Acuity Stockbrokers Research has come out with an assessment on the potential impact from Brexit on the Sri Lankan economy.

Here are some highlights of the report

Summary: Brexit roils global markets

-

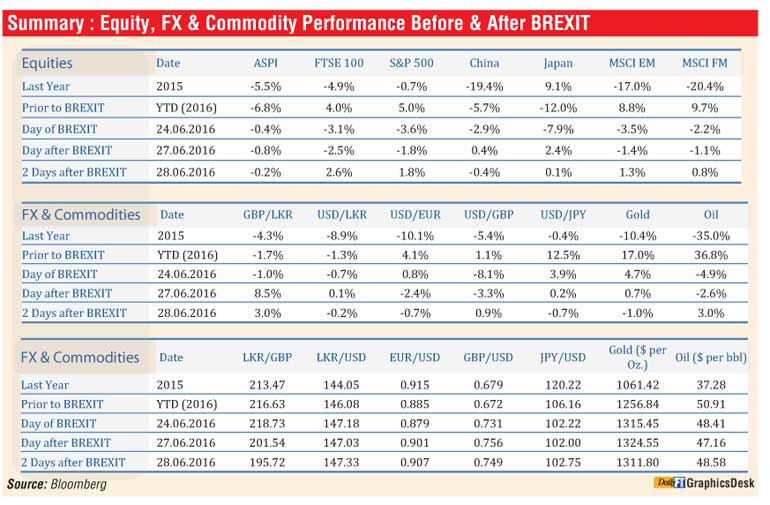

Britain’s decision to exit the European Union sent shock-waves across global markets, as markets had perceived Brexit to be a tail-risk at most. In the immediate aftermath of the decision, the GBP collapsed 8% (against the USD) to its lowest in 30 years, the FTSE 100 crashed 8% intra-day (before closing 3.1% lower), while markets across Asia collapsed as investors fled towards traditional safe-havens such as the USD and gold.

-

Concerns over global growth and increased uncertainty pitched investors into ‘risk-off’ mode immediately, but further developments in the wake of Brexit has created additional insecurity. Following the vote,

-

British Prime Minister David Cameron announced his resignation while Scotland has indicated its dissatisfaction with the vote, highlighting the political fallout from the referendum

-

Moody’s downgraded UK’s credit ratings outlook to ‘negative’ due to a ‘prolonged period of uncertainty’ following the vote. S&P downgraded UK by two notches (from “AAA” to “AA”), while Fitch lowered its rating from “AA+” to “AA.”

-

EU leaders have pressed for the UK’s swift exit to mitigate further uncertainty

Summary: Sri Lanka impacted via financial and trade channels

-

The impact to Sri Lanka via the trade channel could also be significant, as the EU and UK remain major trading partners. The EU is Sri Lanka’s largest trading partner (~29% of exports in 2015) and the UK accounts for 35-40% of this proportion. Sri Lanka’s primary exports to the region (garments, footwear, tourism and tea) are likely to face some pressure in the short to mid-term while competitive pressures are likely to heighten due to depreciation across most EM/FM currencies.

-

Delays in renegotiating trade agreements with EU/UK: Prior to Brexit, Sri Lanka’s Prime Minister indicated his optimism that GSP+ with the EU could be regained by year-end. With the recent developments in EU/UK however, there may be delays in negotiations; moreover, new trade deals will have to be negotiated with the UK which will now fall outside the purview of GSP+.

-

Heightened competitive pressure: The global ‘Risk-off’ environment implies that EM/FM currencies are likely depreciate across the board, suggesting that the competitive pressures for Sri Lanka’s exports are likely to increase in short-medium term.

Potential impact from Brexit | Emerging market risks increase

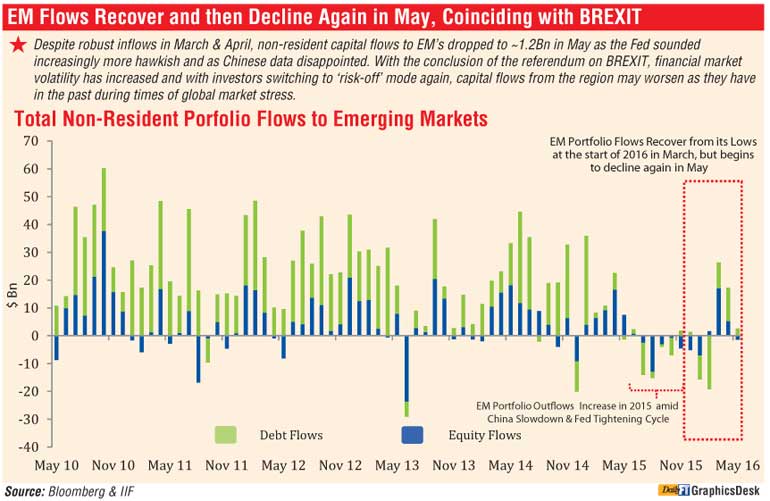

EM flows recover and then decline again in May, coinciding with Brexit

-

Despite robust inflows in March and April, non-resident capital flows to EM’s dropped to ~1.2 b in May as the Fed sounded increasingly more hawkish and as Chinese data disappointed. With the conclusion of the referendum on Brexit, financial market volatility has increased and with investors switching to ‘risk-off’ mode again, capital flows from the region may worsen as they have in the past during times of global market stress.

