Saturday Jul 04, 2026

Saturday Jul 04, 2026

Monday, 9 November 2020 01:18 - - {{hitsCtrl.values.hits}}

Since the country has to invest about 30% of GDP and its savings are only about 23%, there is a gap between savings and investments. This gap has to be filled by tapping into the savings of foreigners. Those savings can be attracted by borrowing from them or getting foreigners to invest in income-earning projects in Sri Lanka which is known as Foreign Direct Investments or FDIs

Aseni, the wiz-kid who is interested in learning everything economic, has turned to her Grandpa, Sarath Mahaththaya, an ex-director of the finance ministry, this time to seek wisdom on a new hot topic. That is, she has heard from many that making foreign borrowings is evil because it would trap a country in what is known as ‘a debt trap’. She wanted a clarification from her Grandpa. But her inquiry led to the following dialogue between the two:

Aseni: Grandpa, I’ve heard many saying that foreign borrowings are an evil because they lead to trap a country in an inescapable debt trap. Is it true, Grandpa?

Sarath: That claim is true as well as untrue. True, because Sri Lanka is indeed caught in a debt trap. Its debt level is so mounting that unless it makes further borrowing, it cannot meet the obligations for repaying the debt and paying interest on that debt, a process which economists call ‘debt servicing’. But this is the strategy which Sri Lanka has followed throughout its post-independence history. As a result, the country’s debt levels are increasing year after year.

If we take the Central Government debt, that is, the money borrowed by the Government to finance its budget, it was simply 4.4% of our Gross Domestic Product or GDP at the time of independence in 1948. In 2019. This has increased to 43%. But if we consider the total country debt including the money borrowed by the private sector from abroad, the total foreign debt is about 67% of GDP. Hence, we are in a debt trap, but it does not necessarily mean that borrowing from foreign sources is an evil.

Aseni: Why is it not an evil, if we’re in a debt trap?

Sarath: That is because if we use those borrowings for productive purposes from which we can earn enough income to repay that debt, then, obviously, those borrowings are not an evil. I’ll give you some examples later.

Aseni: What you mean is that without borrowing, we can’t exist, can we, Grandpa?

Sarath: No, borrowing is needed only if your current income or what you have as assets is insufficient to pay for your expenditure plans. In that case, you have a shortage of money and that shortage has to be filled by money borrowed from another party. This is typical for individuals as well as for nations.

Aseni: Can you give an example of why we have to borrow to make payments?

Sarath: I will take the case of an individual first. Consider a newly married couple of which both are employed. Suppose they want to have a car and a house. These are two capital expenditure items, and their current salary is insufficient to have either one of them right now. They cannot wait until they make enough savings to have them. But if they can pay it over a period of time out of the income they would earn, they can borrow today, have both the car and the house and pay later without running into a problem. In this case, borrowing is not an evil.

|

|

Aseni: But Grandpa, these are capital items. If they borrow for current consumption like, say a grandiose wedding anniversary, won’t they get into trouble?

Sarath: Not necessarily if they don’t overborrow and keep those borrowings within their repayment capacity. A rule of thumb for that capacity is that after servicing the debt if they have at least 40% of their income left for day to day expenses, then, it’s within their capacity. This is called their ‘take home pay’ and if it comes down to a very low level and they have to borrow more to repay the debt, then, they are surely in trouble.

Aseni: Understood, but how do you apply this to a country?

Sarath: Same criteria. A country has to borrow from foreigners if its savings are insufficient for meeting the needs of investments. Economic growth depends on how much of your income you would spend on further income earning assets. These are called investments. A rule of thumb for Sri Lanka is that if you want to get 1% growth, you have to invest 5% of your GDP. Thus, if Sri Lanka wants to have an economic growth of 6%, it has to invest at least 30% of its GDP.

