Wednesday May 27, 2026

Wednesday May 27, 2026

Wednesday, 2 January 2019 00:00 - - {{hitsCtrl.values.hits}}

We are at the beginning of a new year with new hopes. As a country, where are we now? What were our achievements and what we missed in the previous year? What would be our targets for the New Year and what would be the possible challenges?

Everyone is curious about these matters at the beginning of every year. Thus, the purpose of this article is to review the economic performance of Sri Lanka in 2018 and discuss the possible challenges of the New Year. Further, the article attempts to forecast the performance of major economic variables in order to facilitate for informed decisions of major economic players such as investors, savers, consumers, producers, etc.

SRI LANKA IN 2018 Overall economic performance

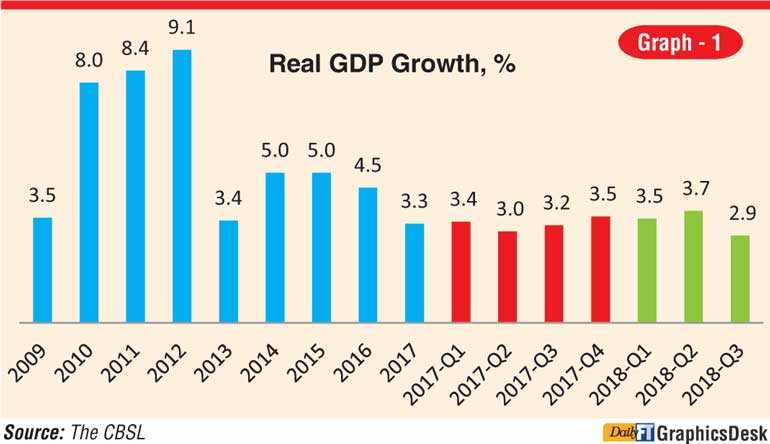

Sri Lanka’s economy grew only by around 3.1% in 2017 well below the envisaged levels of the Central Bank of Sri Lanka (CBSL), as a result of disruptions from droughts and floods, and policy tightening. However, the CBSL expected the economy to be recovered in 2018 and will grow by 4.5%.

The Asian Development Bank (ADB) and International Monetary Fund (IMF) also initially forecasted a growth of 4.2% and 4.8% respectively for the Sri Lankan economy for 2018, with the possible recovery of agricultural sector which was badly affected by natural disasters in 2017.

