Thursday Jul 09, 2026

Thursday Jul 09, 2026

Friday, 17 January 2020 00:00 - - {{hitsCtrl.values.hits}}

For a small time investor starting to be involved in the Sri Lanka stock market this year, 2020, the starting point is to carry out research into the companies and to identify the opportunities available (or where we could have an arbitrage gain).

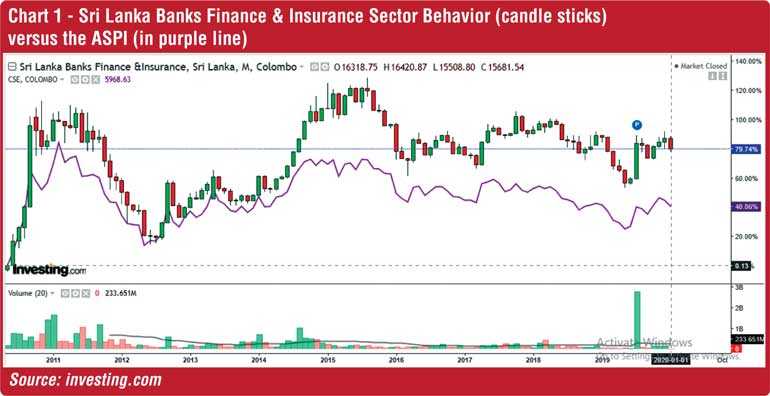

To start the journey, commence with the Banking, Insurance and Finance Sector since it is the sector which withstood all economic conditions in the past and performed better than the All Share Price Index of CSE. (Chart 1)

To narrow the discussion to the Banking sector, it is acknowledged and appreciated how the sector handled the roller-coaster journey in the last couple of years due to, constitutional crisis in October 2018, IFRS9 and BASEL III implementation in 2019, April 2019 situation, CBSL intervention of interest rate controls. Especially the BASEL III implementation had prompted all banks to hurry up and build Capital Conservation Buffer (CCB) even when the current Tier 1 and II capital held by banks are over and above the standards set by the BASEL III standards (which is found on page 2: https://www.cbsl.gov.lk/sites/default/files/cbslweb_documents/laws/cdg/Banking_Act_Directions_No_01_2016_capital_requirements_basel_III_e_0.pdf).

Concept failure by CBSL

Whilst it not the objective of sharing names of banks or the statistics which prove the point, a point to note is the way in which the CCB is raised by certain banks which can be manipulated to the major shareholders’ whims and fancies. Reason being that debenture issue was not open to public and a minimum contribution of Rs. 5 m was required.

But the Commercial Bank PLC came out with an issue allowing all to participate in multiple of 100X100 = 10,000 parcels. This allows the similar concept of a rights issue although these CCB qualified debentures issued by other banks take a different face.

As per the directive by CBSL, no further approval is required by the shareholders nor the debenture holders to convert the debentures to shares in the event a directive is given by the CBSL or the Monetary Board at an “objective pre-specified trigger point” at “non-viability”.

Details of the instructions can be found in the clause in Web Based Code 20.2.2.1.1.1. for (ATI) and 20.2.3.1.1.1 for Qualifying Tier II Capital Instruments.

Two grey areas

No place in the directive of CBSL or the communications issued by banks to shareholders have clarified/specified these two terms;

1. Objective pre-specified trigger point

2. Non-Viability

These debentures are being paid a fixed rate of interest way over and above the period five or seven year tenor instruments of banks and enjoy the option of being converted to ORDINARY shares at this so called trigger which is not known as at the time of the issue. What is non-viability can be different to different parties depends on what criterion that one will look at.

Concern

Almost all the banks’ shares are traded way below the NAV due to the hefty impairment charged by introducing the IFRS9 from 1 January 2019 onwards.

BASEL III, standard valuation basis or the advanced valuation for RWA (Risk Weighted Assets) had been practiced by banks way before official implementation by CBSL. Hence, PBV (Price to Book Value) is at near 50% except for COMB shares, since the director board composition and the shareholder mix is outstanding and commendable. Most of the other banks have a single or two majority shareholders (directly and indirectly), who influence the board at their discretion.

Year 2020 will be business as usual for all banks without abnormal provisioning, amidst the SME reforms introduced by the Government. Share prices will get adjusted to the normal PE ratio and will trade well above 80% of the NAV.

Therefore, these debentures issued with the ability to convert to ordinary shares will become like a call option available for those who subscribed to the debentures. SEC must take a list of debenture contributors and observe the trend, relationship of the debenture holders to the bank in question (all banks which issued Tier II debentures which can be constituted to CCB due to the conversion factor, unsecured and subordinated).

According to the banks’ communications the conversion of debentures to ordinary shares will be done based on the weighted average value of share traded in the last three months (preceding) from the trigger point.

What better time than this?

Due to the grey areas mentioned above a bank can say that they need more Tier I capital and otherwise they claim that the bank will be non-viable. Hence, get the consent (consent is a nice word instead of a directive) of the Monetary Board of the Central Bank to consider it as the so called trigger point.

Then what happens to the other shareholders and the value of shares? As per the directive there is no room for shareholders to contribute by way of rights issue in this instance to redeem the debentures once the trigger is made. Hence, these debenture issues can be another form of a rights issue to a chosen community for obvious reasons.

Caution!

This so-called trigger and the non-viability are extreme situations (for law abiding nations, ethical banks/regulators and practitioners of good governance will consider) which should not be played around, since it can lead to a bank run. But due to the able marketing and communication abilities of Sri Lankan people, even the worst case can be handled by stating it was just another incident for a better future.

I rest my argument and urge the CBSL and the SEC to look into this matter of not defining the Objective pre-specified trigger point and Non-Viability as stated above for the sake of the minority shareholders’ interest (to build a credible stock market) before it is too late after the “trigger!”.

(The writer can be contacted through email [email protected].)