Monday Jul 13, 2026

Monday Jul 13, 2026

Tuesday, 20 October 2020 01:18 - - {{hitsCtrl.values.hits}}

A demutualised stock exchange would assist in creating a share owning democracy, complementing the Sri Lankan economy, and be a compliment to the economy of Sri Lanka - Pic by Sameera Wijesinghe

The genesis

With the extinction of the coffee plantation and the introduction of tea to Sri Lanka, the need arose for British planters, who put in all their funds into the coffee plantation, to look at a better risk-free model to fund the newly introduced tea plantation in Sri Lanka. With that came the birth of the Companies Act and the requirement for companies to have access to capital, and as a result, the origins of the Colombo Stock Exchange (CSE) in 1896.

Until the introduction of a regulated market place in 1987, the CSE functioned with a close club of investors with mostly unwritten laws, regulations, and ethics governing them. The birth of the Securities and Exchange Commission (SEC), as a regulator for capital markets, prescribed that the CSE should be a company that is limited by guarantee, where the distribution of profits is not allowed. The CSE is owned by 15 member firms and the Board consist of nine members, out of which five are nominated by its membership. To maintain national interest, four directors are appointed by the Minister of Finance. The chairman will be a nominee from the member firms.

In and around the year 2000 by a directive issued by the Securities and Exchange Commission, the CSE admitted trading members who did not have a right to vote, however, with a right to use the trading platform. They also had an explicit condition imposed on them that they will not benefit or participate in any demutualisation proceeds that would occur in the event the CSE is demutualised.

What is demutualisation?

Over the last two decades, stock exchanges in the world have undergone radical changes and moved towards demutualisation. Demutualisation, in the strictest sense, refers to the change in the legal status of the exchange from a mutual association with one vote per member (and possibly consensus-based decision making), into a company limited by shares, with one vote per share (with majority-based decision making).

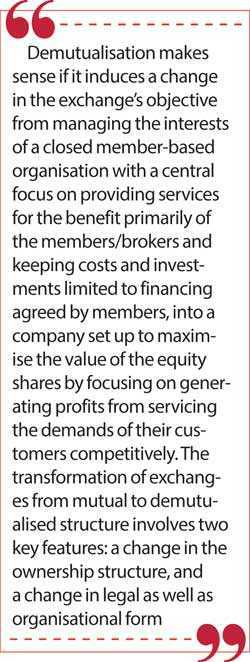

Demutualisation makes sense if it induces a change in the exchange’s objective from managing the interests of a closed member-based organisation with a central focus on providing services for the benefit primarily of the members/brokers and keeping costs and investments limited to financing agreed by members, into a company set up to maximise the value of the equity shares by focusing on generating profits from servicing the demands of their customers competitively.

The transformation of exchanges from mutual to demutualised structure involves two key features: a change in the ownership structure, and a change in legal as well as organisational form.

Both need to be accompanied by adequate safeguards to ensure appropriate governance. Depending on the nature of ownership and legal forms adopted, the demutualised exchange - given their corporate model and facing growing competitive pressures - lends itself to focusing on evolving strategic positioning which, depending on several conditions, could involve greater market consolidation, vertical integration, and product diversification. The objective of demutualisation is to develop and maintain appropriate structures to achieve good governance.

|

|

International take on demutualisation

Demutualised exchanges operate as for-profit entities organised as companies with share capital which may even be listed and publicly traded. Australia, Malaysia, Singapore, and Hong Kong are exchanges that are demutualised, with their shares traded on the exchange.

The process of demutualisation is a complex one, which needs to strike a balance between profit-making and investor protection. Concerns regarding the ability of this approach to do are wide. As it leads to sacrificing effective regulation to meet short-term gains and to maximise shareholder profits. Needless to say, for-profit exchanges and its management tend to prioritise profit and business development to dedicate resources to the regulation of the market and its participants.

