Sunday Mar 29, 2026

Sunday Mar 29, 2026

Monday, 20 November 2017 00:00 - - {{hitsCtrl.values.hits}}

By Dr. P. Nandalal Weerasinghe, Senior Deputy Governor, Central Bank of Sri Lanka

I am deeply honoured to have been invited to deliver the Olcott Oration 2017 and to join a list of great Anandians who have delivered this Oration before. I cannot think of a greater honour that my school could confer on me.

I accepted this invitation with humbleness, with gratitude and respect, and with great pride. Let me also take this opportunity to appreciate the support and guidance I received during my school career at Ananda College. The guidance our teachers gave us laid the foundation for any success later on in our lives.

My oration today is on the rather technical topic of monetary and exchange rate policy. The biggest challenge that I have to face is to present such a topic to an audience with a majority who might not be familiar with the technical jargon involved. However, I will attempt to keep the discussion as simple as possible.

Central banking and price stability

The prime responsibility of any central bank around the world is to maintain price stability by way of maintaining low and stable inflation on a sustainable basis. At the outset, I would like to discuss why low and stable inflation is important for growth and stability of the economy.

Based on experiences of many countries and different time periods, we have seen varying levels of inflation. When countries experience hyperinflation, domestic prices of goods and services will rise every minute. In such a situation, no one will want to hold the local currency and people will rush straight from the bank to the shops to buy goods, fearing that their currency holding will lose value along the way.

In fact, the banking system itself will collapse. As people lose faith in local currency, the barter system, or the exchange of goods for goods or services will become the norm, making transactions significantly more difficult. Hyperinflation will also cause adverse redistributive effects, destroying real value of middle class savings in local currency and real incomes of fixed income earners such as workers and pensioners.

One can read horror stories of hyperinflation in Germany and Australia in the 1920s, and more recently in several Latin American countries and also in countries like Zimbabwe. The episode of hyperinflation in the inter-war Germany is said to have facilitated the rise of Hitler and the global destruction that followed.

The famous economics author Neil Irwin, in his book titled ‘The Alchemists: Three Central Bankers and a World on Fire’, called the Governor of the German Reichsbank at the time, the “worst central banker in history!”

Let us also look at the other extreme case of price movements, namely deflation. The example that will come to anyone’s mind is Japan, which underwent what was known as the “lost decade”. Now it is termed the “lost 20 years!” Since the early 1990s Japan experienced deflation, a continued decline in prices of goods and services. One may think that this is great but what could be considered good for a consumer in the short term may not be good for the entire economy, as evidenced by the experience of Japan. Since then, the Japanese economy had experienced negative economic growth, a drop in nominal GDP, declining wages and negative interest rates. Some indications of sustained growth in Japan are seen only now.

Fortunately, Sri Lanka has never experienced such episodes in the past, and clearly we want neither hyperinflation nor deflation even in the future. But what about double-digit inflation hovering around 10-20%, as experienced in Sri Lanka for several decades from 1970s? Empirical evidence clearly shows that this kind of double-digit inflation is bad for sustained growth. High and volatile inflation causes lenders like banks and other financial institutions to demand a higher fixed interest rate on loans to compensate for the risk that inflation will move around, thus raising the cost of finance for investment. At the same time, financial institutions need to offer higher nominal and real interest rates to encourage savers to deposit their money to mitigate the risk of high and volatile inflation eroding the real value of their savings. High and volatile inflation increases the margin between lending rates and deposits, and this high cost of financial intermediation penalises both savers and borrowers. High and volatile inflation encourages workers to bargain for higher wages. High and volatile inflation also prompts producers and sellers in the economy to add higher markups in pricing of goods and services. The combined result of this self-fulfilling cycle will be lower economic growth and higher current account deficits, depleting reserves and volatile exchange rates, and the country will end up with a commercial capitalist class of buyers and sellers of imported goods or a class of middlemen!