Asian markets tank, extending YTD losses on equity markets across most of the region

-

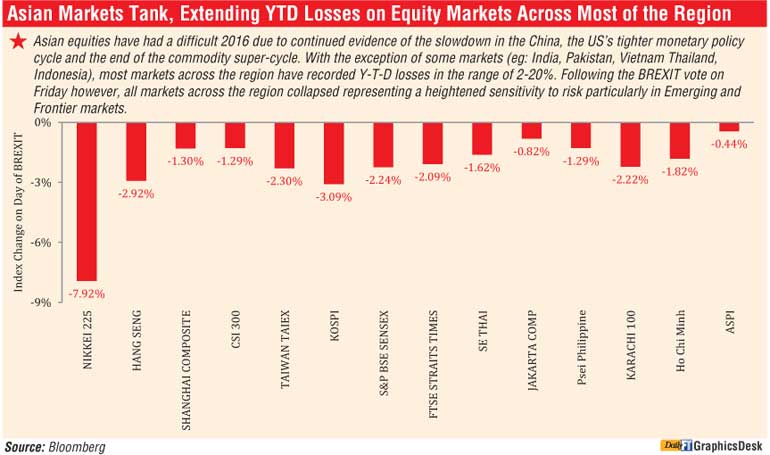

Asian equities have had a difficult 2016 due to continued evidence of the slowdown in the China, the US’s tighter monetary policy cycle and the end of the commodity super-cycle. With the exception of some markets (eg: India, Pakistan, Vietnam Thailand, Indonesia), most markets across the region have recorded Y-T-D losses in the range of 2-20%. Following the Brexit vote on Friday however, all markets across the region collapsed representing a heightened sensitivity to risk particularly in Emerging and Frontier markets.

Traditional safe-haven assets by contrast gain

-

Assets such as gold and the US dollar by contrast, gained following the vote, as Investor risk appetite waned. Gold prices hit a two-year high of 1315 per Oz, while the USD which has been gaining steadily against most currencies since 2015 gathered pace.

EM/FMs tend to underperform significantly during periods of global market stress

-

Since EM/FM markets tend to react strongly to periods of financial market volatility, the risk of EM/FM underperformance has risen significantly.

Potential impact from Brexit | Upside pressure on rates increases

Higher government security outflows to pressure rates

-

Net portfolio flows (debt and equity) to EM/FMs turned negative for the first time since 2008 last year on the back of Fed tightening and China growth concerns. With investor appetite for riskier debt likely to wane on the back of Brexit, a similar trend may re-appear this year and rates are likely to increase as investors off-load EM/FM debt.

Domestic pressure on rates exacerbated by potential implications of Brexit

-

Domestic pressures such as higher private credit (+28.1% Y-o-Y in April’16) and higher inflation (May CCPI up 4.8% Y-o-Y [cf. 3.1% in Apr] and May NCPI up 5.3% Y-o-Y [cf. 4.3% in Apr]) already placed upside pressure on rates in Q2’16. With the outcome of the Brexit vote however, the potential for higher rates has increased further since global financial market volatility is likely to result in higher short-term net portfolio outflows from frontier markets such as Sri Lanka.

Potential impact from Brexit | Depreciation pressure on LKR rises

Headwinds to LKR exist even excluding the impact from Brexit

-

Continued debt and equity portfolio outflows coupled with external debt repayments have placed pressure on the LKR through 2016. G-Sec holdings by foreigners had declined to $ 1.6 b by May’16 while the equity sell-off by end-May was ~$40 m. The country’s pre-determined external debt payments for the remainder of the year meanwhile, is estimated at ~$1.3 b, underscoring the existing headwinds to the LKR’s value.