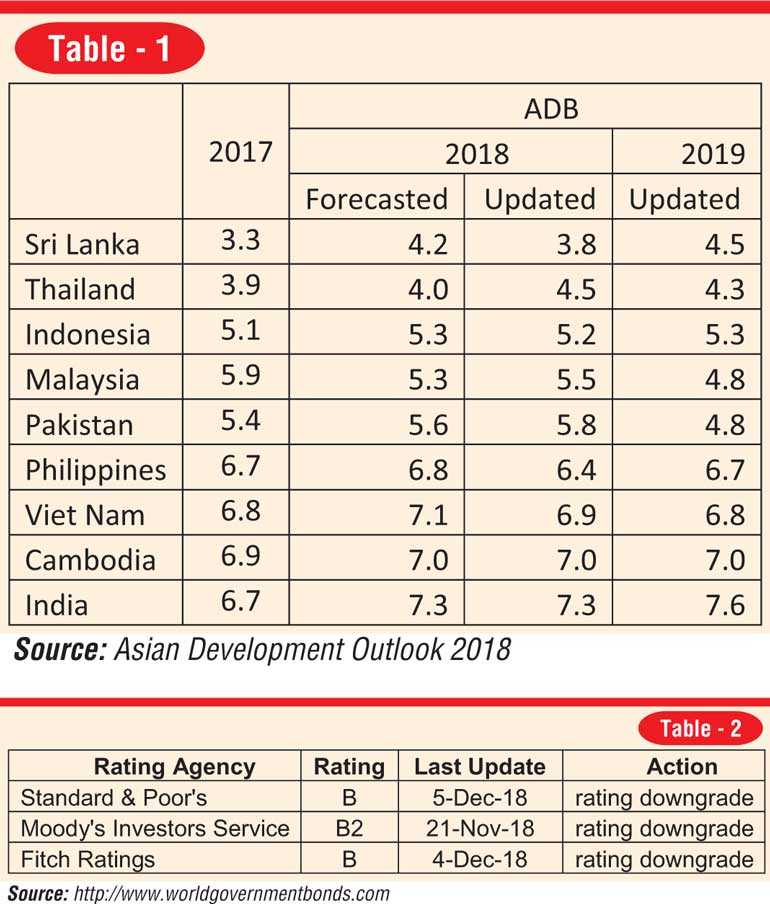

However, according to the Department of Census and Statistics the economy grew only by 3.3% during the first nine months of 2018 and thus the CBSL downgraded the country’s growth projections for the year in several times, following quarterly economic performance (Graph 1), to be 3.7% from its original stance. In addition, the ADB and the IMF declined their forecasts on Sri Lanka’s growth to 3.8% and 3.7% respectively for 2018, considering unfavourable domestic and external developments.

Sri Lanka’s economic performance in 2018 is not satisfactory relative to its regional peers, countries in South Asia and Southeast Asia (Table 1). Almost all the counties recorded over 5% growth in 2018. Philippines, Viet Nam, Cambodia and India managed to continue their robust growth performance in 2018 as well.

The reasons for the subdued economic performance in Sri Lanka could be weak domestic demand, continued tightening in monetary condition as well as Government consumption spending, stagnant fixed investment, and lower net exports. The tightening monetary policy leads to drag down domestic demand as well as investment. Further, inconsistent economic policies driven by political instability may have affected in delaying private and public sector investment which are key drivers of economic growth.

Moreover, the Government initiated certain structural reforms supported by the International Monetary Fund (IMF) to address the key structural problems in the economy such as twin deficits. Some measures include the launching of the new Inland Revenue Act which leads to revenue-based fiscal consolidation and introducing an automatic fuel pricing formula towards reducing fiscal risks from State-Owned Enterprises (SOEs).

During the year, the CBSL allowed for greater exchange rate flexibility while strengthening reserve buffers to ensure resilience against external shocks. Further, in September 2018, the Government launched ‘Vision 2025’. The program planned to address constraints to growth over the next three years, consistent with IMF program. These structural reforms may have affected the economic performance in the short-term, though they have constructive impact on medium to long term on overall economy.