Then the question is what is the appropriate level of low and stable inflation which will result in more desirable outcomes? Most advanced economies set their inflation target in the low single digits around 2%. For example, the United States and the United Kingdom desire to maintain inflation at around 2%, while in the Eurozone it is below but close to 2%. Australia has an inflation target of 2-3%, and in New Zealand it is 1-3%.

Within emerging market and developing economies, the targets are slightly higher. The Philippines and Chile target 2-4%, Indonesia 2.5-4.5%, Brazil 4.5%, South Africa 3-6%, while India targets 2-6% of inflation.

It must be noted here that a Central Bank could only effectively control demand driven inflation. Central banks could do little to address short-term disruptions to prices due to adverse domestic supply developments or unexpected international commodity price movements. However, central bank responses will be required to contain demand driven inflation, usually identified by movements in core inflation indices.

Monetary policy frameworks

In order to maintain low and stable, single-digit inflation, central banks around the world are entrusted with the task of conducting monetary policy with varying degrees of independence. Central banks use various monetary policy frameworks, as there needs to be a mechanism to operationalise the achievement of the end objective of price stability using the policy tools given to central banks to fulfil this task.

Monetary policy frameworks differ across countries depending on country-specific circumstances such as the level of financial market sophistication, openness of the economy, strengths, capacities and independence of institutions, etc.

For example, monetary policy frameworks in some countries are based on currency board arrangements where the value of domestic currency is strictly pegged to an international currency. In currency board arrangements, domestic inflation is directly linked to inflation of the country of which its currency is pegged, and then the anchor for inflation will be the exchange rate.

In such strict exchange rate targeting regimes, the country’s business cycles in terms of growth and inflation would be fully synchronised with the other country’s business cycles. In these countries, monetary authorities have very little leeway to use monetary policy as a countercyclical policy measure to stabilise growth and inflation in the domestic economy.

In the other extreme end, monetary policy frameworks are based on fully-fledged inflation targeting regimes where inflation is directly anchored through inflation targets and interest rate policy, while maintaining fully floating exchange rates. Under this arrangement, the exchange rate acts as the shock absorber to minimise the impact of external shocks on the real economy. In such regimes, central banks have more autonomy to use interest rates as an instrument to counter any cyclical economic shocks. There are many central banks that have a combination of these two extremes, where some are closer to inflation targeting and others being closer to exchange rate targeting with soft pegs with some leeway to use the interest rate as an instrument to manage inflation and growth. One cannot argue that one regime is superior to the other. It all depends on country circumstances, and even within one country, monetary policy frameworks move in different directions at different times. Monetary aggregate targeting frameworks fall between these two extreme regimes depending on the extent of exchange rate flexibility of such policy regimes.

Evolution of monetary policy framework in Sri Lanka

Sri Lanka’s monetary policy framework has also evolved from a currency board arrangement before the establishment of the Central Bank of Sri Lanka in 1950. This history has been well covered in the masterpiece, ‘From dependent currency to central banking in Ceylon’ written by Prof. H.A. de S Gunasekera, in whose honour my retired senior central bank colleague Sirimevan Colombage delivered an eloquent speech recently at the University of Peradeniya.

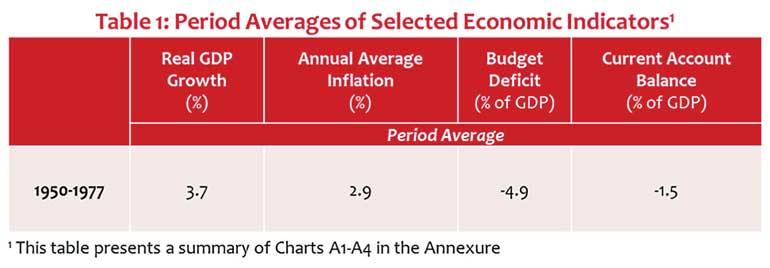

From 1950-1977 Sri Lanka’s monetary policy framework was largely based on maintaining a fixed exchange rate regime in terms of fixing the value of the Sri Lankan rupee first to the sterling pound and then to the US dollar. Under this fixed exchange rate regime, domestic inflation was directly linked to foreign inflation and therefore there was no need for an explicit monetary anchor to manage inflation. The Central Bank did not have much leeway to control domestic inflation as the fixed exchange rate was the anchor to manage inflation. Like many other things, inflation was also more or less imported from the United Kingdom those days!

