Friday Jul 17, 2026

Friday Jul 17, 2026

Monday, 21 November 2022 00:30 - - {{hitsCtrl.values.hits}}

President Ranil Wickremesinghe

MP Patali Champika Ranawaka

|

An alternative report

This year, along with the presentation of the Budget 2023, the legislators were benefitted by the submission of a new report by a special committee setup under the National Council System in Parliament. That committee had been tasked to examine the state of the macroeconomy and come up with stabilisation policies as an independent thinktank of parliamentarians. The Committee had been headed by the opposition legislator Patali Champika Ranawaka who had been in this field for quite some time. The report is still not in public domain officially though there are some purported copies in circulation in the social media.

But a summary can be found by interested readers at https://www.newsfirst.lk/2022/11/16/parliament-committee-says-government-trying-to-restructure-domestic-debt/. A live discussion of the findings of the report was done by its head on TV and it can be accessed at https://www.youtube.com/watch?v=87rLctP7dZk&list=PLwBEINflt3JFzmeTDmw0a3YwYLMXbtRVb.

Need for being apolitical

Up to now, the legislators and the citizens were told of the state of the macroeconomy and its recent developments through a special publication by the Central Bank coinciding the presentation of the budget. The report titled Recent Economic Developments highlighted the state of the economy in colourful graphs, tables and special box articles which were all reader friendly. However, the report took an official line with a carefully selected vocabulary not to offend the government in power and, hence, could be branded as an extension of the budget submitted by the Minister of Finance.

Had Dr. N.M. Perera, the left-oriented Finance Minister of 1970-75, seen it, he would have been dismayed that the subsequent central bankers have chosen to ignore the wise advice he gave them in 1971 that he expected apolitical, objective, and impassioned reports from the central bank. In these circumstances, the special economic stabilisation report presented by the sub-committee will give an objective view of the state of the macroeconomy to legislators free from political hues. Since it adds to their knowledge, it is a welcome development.

Inflation by Shadowstats

One important benefit of the big data fields and advancements of information and communication technology has been the challenge it has posed to government monopoly over economic statistics and analysis. The availability of computing power with accuracy and the ability to collect data on a real time basis have enabled private parties to produce official statistics by using the methodologies adopted by official statistical bureaus. This has given birth to several new data platforms which can function as alternative data providers. This technology has specifically been used in computing inflation rates which can be tested with those published by official bureaus. One is the shadow government inflation numbers published by John Williams for use by individual subscribers (available at: http://www.shadowstats.com/alternate_data/inflation-charts).

They release real time inflation numbers by using the same methodologies adopted by official bureaus but based on price numbers collected from supermarkets at the points of sale. In the case of USA, the shadow inflation numbers are about two percentage points higher than the official numbers. In the case of Argentina, the gap is much wider than the gap one finds in USA. Shadowstats compiles alternative inflation data for almost all the countries and interested subscribers, mainly, existing, and prospective investors, can have access to them upon making the required subscriptions. What this means is that the global investor community does not want to trust the government data on inflation and other macroeconomic variables.

Hanke’s inflation dashboard

Another such inflation number which is very much demanded by interested investors is the inflation dashboard being operated by Johns Hopkins University’s Steve Hanke (see: https://www.cato.org/publications/commentary/hankes-inflation-dashboard-official-statistics-misrepresent-real-inflation). Normally, the central banks do not agree with him because the methodology adopted by him is not in line with the consumer price indices used by them for measuring inflation and taking appropriate monetary policy action. These consumer price indices are calculated by collecting the prices of selected consumer products from different markets and averaging the changes in the consumer prices considering the importance of those products in the monthly budget of a typical consumer, a process known as ‘weighting’.

But as a measure of inflation, it has two defects. First, it is the calculation errors. The whole process is like a black box where nobody knows what is happening inside except the output it produces. The second is that those consumer price indices measure only the price inflation relevant to consumption whereas a central bank should be concerned with the all the prices in an economy, namely, consumption goods, investment goods, and export goods which form the total aggregate demand of an economy. The inflation numbers released by

Shadowstats also suffer from these defects since they cover only the consumption goods. But the inflation dashboard compiled by Steve Hanke covers all these prices, since he computes inflation from the top by using the relationship between inflation and the exchange rate as modelled by Swedish economist Gustav Cassel in 1916 in his Purchasing Power Parity or PPP Theory. Hence, it is more representative of inflation being controlled by central banks.