A taskforce for demutualisation was set-up under the auspices of the International Organization of Securities Commission (IOSCO), the apex body of capital market regulators. The body held wide consultations and deliberations on some of the matters deliberated above. Its findings focused on minimising and managing challenges and involved recommendations which included the introduction of public interest directors to the Board of the Exchange to better ensure the integrity of the regulation process, some of them listed below;

1. The introduction of ‘public interest directors’ to the Board of the exchange to better ensure the integrity of the regulatory processes.

2. A clear statutory statement of the obligation to provide a fair and efficient public trading market.

3. Publication of the decisions, actions, rules, and regulations of the exchange as well as that of the regulator to enhance transparency.

4. Functional separation of the commercial activities of the exchange from its regulatory functions.

5. Rigorous regulatory oversight and enforcement mechanisms to enhance the exchange’s accountability to the government regulator and the public.

6. A cap on share ownership.

Drawing on international experience and expertise, a demutualised exchange should be structured in a manner to prevent any possible takeovers. A cap on share ownerships, ideally 5%, with some exchanges have higher limits, to forestall any person or entity taking control. Furthermore, even if one or a group of persons obtain majority shares, they would not be able to appoint a majority of the Board and in most cases the majority comprises of executive directors and Government appointees.

After much deliberation, the SEC and the CSE have moved forward in taking this decisive step to demutualise the CSE by presenting a new SEC Act and a Demutualisation Act in Bill form to Parliament for deliberation in 2018. In this respect, the SEC Act needs to be amended to facilitate the licensing of a demutualised exchange and the regulations thereunder. Provisions should be made to convert the CSE from a company limited by a guarantee to a company with share ownership and thus the need for a Demutualisation Act.

The decision to demutualise the CSE was founded on the fact that the old mutual association structure failed to provide flexibility and the resources needed to compete in a competitive environment. The notion of not-for-profit was not a motivating factor for the management and needed entrepreneurs with the discipline to run the organisation in an efficient and keeping-up-with-the-times manner.

The legal angle

The Articles of Association of the CSE, a not-for-profit organisation, stipulates that at a time of liquidation the asset of such organisation should be transferred by the Registrar of Companies to an organisation of similar standing and objectives. This is stipulated in section 83 that at the time of liquidation the assets of the exchange must be given or transferred to some other institution or institutions having objects similar to the objects of the Exchange.

The CSE has considerable assets that cannot be distributed amongst its members. Strictly speaking, the assets then must go to charity as there is no other institution performing the role of the exchange. This highlights the necessity to promulgate legislation for demutualisation.

The most talked-about and contagious issue is the share allocation to the necessary stakeholders. It will be interesting to note that one of the most successful demutualisations was the Bursa Malaysia due to the top-down approach adopted by the then Prime Minister Dr. Mahathir Mohammed who personally drove the initiative until the best possible outcome was achieved.

The methodology adopted in Malaysia was the identifying of stakeholders and apportion of shares to them based on the contribution they have made towards the development of the exchange. It was identified that in addition to the stockbrokers (member firms) they identified listed companies, investors, and the State to have contributed towards such development. After a proper analysis, these stakeholders were presented with appropriate stakes in the demutualised stock exchange. As a result, the brokers – 30%, Remisiers – 10%, Capital Market Development Fund (CMDF) – 30%, Ministry of Finance (State) – 30% and created a CMDF for all other stakeholders that could not be identified individually.

In Sri Lanka, on or about 2004, the then Chairman of the SEC, Dr. Dayanath C. Jayasuriya convened a meeting of the stockbrokers and came to a mutual agreement regarding apportion of shares to the brokers and other stakeholders. However, after that time, with several changes in the economic and political environment, seemingly there has being disputes on the consensus on this matter. The full members of the exchange are staking a high claim and were resistant to any fair position.

The consultants of the Asian Development Bank recently concluded with a parameter for share allocation of the demutualisation. In the event the Malaysian approach is adopted, i.e. of identifying those who contributed to the development of the exchange, the situation may lead to trading members who were licensed after 2005 being eligible for a claim at the demutualisation.