Monetary sector

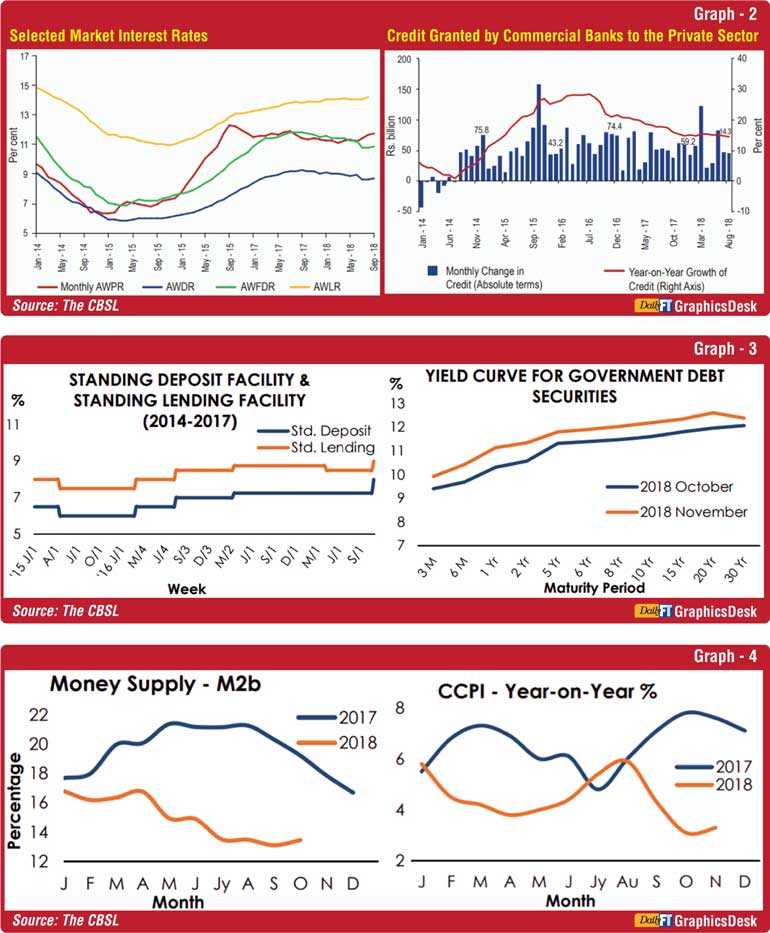

The tight monetary policy stance which prevailed in 2017 continued in 2018 as well. Following the lacklustre economic performance in the first quarter in 2018 relative to the respective period of the previous year, the CBSL decided to relax monetary policy stance moderately in April/2018. However, the Monetary Board increased the Standing Deposit Facility Rate (SDFR) by 75 basis points to 8% and the Standing Lending Facility Rate (SLFR) by 50 basis points to 9% in November/2018.

In consistent with the Central Bank’s policy rates, the yields on Government securities as well as most other market interest rates have stabilised at high levels throughout the year (Graph 2 and 3). The growth rate of credit granted by commercial banks to the private sector decelerated responding to the high interest rates (However, credit to the private sector increased in absolute terms despite rising interest rates).

Moreover, reflecting the impacts of the tight monetary policy stance, money supply decelerated gradually along with the inflation (Graph 4). The headline inflation remained in low single digit levels during the year due to continued slowdown in food inflation and low money supply in the market. This resulted to a rise in real interest rate in the economy.

External sector

External sector performance was not impressive in 2018, except the earnings from tourism. The trade deficit widened to $ 8,857 million during the first ten months in 2018, ballooning by 16.7% in comparison to the corresponding period of 2017, due to a higher growth in import expenditure alongside a marginal growth in exports. During the period, export earnings improved only by 5.1% while import expenditures increased by 10.3%.

Strengthening the current account, earnings from tourism increased by 10.6% during the first 10 months of 2018 and amounted to $ 3,496 million. It is noteworthy to mention here that, in October 2018, the adventure experts at Lonely Planet named Sri Lanka as the No. 1 country to visit in 2019. Meanwhile, a marginal decline (0.5%) was recorded in foreign workers’ remittances in first 10 months of the year. $ 5,876 million was received as remittances.

Foreign investments outflows from the Government securities market were observed throughout the year and totalled to $ 640 million during the first 10 months. It is reported that the Colombo Stock Exchange (CSE) has recorded a net foreign outflow of Rs. 27.50 billion (year to date up to 28 December 2018), against the net foreign inflow of Rs. 17.65 billion recorded in 2017.

As discussed above, due to widening trade deficit and investment outflows and also tightening US market condition and the effect of speculation in the domestic market, the Sri Lankan rupee depreciated by around 16% against the US$ during 2018, relative to a 2% depreciation reported in 2017.

The CBSL largely allowed the market to determine the exchange rate with a less intervention to defend the LKR by supplying foreign exchange out of its official international reserves, following many regional peers. Nevertheless, gross official reserves amounted to $ 7.0 billion at end November 2018, providing an import cover of 3.7 months comparative to the 4.6 months at end-2017.