Money for these investments should come from savings made by people. Savings are simply that part of your income which you don’t consume. Sri Lanka’s Government is a notorious spender because it spends on consumption more than it earns. Hence, its savings are negative by about, on average, 2% of GDP. This is called a state of dissavings. But Sri Lanka’s private sector is a little better. On average, out of Rs. 100 it earns, it spends about Rs. 75 on consumption. Therefore, Sri Lanka’s private sector makes a saving of 25% of GDP. But since the Government is a dissaver and eats into the savings of the private sector, the total savings of the country are on average about 23% of GDP.

Since the country has to invest about 30% of GDP and its savings are only about 23%, there is a gap between savings and investments. This gap has to be filled by tapping into the savings of foreigners. Those savings can be attracted by borrowing from them or getting foreigners to invest in income-earning projects in Sri Lanka which is known as Foreign Direct Investments or FDIs.

There is another way Sri Lanka can tap the savings of foreigners. That is to get them to invest in Sri Lanka’s share market and in Treasury bills and bonds issued by the Government and debentures issued by private companies. But these moneys are short-term and can go out of the country at any moment. Hence, there is risk in overly depending on them. In that context, the more permanent way of attracting foreign savings is through long-term borrowing or through FDIs. But since the FDI flows are very limited, the only viable way available for Sri Lanka is to borrow.

But those borrowings should necessarily be used for sufficiently high income earning projects. If they are used for low income earning projects or for consumption, it is inevitable that the country would eventually get into a debt problem. This is the crux of the problem we are having in Sri Lanka. Since the Government is consuming more that it earns, a part of its borrowings is used for consumption. At the same time, its investment of proceeds of foreign loans has been in low earning assets. On top of this, since Sri Lanka uses proceeds of loans to service its debt, called debt rolling-over or debt refinancing, naturally it is building its foreign loan stock which does not generate an income at all.

Aseni: What you mean is that we have not used foreign borrowings properly. Has it been the case all the time, Grandpa?

Sarath: No, there have been some occasions where Sri Lanka had used foreign borrowings properly or prudently if we put it in the language of economists. But these instances have been during the colonial times. A good example is how the colonial government financed the construction of the railway system in the country. Contrary to what many believe, not the entirety of the money spent on the railway system was financed out of local resources. It was principally financed out of loans raised from the London capital market. But when approving these borrowings, the Colonial Secretary had laid down two conditions. One was that the country should use the loan proceeds only for the railway project and not for any other purpose. The second was that the railway system should be operated with a surplus and a part of the surplus should be transferred to a special sinking fund dedicated for servicing the debt.

Accordingly, the railway authorities in old Ceylon had borrowed £ 3.1 million at interest rates ranging between 3 and 6% and created a dedicated sinking fund to repay the loans. By 1905 when the whole of the railway system had been fully constructed, the outstanding balance in the sinking fund was Rs. 41 million, while the debt liability was only Rs. 39 million. Thus, the country’s railway system was funded not by general taxpayers but by the users of the system.

Aseni: That is interesting. But what happened to the sinking fund system after that?

Sarath:We continued the sinking fund system even after the independence for some time. But in mid 1980s, the government abolished the sinking fund system because it thought that the moneys transferred to the sinking fund could be used by it for its current expenditure programmes. There was a logic in this argument. That was when the Government was making dissavings and running a budget deficit, the moneys transferred to the sinking fund did not come from its surpluses like the railway project but out of the borrowings it made. There was no logic in managing a sinking fund by borrowing money.

Aseni: But it was a wrong decision, wasn’t it, Grandpa?

Sarath: It becomes a wrong decision on two counts. The first is that the Government instead of managing its revenue and expenditure properly chose to kill the sinking fund system. What it would have done was to generate a sizable surplus at least in its savings and continued with the sinking fund system. Because of this failure, we had continued to rollover the Government debt thereby adding more and more to the debt stock in each passing year. Now we have a debt problem because we do not have resources to service the debt.

It has become a continued borrowing not for investment purposes but for avoiding loan default. Sri Lanka has been downgraded by rating agencies because it runs a risk of further borrowing to service the debt. The more prudent measure is to improve the budgetary situation curtailing consumption expenditure, increasing revenue, and transferring resources for capital investment.

