Monday Jul 13, 2026

Monday Jul 13, 2026

Wednesday, 13 June 2018 00:00 - - {{hitsCtrl.values.hits}}

To facilitate Foreign Direct Investment (FDI), Sri Lanka launched last week an innovative online one-stop shop to help investors obtain all official approvals. To mark the occasion, this blog series explores different aspects of FDI in Sri Lanka. Part 1 (see http://www.ft.lk/columns/Five-reasons-why-Sri-Lanka-needs-to-attract-FDIs/4-656109) put for the five reasons why Sri Lanka needs FDI. Part 3 will relate how the World Bank is helping to improve Sri Lanka’s enabling environment for FDI

Sri Lanka and foreign investments read a bit like a hit-and-miss story. But it was not always the case.

Before 1983, companies like Motorola and Harris Corporation had plans to establish plants in Sri Lanka’s export processing zones. Others including Marubeni, Sony, Sanyo, Bank of Tokyo and Chase Manhattan Bank, had investments in Sri Lanka in the pipeline in the early 1980s.

All this changed when the war convulsed the country and derailed its growth. Companies left, and took their Foreign Direct Investments (FDIs) with them.

Nearly a decade after the civil conflict ended in 2009, Sri Lanka is now in a very different place.

In 2017, Foreign Direct Investment (FDI) into Sri Lanka grew to over $1,710 billion including foreign loans received by companies registered with the BOI, more than doubling from the $801 million1 achieved the previous year.

But Sri Lanka still has ways to go to attract more FDI.

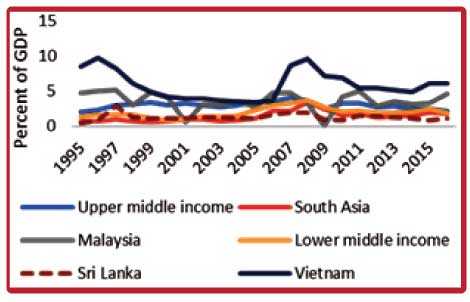

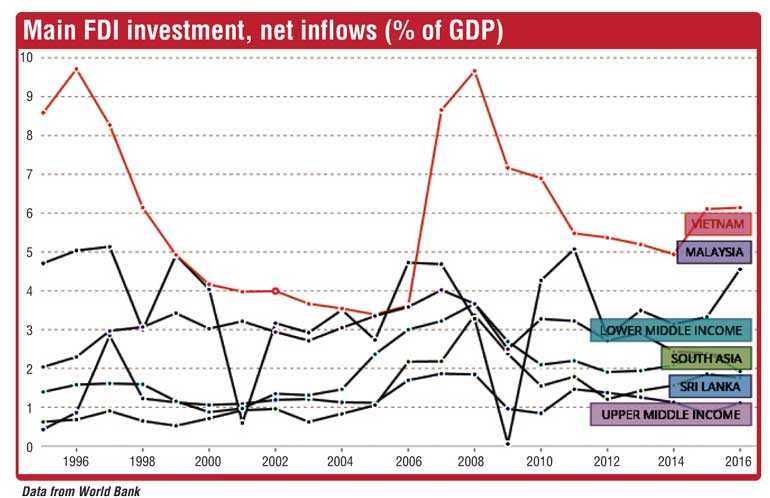

As a percentage of GDP, FDI currently stands at a mere 2% and lags behind Malaysia at 3-4% and Vietnam at 5-6%.

More importantly, FDI into Sri Lanka has been skewed away from high value-added global production networks. And currently the larger share of FDI inflows have been focused on infrastructure.

While they may boost jobs and growth temporarily during the construction period, these investments have little long-term impact. Compare this to a factory or a new IT service firm which would employ people as long as it makes profit, and export, pay taxes, and contribute to Sri Lanka’s growth for decades.

Moreover, high infrastructure FDI relies on few and large infrastructure deals that are unlikely to be replicated and sustained over time.

On the other hand, manufacturing and services hold a better promise for the long run, but even there, a large share of FDI is related to traditional sectors and local market-oriented activities with low value-added, where productivity gains are small.

To keep and increase FDI flows, Sri Lanka will need to make concerted and ambitious efforts to address gaps and play to its strengths.

Simply put, Sri Lanka can improve FDI by creating a more hospitable environment for investments. Taking steps in this direction is essential for domestic investment as well, not only FDI. And while the government has already begun targeting problem areas, much more is needed.

To that end, here are six ways Sri Lanka can improve FDI:

Reworking trade policy

Reforms in Sri Lanka’s trade policy saw eliminations or reductions of some 1200 para-tariff lines in late 2017, and further liberalisation is expected with the budget in 2018 and beyond to boost trade. More trade will help diversify the economy and exports, and lift a burden off of the public sector to drive growth. It can also actively promote technology absorption, skill upgrading, and increased competitiveness; workers, consumers, producers and the state will benefit in the long-run as a result.