Fiscal sector

As a result of the Government’s effort for fiscal consolidation, during the first eight months of 2018, the overall budget deficit declined to 3.5% of the estimated GDP from 4% in the corresponding period of 2017. The total expenditure and net lending declined to 12.1% of GDP while Government revenue dropped to 8.6% of GDP.

The decline in overall budget deficit is in line with Quantitative Performance Criteria (QPC) set under the Extended Fund Facility of the International Monetary Fund (IMF-EFF). Though the decline in public investment reduce budget deficit, it may have affected negatively towards economic growth in the country.

International ranking and foreign relations

The country’s position according to different international rakings in 2018 showed a mixed result. Internationally-recognised indexes such as the Doing Business Index, Global Competitiveness Index, Rule of Law Index, and Credit ratings are considered here as they are important in attracting Foreign Direct Investments (FDI) and Foreign Portfolio Investment (FPI) to the country.

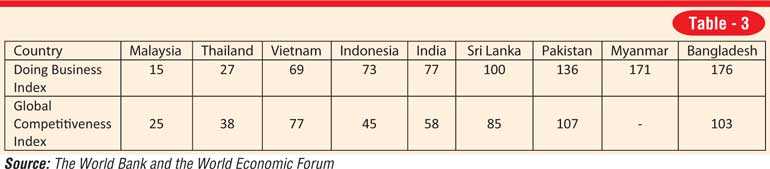

As per the World Bank’s Doing Business Index, Sri Lanka ranked at 100 among 190 economies in 2018 climbing 11 steps from its previous position due to improvements in sub-sections such as dealing with construction permits, registering property, paying taxes, and enforcing contracts. However, Sri Lanka slipped four steps according to the Global Competitiveness Index calculated by the World Economic Forum and positioned at 85th in 2018.

Notably, three major Credit Rating agencies, Standard & Poor’s, Moody’s Investors Service, and Fitch Ratings, downgraded Sri Lanka during the year (Table 2), though the CBSL said that the ratings are based on uncorroborated facts on the country’s macroeconomic fundamentals. As summarised in Table 3, Sri Lanka’s position according to the said international rakings is not attractive relative to its regional peers.

Moreover, as per the World Justice Project’s Rule of Law Index 2017-2018, Sri Lanka ranked at 59th place, improving nine steps. It is also said that Sri Lanka ranked at 100th position as per the Global Gender Gap Index with 0.676 points in 2018. The Index benchmarks national gender gaps on economic, education, health and political criteria, and provides an effective comparison across regions and income groups. Though the country raised nine notches in the index, it is still below the global average.

Meantime, Sri Lanka and Singapore signed the Sri Lanka-Singapore Free Trade Agreement (SLSFTA) which is a comprehensive Free Trade Agreement covers goods, services, e-commerce, telecommunications, foreign direct investment, intellectual property and public procurement, on 23 January 2018. The Agreement was brought into operation with effect from 1 May 2018, despite many concerns are still being discussing.

Stock market performance

The Benchmark All Share Price Index (ASPI) has made a 4.97% loss in 2018 relative to 2.3% gain reported in 2017 (Graph 5). The S&P SL 20 index, which features the CSE’s 20 largest and most liquid stocks, has also moved down consistently, making a 14.63% loss for 2018.

Historical trends show that there is an inverse relationship between interest rate and stock market index in Sri Lanka as it is natural that investors shift from risky equity securities to comparatively less risky fixed income bearing financial assets such as Government and corporate debt securities and fixed deposits when their returns are moving up.

Market was less active in 2018 in terms of turnover compared to the previous year. The daily average turnover amounted to Rs. 788 million at the end of the third quarter of 2018 relative to Rs. 915.3 million in 2017. According to market analysts, lack of local investor participation was observed during the year and foreign investors played an active participation in the market in recent years. Relatively small size of the market (20.7% of GDP at the end of September 2018), less liquidity and high transaction cost are the major challenges of the Sri Lankan stock market.

