Wednesday May 20, 2026

Wednesday May 20, 2026

Thursday, 29 September 2016 00:00 - - {{hitsCtrl.values.hits}}

The Federal Reserve System (the Fed) and Bank of Japan (BoJ), two of the main central banks in the world, announced their monetary policy changes on 21 September.

The Fed’s decision was a testimony that the central bank doesn’t want to upset market sentiment while Bank of Japan hinted that the innovative central bank will never be out of ideas.

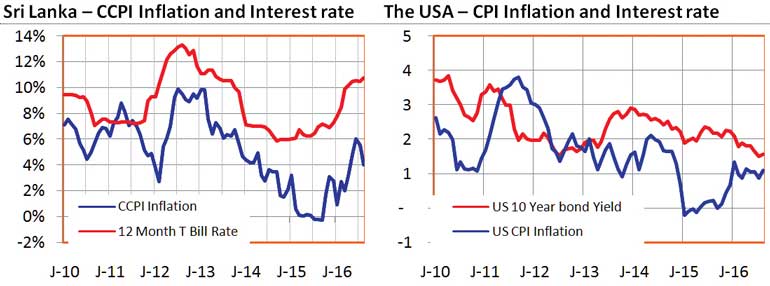

The BoJ initially took short-term interest rates in to negative territory in their fight against deflation and decided to experiment with a longer tenure – to anchor 10-year government bond yields near zero by fine-tuning its asset purchases.

The Fed by majority voting of Federal Open Market Committee (FOMC) decided to maintain the fed fund rate at current levels - target range for federal funds rate at ¼ to ½%. This indicates that the Fed would like to maintain the status quo for the time being. However, the Fed believes the case for an increase in the federal funds rate has strengthened.

Bank of Japan (BoJ)

In 2013, Haruhiko Kuroda, the former Head of the Asian Development Bank (ADB), took the helm of BOJ that was believed to be a traditional central bank. He was worried about the risk of deepening deflation and encouraged by the political popularity of Prime Minister Shinzo Abe, embarked on a program of aggressive policy innovations.

Despite the continued innovation in monetary policy, the BoJ thus far has failed to revitalise the long-term paralysis of the economy. The bank didn’t receive the much-anticipated political support through the third arrow of pro-growth structural reforms of the Japanese Prime Minister.

It should also be emphasised that the BOJ alone cannot combat the deflation war; the government, in the form of structural policy responses to lift potential growth rates should supplement the efforts of monetary authority.

The Federal Reserve

Bank (Fed)

The Fed, under the leadership of former Chairman Ben Bernanke who is a specialist in depression economics had engineered a series of unorthodox monetary policy actions to steer the world economy amidst the most difficult deflationary condition since the Great Depression in 1930.

Bernanke was a strong critique of Japanese policies, which led to decades of economic stagnation and lost of output. In response to criticism of a low interest rate regime maintained since 2008 to combat the financial crisis, he expressed that the best strategy for the Fed is to set short term interest rates at a level consistent with the healthy operation of the economy over the medium term admitting that the real, or inflation-adjusted interest rates (the market, or nominal, interest rate minus the inflation rate) which is most relevant for capital investment decisions is decided by a multitude of economic factors.

During the period of financial crisis, the monetary authorities pumped billions of dollars of liquidity into the financial system and averted otherwise a major financial disaster in modern human history. While doing so, the federal fund rate remained near zero from 2008 till December 2015. The Fed has not considered it appropriate to increase the interest rate yet.

Though inflation fear is widespread, the FOMC has decided that it is risky to let fragile growth fall apart. As an election year passes with divided politics on the surface, the Fed has decided to continue with its accommodative policies in filling the gap left by the slow responses and inaction by politicians worldwide. The Fed, for its part, is satisfied navigating as smoothly as possible until politicians step in to take effective action or the economy gathering momentum on its own.

The message carried by the decision of both central banks is that Central Banks cannot act within a vacuum completely ignoring the sentiments of the market as well as the near term economic wellbeing of citizens. The monetary policy should be innovative and adjusted in response to the changing dynamics of the economy.

While acting to achieve the long-term objectives of the price stability, central banks around the world have been trying to fill the gaps of volatile fiscal policy decisions by the lawmakers. They have been tasked to carefully navigate the economies through unchartered territories to achieve the economic wellbeing of the societies they represent.

(The writer is a CFA charterholder with local and international capital market experience.)