This system worked well as long as Sri Lanka earned sufficient foreign exchange to meet expenditure on imports without any restriction. For example, during the periods of export booms particularly in the early 1950s, the fixed exchange rate regime worked well, as foreign exchange earnings, which arose due to external factors rather than domestic export promoting policies, were not only sufficient to meet current expenditure but also helped build up foreign reserves so that a currency peg could be maintained without foreign grants or borrowings. The necessary condition for any country to maintain a currency peg with a strong reserve currency like a sterling pound on a sustainable basis is the country’s ability to earn sufficient foreign exchange. In other words, such a country would require a strong set of export-oriented policies.

In technical terminology, a country should run at least a balanced current account in the balance of payments on a long-term basis for it to be able to maintain a peg with a strong foreign currency. Economies like Japan early on, and later Hong Kong, Singapore, Taiwan and even China, given their strong export-oriented policies, were able not only to generate current account surpluses on a sustainable basis, but as a result, also saw the value of their currencies appreciating against major currencies like the sterling pound and the US dollar.

During the period of Sri Lanka’s fixed exchange rate regime, successive governments did not pursue export oriented policies continuously. There were short episodes where policies focused on export promotion, but there were more times of policy reversals towards encouraging import substitution and inward looking polices. From a long-term perspective, such polices were inconsistent with the need to maintain a fixed exchange rate regime. Under these circumstances, the key challenge the Central Bank had to face was how to defend the exchange rate peg amidst policies which did not promote exports. The only choice available for the Central Bank at the time was to restrict the use of available foreign reserves and impose severe exchange control restrictions. In a way, the Central Bank at the time was successful in maintaining low inflation, which is one of the key responsibilities of the bank, but it failed to support the multiple objectives, which were often in conflict with each other, of the then Central Bank.

In addition to pursuing inward looking economic policies, successive governments also ran high budget deficits mainly to provide subsidies and various free entitlements. Such budget deficits, even at moderate levels, caused more demand for imports in the midst of weak export performance, creating continued current account deficits, while the Central Bank was required to maintain a fixed exchange rate regime. This was an impossible task for the Central Bank. As a result, the Central Bank, from time to time, either devalued the rupee or maintained a dual exchange rate along with severe restrictions on the use of foreign exchange. This monetary policy framework lacked credibility and created severe distortions to market pricing.

Meanwhile, on the global front, the collapse of the Bretton Woods system, with the United States declaring in 1971 that it would cease to redeem US dollars for gold from its reserves, challenged the system of fixed exchange rates that the global economy was used to operate in. In addition, the 1973 oil crisis caused inflation to escalate in all countries, including Sri Lanka, often resulting in a destructive wage-price spiral. In Sri Lanka, inflation increased to 14.4 per cent by December 1973, the highest level of inflation the country experienced until then during its post-independent history.

Elsewhere in the world, following the collapse of the Bretton Woods system of exchange rates, the international community was getting used to floating exchange rates, where each currency’s value was determined by the international demand for the currency. This was a new normal, prior to which money has historically been based on a valuable commodity such as gold.

Post-liberalisation monetary policy framework

In November 1977, Sri Lanka embarked on a major economic liberalisation move, marking a paradigm shift from inward-looking restrictive policies towards a liberal regime under which trade and payments were liberalised to a great extent.

To be consistent with the new liberal regime, the Central Bank abandoned the fixed exchange rate regime and moved to a more market based system of exchange rate management. On 15 November 1977, the prevailing dual exchange rates were unified at an initial rate of Rs. 16 against the US dollar. This was an overnight devaluation of the basic exchange rate by 120%.

The rupee was then allowed to float under a managed exchange rate regime. Accordingly, compared to the end 1976 exchange rate of Rs. 8.83 per US dollar, the exchange rate was recorded at Rs. 15.56 at end 1977.