The Securities and Exchange Commission (SEC) and the Colombo Stock Exchange (CSE) initiated new SME Board titled ‘Empower’ in July/2018 in order to empower the country’s economic backbone, Small and Medium Enterprises (SMEs) and improve the size of the market.

2019 outlook

The economy is expected to grow by 4.5 and 4.3% in 2019 according to the ADB and IMF’s forecasts respectively. The CBSL’s vision towards acceleration of economic growth was clearly indicated on its Monetary Policy Review: No. 7 – 2018.

“In order to accelerate growth on a sustainable basis, it is essential that growth enhancing structural reforms are carried out within a coherent and transparent framework, rather than relying on unsustainable short-term monetary and fiscal stimulus, which leads to overheating of the economy.”

National level elections will probably be scheduled in 2019. As none of the major political party has a clear majority in the parliament to form a strong government and none of the major political party clearly nominated a presidential candidate, direction about future political leadership is unclear.

Further, an uneasy condition between the Prime Minister and the President could weaken economic policies. In this scenario, large scale public and private sector investments are getting delayed, weakening economic growth. Therefore, in this scenario it is not easy to reach the expected economic growth of 4.5% in 2019.

Moreover, whoever will come to power based on future elections will not be able to reverse recent reforms or to halt implementation of future reforms which address structural problems of the economy as such attempt would lead to further deteriorate economic condition and downgrade credit ratings. In addition, it would limit the Government’s access to global capital markets, curtail foreign direct investment inflows to the country and reduce funding from international lenders.

It is reported that Sri Lanka will have $ 4.2 billion in debt service payments in 2019, $ 3.7 billion in 2020, $ 3.3 billion in 2021 and $ 3.7 billion in 2022, adding up to a total of $ 14.9 billion during the four years. The major challenge in the New Year and years after is to refinance large volume of foreign debt settlements because of increasing Government’s debt refinancing cost of external sources due to poor credit ratings and associated political risk.

The Fed did its fourth rate hike of the year in December 2018 by raising policy rates from 2.25 to 2.5%. Their insights suggest that there could be further rate hikes in next year. Thus, it seems that the US monetary policy becomes tighter and the dollar strengthens further. As a result, emerging economies like Sri Lanka will be badly affected in 2019 as well. Consequently, the funds outflow from the domestic financial market increase the pressure on the exchange rate and foreign exchange reserves. In this scenario, further depreciation in currency can be expected in 2019 at a moderate level because the CBSL has limited capacity to intervene the market as it has limited reserves.

The impact of currency depreciation (around 16%) in last year is yet to emerge in 2019. Not only the Sri Lankan Rupee, but many currencies in emerging economies depreciated due to the impact of the Fed rate hike and strengthening US Dollar. However, Sri Lanka is more vulnerable for currency depreciation as it consumes more than what it produces and it holds higher external debt stock. The impact of currency deprecation could be reflected through inflation soon.

As a consequence of rising interest rate and subdued economic growth, the non-performing advances of the banking sector have been inclining rapidly over the past period. This trend may continue in 2019 as well if the economy will not recover at an acceptable pace, challenging the stability of the financial system of the country.

Finally, I wish to conclude the article with the following paragraph which quoted from a newspaper article written by Dr. W.A. Wijewardena, a former Deputy Governor of the CBSL and a renowned commentator of economic affairs (http://www.ft.lk/columns/Economy-at-a-crossroads----The-way-out-for-Sri-Lanka/4-669428). The paragraph explains remedies for many economic problems that Sri Lanka is currently facing: “Unless it attains an economic growth rate of about 9% per annum in the next 15-year period, it is unlikely that it will be able to beat the middle income trap. The way to do so is to produce for a market bigger than the market in Sri Lanka and supply goods that are demanded by that market. It requires the country to convert its production system from a simple technology based one to a complex technology one and join the global production sharing network to keep its presence in the market.“

(The writer is a visiting lecturer at University of Colombo and IPM and can be reached via email [email protected].)