Friday Jul 03, 2026

Friday Jul 03, 2026

Friday, 30 December 2022 00:00 - - {{hitsCtrl.values.hits}}

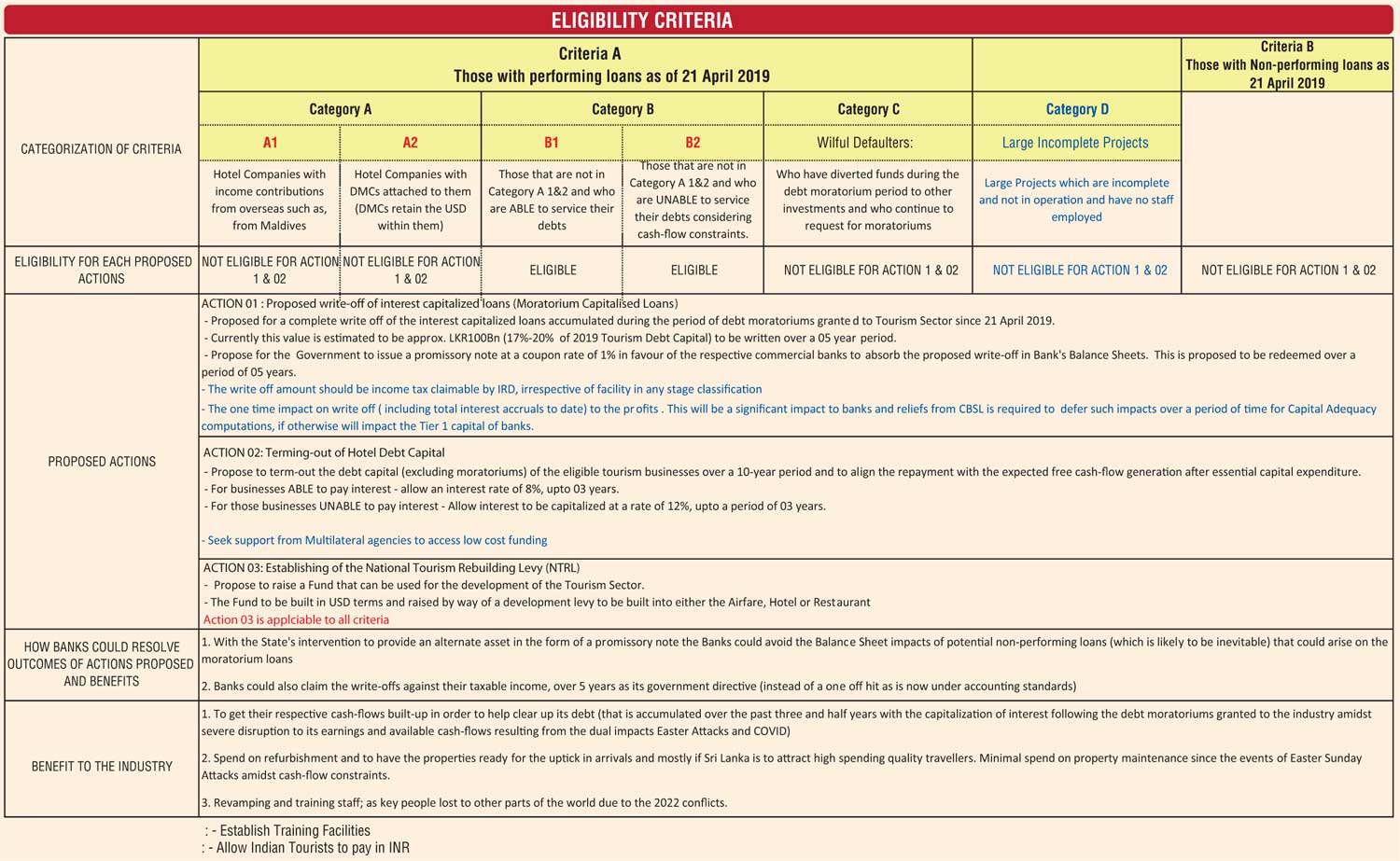

The banks need prudence, knowing the inability of the industry to generate income, and no policy directive on how to treat it

The moratorium interest that has built up over four years due to a manmade economic crisis and muted tourist arrivals has made debt unsustainable for the tourism sector. It is vital therefore to strengthen the tourism industry’s ability to recover and grow; while also ensuring the banking industry that supports them, is stabilised given the exposure to this industry which is around 5.3% of the total lending as at 31 December 2019. The construction industry is another industry that needs serious handholding.

The tourism sector provides approximately one million direct and indirect employment and safeguards the livelihoods of many with its multiplier effect. The tourism industry was the third largest foreign exchange earner for Sri Lanka in 2018 ($ 5 billion direct and indirect) with an approximately 5% of direct contribution to the country’s GDP. The domestic demand which helped to keep the industry alive is expected to contract this year with the increased taxes, high interest rates and rising COL. A recent World Bank report released shows that for every dollar governments invest in protected areas and support for eco-tourism, the economic rate of return is at least six-times the original investment.

The tourism sector is seeking the Government’s support to extend the moratorium concessions further with a clear plan to end it, a reasonable request given the state of affairs in the sector and the probability that the NPL risks to banks will increase substantially, if the moratoriums are lifted (see chart). This extension will help the tourism sector to invest on staff retention and training (large numbers leaving the country). Furthermore, hotels do not possess the funds to attend to the much needed upgrades to their infrastructure that has seriously deteriorated over the last four years, as there was little or no revenue generated due to poor tourist arrivals. The Government needs skills of a high order to find solutions to end this crisis.

Impact on banks

The moratorium interest, and interest accruing on such interest, have been accumulating in the background in bank P&Ls as profits (without actual cash inflows) but reflected in Balance Sheet as a credit build up in retained earnings (at full and normal rates, without a limit), while the debt to hotels are fully borne by the hotel companies. The moratorium interest accumulated have been reflected in the P&Ls of the banks as profits. This inflates the retained earnings of the banks, in their Statements of Financial Position. These retained earnings are not funded by actual cash inflows. This is due to a prolonged period of halted travel with limited tourist arrivals. The banks need prudence, knowing the inability of the industry to generate income, and no policy directive on how to treat it.

These profits have inflated the shareholder funds in the banks’ balance sheets by adding unrealised profits to retained earnings which consist of the unrealised moratorium interest (with no cash inflows) and more worryingly without considering a write down since there were no tourist arrivals. By doing so, the banks have created a void in its Tier 1 Capital by reflecting gains on unrealisable profits from the moratorium loans on tourism.

Options for the Government

Open ended moratoriums certainly impose a direct threat to the stability of the banks. In order to manage this impact and to strengthen the banks’ equity and to reduce the possible risks of NPLs doubling, some options are;

% of the moratorium to be deductible against the tax expenses over a period of 5 years.

Transfer the hard-core moratoriums to an asset management company.

Strengthen banks’ Tier 02 capital which will strengthen the balance sheet.

Ensure the sector is not charged interest at 30% and also penalty interest.

Government to issue an instrument at 0% coupon rate for the value of moratorium accumulation after negotiating with banks.

Conclusion

Given the challenges in several sectors and in forward to medium term demand and until the market numbers (arrivals) and the average spend per tourist gets back to December 2018 levels (the last peak before April 2019), the tourism industry including the SME supply chain should be supported intelligently. The key point to keep in mind is that banks need a healthy private sector to lend going forward. Banks are not in the business of investing in Government treasuries only in a crisis.