Economic Stabilisation Committee Report

The Economic Stabilisation Committee Report has covered six major areas in its first report. All these six areas have been on critical economic issues faced by Sri Lanka today and therefore present an alternative view of analysis of same. These critical areas have been debt restructuring, shortage of medicines and its impact on healthcare system, the emerging food crisis, nutritional issues and the need for a social protection net, energy issues, and transport issues. To come up with its recommendations, the Committee had had wide consultations with experts in the respective fields. Going by the recommendations of the first report, one can conclude that the committee members had done their homework properly before confronting the relevant officials and experts.

This writer recalls that in 1950s, 60s, and 70s, veteran politicians like Dr. N.M. Perera and Dr. Colvin R. de Silva had in the same way done their homework and research properly before they stood in the well of the Parliament to deliver a speech. Reading their speeches in Parliament was like completing a credit course on a subject for a Master’s degree at a university. It is encouraging that professionalism in Parliament today had attempted to reestablish that rich old tradition.

Given the limitation of space, though all the six areas of reporting are relevant, I will concentrate on their findings on Sri Lanka’s debt profile and the work being done in the debt restructuring program.

Why should Sri Lanka borrow abroad?

Sri Lanka’s present debt profile is something that is being widely condemned by many today. Some even argue that Sri Lanka should not rely on foreign borrowings to steer through its economic growth path to prosperity. They even argue that ancient Sri Lankan kings like King Parakramabahu I could build reservoirs as large as oceans without relying on foreign financing, why should the independent Sri Lanka go for such an unsustainable option. What is forgotten here is that Sri Lanka needs to invest about 30% of its GDP year after year to maintain a safe economic growth record to become a rich country. If these investments could be entirely financed out of savings made by Sri Lankans – its government and its people – there is no necessity for Sri Lanka to borrow abroad. However, Sri Lanka’s domestic savings are less than the requirement and its government savings are in most years negative. Hence, to fill the savings-investment gap, Sri Lanka needs to rely on savings of foreigners.

King Parakramabahu I did not have this problem because the surpluses he made in his domestic budgets and in the balance of payments, he had a surplus that could be invested back in those giant irrigation schemes. The present debt restructuring issue has arisen because though Sri Lanka relied on foreign savings, it could not make those borrowings sustainable due to chronic and acute shortages of domestic as well as foreign exchange. Therefore, even after the debt is restructured, Sri Lanka’s debt issue is not solved because it will still have to tap foreign savings to continue its growth momentum which is now rephrased as seeking to become a rich country by 2048. For that, it needs to maintain an annual compound economic growth rate of above 8% which crucially depends on investing about 35-40% of GDP.

There is no evidence that in Budget 2023, a plan of action to generate these investment needs from local sources has been put in place. The budget speech as well as the Recent Economic Development Report of the Central Bank had failed to identify this crucial need. It has even been missed by the sub-committee on economic stabilisation and it is expected that it will cover this important aspect of long-term debt sustainability from a growth point in its future reports.