Improving logistics and trade facilitation

Sri Lanka can leverage its unique location and trade agreements to overcome the dis-economies of its small scale. The Colombo port, which already sees 80% of its volume come from trans-shipment cargo, is poised to grow. However, Sri Lanka cannot take its position for granted with high growth in other ports in Pakistan and India.

Another way to compete is on speed and cost of trade processing. While domestic logistics are inefficient, internationally Sri Lanka is performing better. Currently, it ranks 57.7 out of 100 on the BMI Logistics Risk Index, and places 15th on the UNCTAD Liner Shipping Connectivity Index, which ranks countries according to their level of connectedness to international maritime networks.

The per-container cost for exporting and importing to and from Sri Lanka are much lower than the South Asia average but not at world class level (respectively, $ 560 and $ 690 – South Asian average is $ 1,923 and $ 2,118, 2015 data). To go the extra mile to a regional logistics hub, the government has started reforms including establishing a Trade Information Portal and the National Single Window which will streamline trade processing across the 20 plus agencies involved.

Promoting investments and enabling regulations while avoiding policy uncertainty

The island was ranked 111th out of 190 economies in the Ease of Doing Business index 2018which shows opportunity for improvement. The Government has carried out some focused reforms since 2016 to improve investment climate, and with the expected lag, reforms are cropping up. In 2017, trade across borders was made  more efficient, and this year improvements are expected relating to starting a business, property registration and construction permits.

more efficient, and this year improvements are expected relating to starting a business, property registration and construction permits.

Reforms are needed to address critical challenges in areas like land ownership. Currently, land is primarily State-owned in Sri Lanka, and land administration is weak and cumbersome. Anecdotal evidence points to discouraged FDI projects due to land issues. A large share of exports and most export innovation has occurred in a few Export Processing Zones, primarily in the Western Province, that are now generally at capacity, new SEZs are being planned.

Further, the BOI (Sri Lanka’s main FDI facilitation body) is transitioning towards modern investment promotion. Internal Revenue Act streamlined and improved the efficiency and transparency of incentives applicable to foreign investments in Sri Lanka. The Government is also liberalising the foreign exchange controls.

Policy uncertainty in Sri Lanka has proven daunting for investors, with a lack of information on regulations, high fragmentation in policymaking, frequent policy changes and slow policy implementation. Long-term policy strategies can serve as path-setters and expressed commitment to policy continuity in support of the GOSL vision.

Boosting innovation by way of competitive product and financial markets

Sri Lanka has seen little transformation in what it exports over the last 20 years. There’s been limited innovation and diversification even into “nearby product” space (new products closely related to existing ones) which is an easier step that happens organically with investment. This difficulty moving into new space has also left the country out of step with regional and global production networks. Where innovation exists, it is limited to a handful of industries. A national innovation strategy seeks to address gaps and support start-ups and SMEs.

Financial products have also remained behind the firm needs – e.g. SMEs need factoring and leasing, supplier finance mechanisms and export-related financial instruments. Now the Secured Transactions Act is being amended to allow one of those innovative products – the use of movable collateral.

Addressing labour related issues and getting women to work

Efforts are also needed to expand the pool of labour, relax constraints in labour laws such as long and costly termination procedure, and equip Sri Lankans with skills in demand in the marketplace. In particular, Sri Lanka can benefit tremendously from boosting its female labour force participation rate by addressing issues such as a lack of quality childcare, skills mismatch, unsafe transport and poor working conditions that keep women away from the labour force.

Sri Lanka could also ease the access of local companies to foreign expertise through introducing simpler visa procedures, which are currently complex and burdensome for foreign employees in Sri Lanka, limiting FDI especially for smaller ventures such as in tourism.

Providing enabling logistics and the right infrastructure environment

Nationally, Sri Lanka needs to address transportation shortfalls, which have seen inequitable development with some regions disconnected from growth, increasing issues of congestion, and poor safety for women. Different areas face different transportation gaps in roads, air travel and marine transportation infrastructure while rail infrastructure is outdated and limited, especially for the transport of goods. (Source: http://blogs.worldbank.org/endpovertyinsouthasia/six-ways-sri-lanka-can-attract-more-foreign-investments)

[The writer is a Program Leader for Sri Lanka and Maldives at the World Bank, responsible for financial markets, trade and competitiveness, macro and fiscal, governance, and poverty. Her operational work has focused on several financial sector areas of work (capital markets, access to finance for the poor, housing finance, and infrastructure finance and PPPs) as well as investment climate and institutions, trade policy and facilitation, and public sector institutions strengthening, and macro/fiscal policy. Before Sri Lanka, she has worked as Program Leader in Indonesia, with the World Bank CFO, as operational staff in South Asia, in the International Finance Corporation and in academia. Dr. Nenova has also published in leading US and international journals and co-created several innovative World Bank publications such as the Doing Business Report. She holds a Ph.D. in Economics from Harvard University.]

Footnotes

1These figures includes loans, excludes inflows to non-BOI companies and direct investment in listed companies in the CSE not registered with the BOI