This sharp devaluation addressed the overvaluation of the rupee observed under the fixed regime. The subsequent managed exchange rate regime allowed some flexibility to determine the value of currency largely on the basis of market demand and supply, while attempting to prevent the overvaluation of the rupee by maintaining the real value of the rupee against movements of a basket of major currencies.

The aftermath of the managed float

The introduction of the managed floating exchange rate was a welcome move from the perspective of a liberal macroeconomist. However, this resulted in new challenges to the conduct of monetary policy, particularly as the exchange rate was no longer available to anchor inflation expectations like in the past. The Central Bank also had to face a new challenge, as the Government started to run extremely large fiscal deficits funded mainly by concessional external funding to develop public infrastructure such as the accelerated Mahaweli scheme. Annual fiscal deficits averaged 13.3% of GDP between 1978 and 1983, external current account deficits averaged 10.8% of GDP between 1979 and 1983. Year-on-year inflation averaged 15.6% during February 1978 and January 1985, with a peak of 32.5% in August 1980. It must be mentioned here that rising inflation was a main cause for the 1980 general strike, which resulted in over 40,000 public and private sector workers losing their jobs.

Little wonder that the Central Bank of Sri Lanka started looking for a new framework to contain inflation and inflation expectations in the absence of the pegged exchange rate system.

Beginning of monetary aggregate targeting in Sri Lanka

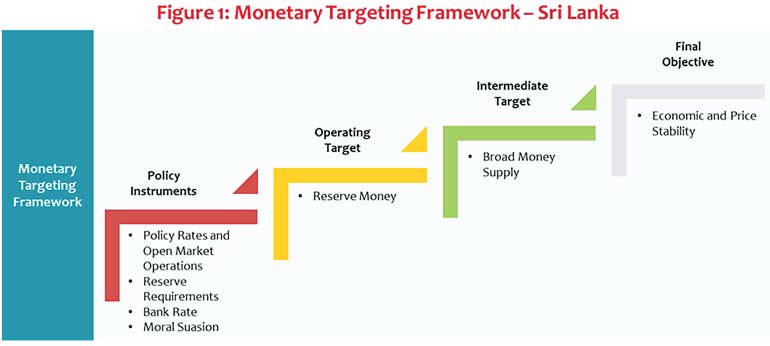

The relationship between monetary expansion in terms of the amount of money held by the public and inflation has been well recognised in Sri Lanka from the beginning of central banking in the country. However, the first mentioning of “desired monetary targets” in a Central Bank annual report in Sri Lanka could be found in 1982.

The 1982 annual report states that “the National Credit Plan for 1982 was formulated against the perspective of the prevailing monetary and credit policies. It attempted to rationalise the use of private sector credit among different sectors of the economy as an instrument of selective credit policy. Having taken into consideration the real growth, estimated rate of price increase and increased monetisation of the economy, the desired monetary targets were set in the Plan with a view to maintaining the consistency between financial and real output flows in the economy. The monetary targets were then translated into a permissible level of credit to the private sector by commercial banks after allowing for the impact of the behaviour of the external sector and the credit requirements of the government.”

This is a classic characterisation of an annual monetary programme, which is a crucial element in monetary aggregate targeting. Based on Irving Fisher’s Quantity Theory of Money, monetary aggregate targeting seeks to explain the relationship between money growth and nominal economic growth (which is the combination of real economic growth and inflation). In this framework, as monetary policy instruments attempt to influence the final objective of inflation by first affecting monetary aggregates, broad money supply was considered the intermediate target. For operational purposes, reserve money or base money, which could be influenced and monitored by the Central Bank on a daily basis, was considered the operating target. The operating target and the intermediate target, both being monetary aggregates, were linked to each other through the money multiplier.

To be continued tomorrow

Footnote: I would like to note that the views expressed in this oration are my own as an economist and do not necessarily reflect the views of the Central Bank of Sri Lanka. I also would like to acknowledge the technical support received in preparing the oration from Dr Chandranath Amarasekara and his team at the Economic Research Department of the Central Bank of Sri Lanka.

Click here to read Part II

Click here to read Part III