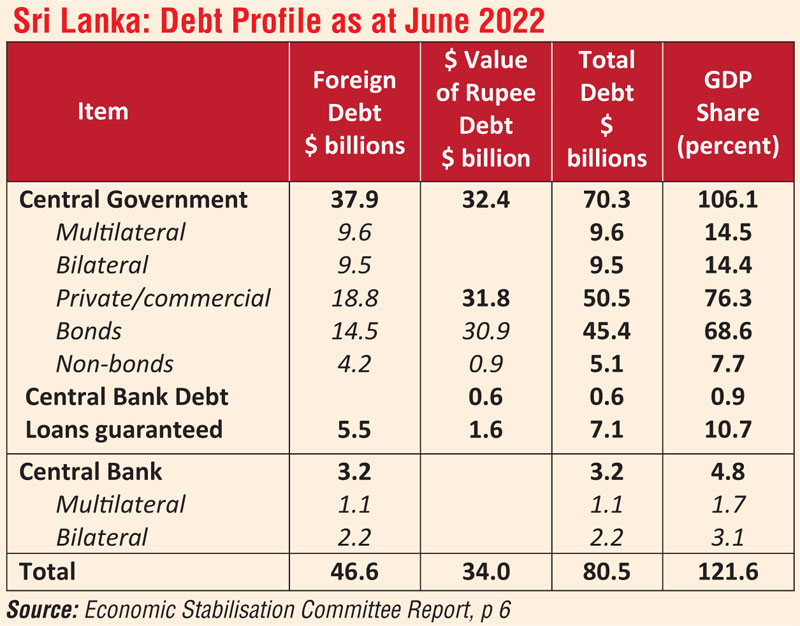

Sri Lanka’s debt profile

The Economic Stabilisation Committee has attempted to quantify Sri Lanka’s debt – in the case of foreign debt, those by the central government and the private sector and in the case of the domestic debt, only those contracted by the central government. This has been a major exercise because the debt is being reported by the Central Bank and the Treasury in accordance with the global debt reporting standards. These standards require the Central Bank/Treasury to consider all debt owed to a foreign national as foreign debt and all others owed to citizens, irrespective of the currency concerned, as domestic debt. As a result, there is a tendency to underreport foreign debt and overreport domestic debt.

But if you look at it from a debt sustainability point, irrespective of the citizenship, all debt contracted in a foreign currency is regarded as foreign debt and all other debt in the local currency as domestic debt. In addition, according to the IMF definitions, foreign debt consists of all those that have been borrowed in foreign currencies by the central government, by government corporations, by the central bank, by commercial banks, and those by government entities/private firms on guarantees by the government. The calculations by the committee by following this definition are given in the Table.

Accordingly, the nation’s foreign debt had amounted to $ 47 billion and the central government’s domestic currency debt $ 34 billion, making a total debt liability of $ 81 billion or 121% of GDP. However, these numbers also have missed certain other foreign currency debts which the committee too have missed. That is, there is an outstanding balance of $ 1.9 billion owed by the central bank to the Asian Clearing Union which should be paid in every two-month period. This number pertains to the liability as at end of June 2022; but this number may have increased by another $ 500 million in the period since then. When this is due in January 2023, unless the central bank has been able to have it further deferred, it is a mega amount which Sri Lanka should meet. This is deferred trade credit and a foreign exchange liability of the country.

Capitalising the defaulted amounts

There is another concept which has not been investigated. That is, after Sri Lanka decided on 12 April 2022 not to pay the principal and the interest on account of commercial loans and those borrowed from other countries, the defaulted figures should be added to the principal amount every time a debt repayment in this category arises. Thus, the principal reported in the table is going up every month increasing the country’s foreign debt obligations. If the debt restructuring becomes a success with a reasonable haircut being accepted by creditors, the government should get a benefit by way of a reduction in the total debt obligations. If it is not successful, Sri Lanka should add these debt liabilities to the existing debt stock.

|

Need for domestic debt restructuring

There is another aspect which the committee has brought to the notice of fellow parliamentarians. That is the possibility of having to restructure the domestic debt if it becomes impossible for the Government to borrow from the market and repay the maturing domestic debt and the interest involved. The Central Bank is trying its best to avoid this by increasing interest rates on the government papers to more than 30% per annum. Though many complain about the high interest rate structure in the country, given the high inflation of 70%, the real interest rates offered to both savers and borrowers have been in the negative region. As such, the present high interest rate structure should remain in Sri Lanka’s system for a further period.

If for some reason, the domestic debt should also be subject to a haircut of about 40%, the pain to be suffered by domestic institutions, and citizens will be much more. Hence, the present high interest rates are a small payment which Sri Lanka should make to avoid a bigger loss.

RW government cannot ignore this report

Both Sri Lanka’s foreign and domestic debt is a complex issue. If foreigners agree to a haircut, foreigners will lose while Sri Lankans will benefit due to the lowered debt liability. However, if the domestic debt is restructured, all Sri Lankans stand to suffer. This message has been conveyed by the Economic Stabilisation Committee to all Sri Lankans in adequate terms. It is up to President Ranil Wickremesinghe to reckon them when framing the country’s economic strategies.

Hence, in my view, a bouquet is due from all of us to the Economic Stabilisation Committee.

(The writer, a former Deputy Governor of the Central Bank of Sri Lanka, can be reached at [email protected].)