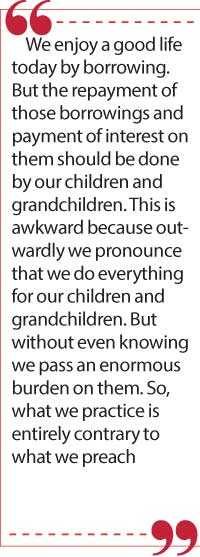

The second count is that we are transferring the burden of debt repayment to our future generations. We enjoy a good life today by borrowing. But the repayment of those borrowings and payment of interest on them should be done by our children and grandchildren. This is awkward because outwardly we pronounce that we do everything for our children and grandchildren. But without even knowing we pass an enormous burden on them. So, what we practice is entirely contrary to what we preach.

But today, we cannot establish a sinking fund system and bear the burden of debt repayment by ourselves. That is because we are not ready to reform our budget to generate a surplus. Therefore, like a festering wound, the situation becomes worse day by day and one day we will succumb to the that unhealable wound.

Aseni: Can’t we borrow from abroad and just wade through the current difficult situation?

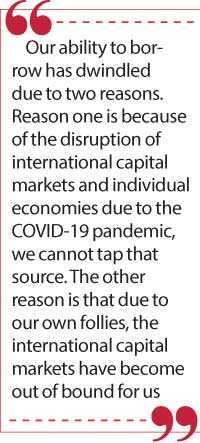

Sarath: There, we have walked to the wall and now we have to scale the wall which is immensely difficult. Our ability to borrow has dwindled due to two reasons. Reason one is because of the disruption of international capital markets and individual economies due to the COVID-19 pandemic, we cannot tap that source. The other reason is that due to our own follies, the international capital markets have become out of bound for us.

We have given a generous tax concession to taxpayers at the beginning of the year and it has eaten into the Government revenue drastically. This has been exacerbated by the onset of the COVID-19 pandemic. The current estimate is that the Government revenue will fall by about 5% of GDP to a level of 8% in 2020. Since the expenses have ballooned, the budget deficit is projected to rise to 10% of GDP. This is known to foreign investors and they have given a high probability to the country defaulting its existing international sovereign bonds or ISBs.

As a result, the yield rates on these bonds have increased significantly in the markets. For instance, the bond which is to mature next year was issued at a coupon rate of 6.25%. But its secondary market yield had risen to 32% last week. This means that an ISB of $ 100 is traded in the secondary market at a deep discount. The bill which I quoted was trading at a price of $ 85.50 in the market denoting a discount of $ 14.50. But the bonds that are to mature in 2029 have gone through the worst experience. The secondary market price of those bonds amounted to $ 60.50 last week, marking a deep discount of $ 39.50. Hence, if we go to the market today, we will have to allow a high discount to prospective investors.

Aseni: That is scary. But the people in the Government say that there is no risk of default of foreign loans because we have enough foreign reserves to do so. Is it the correct situation, Grandpa?

Sarath: Our problem is not only the borrowing of the central Government but also the borrowings of the private sector as well. We should have enough foreign exchange to repay all these loans. According to the latest estimates, within the next 12-month period, our debt servicing obligations will amount to $ 6.7 billion. But the available liquid foreign reserves, after excluding the gold reserve, are only $ 5.4 billion. Naturally, unless we borrow, we have no resources to repay these loans because our balance of payments is going to be in a massive deficit this year.

Aseni: Can’t we go for a rescheduling of our loans and get some breathing space?

Sarath: That is one possibility, but it would give us only temporary possibility. The medium to long term solution should be to improve the budget and earn capacity to service the debt and have extra space to handle the type of disasters which we are facing today. That requires all of us to make the utmost sacrifice from top to the bottom. Without that, I do not see any chance for Sri Lanka. I am waiting for the budget to be presented in Parliament shortly to see whether the Government would address these issues.

Aseni: That is a good discussion and thank you, Grandpa. I now know that foreign borrowings are needed because of the low domestic savings. But if they are not used properly, the country would get into serious problems relating to debt servicing.

(The writer, a former Deputy Governor of the Central Bank of Sri Lanka, can be reached at [email protected].)