment (FDI) inflows in to the country.

A national liability

In its current form, the Hambantota Port cannot be considered as a national asset and it is only a national liability without any real business operation or plans for such business operations in the future. Taxpayers take the burden of the maintenance of the port and service loans, hence it is not wrong to term it as a national liability.

The operation of the port was largely confined to RORO (Roll-On/Roll-Off) and revenue of the port was Rs. 2.4 billion in 2015. The construction of the port was apparently not based on proper evaluation of commercial feasibility and has no proper business plan to run a profitable port operation. The loans ($ 1.27 billion), obtained by the Sri Lanka Ports Authority (SLPA) for the construction of the port, are still within their grace periods and the SLPA will find it extremely difficult to service the debt when those loans become due for repayment.

The Government has chosen the best option to revive the operation of the Hambantota Port and allied infrastructure. The port requires a credible and internationally reputed port operator to attract regional transhipment cargo. Furthermore, it requires a large amount of FDI to set up manufacturing businesses in the surrounding area of the port to generate a sizeable load of local cargo. There are abundant examples in the region for such successful ports (i.e. Port of Tanjung Pelepas in Malaysia).

[The writer is a CFA charterholder with local and international capital market experience and a former Fund Manager at the Employees’ Provident Fund (of the Central Bank of Sri Lanka).]