On 26 January 2018 a Demutualisation of the Colombo Stock Exchange Bill was presented to provide for the demutualisation of the CSE by the conversion of the CSE which is a company limited by guarantee, to a company limited by shares; and to provide for matters connected therewith or incidental thereto. Now, with the change of the Government, a fresh Bill will need to be presented with the new SEC Bill for deliberation and approval.

The 2018 Bill stipulated allocation of 60 per centum of the shares to be issued to the full members (stock brokers) and 40 per centum in respectively of the shares to the Capital Market Development Fund set up under the proposed new Act. A maximum ceiling of share ownership of 5 per centum is stipulated to prevent any possible or potential takeover.

I trust that sufficient care has being taken in arriving at this demarcation particularly in respect of the allocation to the state via the Capital Market Development Fund. One must be mindful of donor contributions that were made to the CSE via the State and tax cuts and benefits given to the CSE be factored in computing the allocations.

Where members fail to agree on the allocation of the individual shareholding, each member shall be entitled to an equal proportion of the shares allocated to members (as at one time the members wanted their allocations based on their contributions and turnovers) of the demutualised Stock Exchange, to a maximum ceiling of five per centum for each member.

The proposed Bill specifies that the Minister shall constitute a Nomination Panel consisting of the Governor of the Central Bank of Sri Lanka, Chairman of the University Grant Commission, Director General of the Insurance Regulatory Commission of Sri Lanka, Director General of the SEC and a member of the Board of Directors of the CSE/demutualised Stock Exchange, as the case maybe as determined by the Board of Directors within two months from the appointed date to recommend persons to serve as members of the Board of Directors of the demutualised Stock Exchange:

The Governor of the Central Bank of Sri Lanka shall be the Chairman of the Nomination Panel and the Director-General of the SEC shall be the Secretary of the Nomination Panel.

The selection of the Chairman of the University Grants Commission and the Director-General of the SEC to this Nomination Panel would raise concerns on relevancy and governance issues for a regulator to sit on the selection panel of recommending Directors to an entity regulated by him.

The members of the Board of Directors of the demutualised Stock Exchange appointed shall consist of seven persons comprising—

(a) not more than three persons representing stockbrokers; and

(b) not less than four persons appointed as independent directors.

The Chairman of the Board of Directors of the demutualised Stock Exchange shall be elected by the Board of Directors from amongst the independent directors.

The Capital Market Development Fund set up under the Act is to further public interest through–

(a) the development of the capital market of Sri Lanka;

(b) the promotion of investor education;

(c) the improvement of capital market infrastructure; and

(d) the improvement of investor access and participation in the capital market.

The Board of Directors of the company incorporated for the Capital Market Development Fund set up under the Act shall be–

(a) the Chief Executive Officer of the Demutualised Stock Exchange;

(b) the Director-General of the Commission; and

(c) the nominee of the Chairman of the Commission with the concurrence of the Chairman of the Colombo Stock Exchange.

The appointment of the DG of the SEC seems inappropriate as he becomes a stakeholder in an institution he is regulating.

The Board of Directors of the demutualised Stock Exchange shall take necessary action to list the demutualised Stock Exchange on its own exchange with the approval of the Commission within three years from the date of conversion unless otherwise specified in writing by the Commission. It is hoped that these anomalies will draw the attention of the drafters and rectified accordingly in the new Bill to be presented to this Parliament.

The future

I trust that the demutualisation of the CSE will have a smooth passage without litigation glitches. A demutualised stock exchange would assist in creating a share owning democracy, complementing the Sri Lankan economy, and be a compliment to the economy of Sri Lanka.

A move such as this has the capability of pegging the CSE on a level the same as developed exchanges in the world, having the potential to be a vibrant capital market and make Sri Lanka move towards a regional financial hub. This move will undoubtedly result in augmenting the stature of the CSE on par with other developed exchanges, enabling growth and sustainable development and building the infrastructure necessary for Sri Lanka’s transition into a regional financial hub.

(The writer is a Lawyer, a former Director General of Securities and Exchange Commission of Sri Lanka and a former Senior Advisor to the Minister of Finance. He can be contacted at [email protected])