Thursday Jun 11, 2026

Thursday Jun 11, 2026

Wednesday, 13 February 2019 00:00 - - {{hitsCtrl.values.hits}}

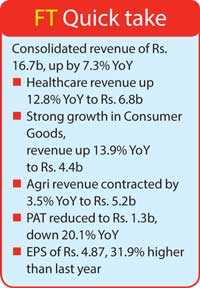

Diversified Sri Lankan conglomerate Sunshine Holdings (CSE: SUN) reported top-line performance growth of 7.3% YoY to stand at Rs. 16.7 billion for the first nine months of the current financial year (9MFY19).

The top-line increase was mainly due to strong performances in the consumer and healthcare sectors and despite a contraction within the agribusiness sector. The company also reported a 31.9% growth in earnings per share (EPS).

Profit after Tax (PAT) for the period in review declined to Rs. 1.3 billion and profit margins have also reduced to 7.8% compared to last year’s (9MFY18) 10.5%, mainly due to lower profitability in the agribusiness sector. The group’s healthcare business emerged as the largest contributor to Sunshine’s top-line performance, accounting for 40% of total revenue, while agribusiness and consumer goods sectors of the group contributed 31% and 26% respectively of the total revenue.

Profit after Tax and Minority Interest (PATMI) increased by 36.9% YoY to Rs. 700 million with the agribusiness sector, represented by Watawala Plantation PLC (CSE: WATA) and Hatton Plantations PLC (CSE: HPL), making the largest contribution to PATMI, accounting for 46% of the total. Net Asset Value per share increased to Rs. 53.54 as at end 9MFY19, compared to Rs. 48.81 at end of 9MFY18.

“Our strong top-line performance reflects the dedication of our employees to delivering the best products and unmatched service and convenience to our customers, amidst tough business conditions,” said Sunshine Holdings PLC Group Managing Director Vish Govindasamy. “Both Consumer Goods and Healthcare sectors have been able to continue their momentum from last year, reporting impressive revenue growth during this period.

“Moving forward, we will continue to consolidate our operations with a view to further strengthening overall profitability while also exploring opportunities to expand growth within our current business segments. Our continuous focus on improving quality and internal efficiency through well-placed strategies will yield strong results for the group in the coming few months,” stated Govindasamy further.

As the largest contributor to Group revenue, Sunshine Healthcare grew its revenue by 12.8% YoY to Rs. 6.8 billion. Though the second round of drug price control – which came in to effect in September 2018 – had a negative impact, the revenue growth was propelled due to higher sales volume and footfall growth in retail. The pharma sub-segment, which represents 65% of healthcare revenue, was also up by 8.5% YoY. Reported PAT for healthcare amounted to Rs. 218 million in 9MFY18, up 8.5% YoY.

Sunshine’s Consumer brands – spearheaded by premium brands like ‘Zesta’ and ‘Watawala Tea’ – recorded impressive growth in revenue, with stronger domestic business growth enabling a 13.9% YoY growth to Rs. 4.4 billion on the back of both volume and price increases. Due to lower input costs, PAT from the Consumer segment grew by 90.4% YoY, to stand at Rs. 391m for 9MFY19, resulting in higher gross profit margin.

The Group’s agribusiness sector, led by Watawala Plantations PLC (WATA) and Hatton Plantations PLC (HPL), saw a revenue decline of 3.5% YoY to Rs. 5.1 billion due to unfavourable weather conditions which impacted the tea plantations managed by HPL. Tea volumes were contracted by 4% YoY, resulting in a revenue drop of 19.5% YoY. However, palm oil sub-sector reported an increase in revenue of 12.1% YoY due to the increase in net sale average (NSA) and a marginal increase in crop. Due to lower yields, PAT for Agri sector 9MFY19 amounted to Rs. 734 million, contracting 29.4% YoY. Sunshine’s Renewable Energy recorded revenues of Rs. 311 million in 9MFY19, up 52.6% YoY from Rs. 204 million during the same period last year as a result of higher rainfall in the catchment areas. The sector made a profit of Rs. 165 million for 9MFY19, compared to a profit of Rs. 57 million in 9MFY18.

Govindasamy noted that the Group will focus on stabilising the volumes as far as their healthcare business is concerned, despite the depreciation of the rupee against the dollar continues to impact the margins of the entire healthcare industry. He also said that greater attention will be given to further strengthen Healthguard’s online presence among Sri Lankans in order to attract more customers towards their specialty range of beauty and wellness products.

Similarly, the Group’s consumer business would continue investments into its brands to scale the domestic business while the continuing success of its Palm Oil segment was also expected to continue to yield higher returns, brought about by superior agronomic practices.

The wage collective agreement was entered between the Regional Plantation companies (RPC’s) and the trade unions on 28 January increasing the daily basic wage to Rs. 700, the Price Share Supplement (PSS) to Rs. 50 and thereby the total daily wage to Rs. 855.

The dairy sub-sector has reached a total of 1,016 milking cows. The total number of animals has also grown to 1,257. However, Govindasamy noted that the interim cost of feeding the whole herd would have a slightly negative impact on Agri profitability. In the Renewable Energy segment, construction of their third hydropower plant was concluded in the fourth quarter and the first roof-top solar unit had been commissioned at Sunshine Tea Kelaniya premises.