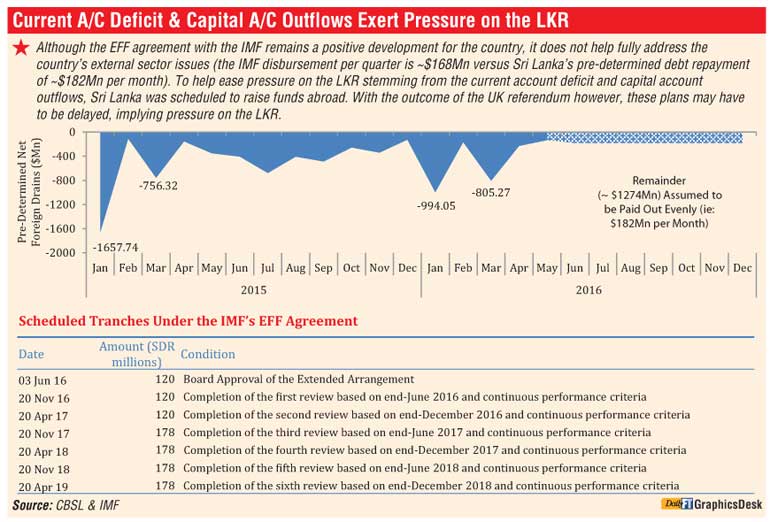

Current A/C deficit and capital A/C outflows exert pressure on the LKR

-

Although the EFF agreement with the IMF remains a positive development for the country, it does not help fully address the country’s external sector issues (the IMF disbursement per quarter is ~$168 m versus Sri Lanka’s pre-determined debt repayment of ~$182 m per month). To help ease pressure on the LKR stemming from the current account deficit and capital account outflows, Sri Lanka was scheduled to raise funds abroad. With the outcome of the UK referendum however, these plans may have to be delayed, implying pressure on the LKR.

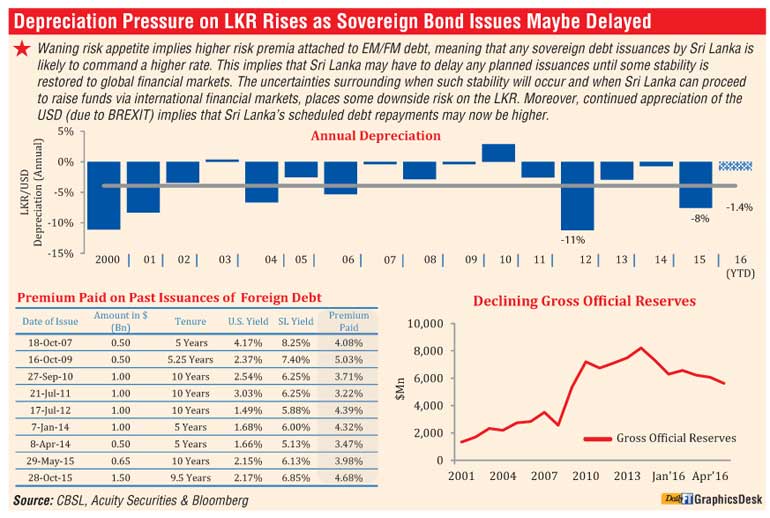

Depreciation pressure on LKR rises as sovereign bond issues may be delayed

-

Waning risk appetite implies higher risk premia attached to EM/FM debt, meaning that any sovereign debt issuances by Sri Lanka is likely to command a higher rate. This implies that Sri Lanka may have to delay any planned issuances until some stability is restored to global financial markets. The uncertainties surrounding when such stability will occur and when Sri Lanka can proceed to raise funds via international financial markets, places some downside risk on the LKR. Moreover, continued appreciation of the USD (due to Brexit) implies that Sri Lanka’s scheduled debt repayments may now be higher.

Potential impact from Brexit | Impact via trade channel

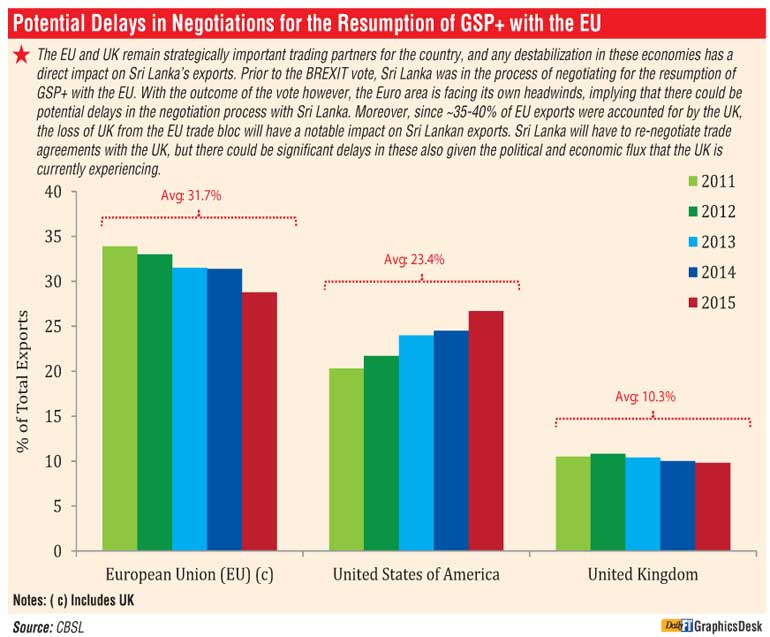

Potential delays in negotiations for the resumption of GSP+ with the EU

-

The EU and UK remain strategically important trading partners for the country, and any destabilisation in these economies has a direct impact on Sri Lanka’s exports. Prior to the Brexit vote, Sri Lanka was in the process of negotiating for the resumption of GSP+ with the EU. With the outcome of the vote however, the Euro area is facing its own headwinds, implying that there could be potential delays in the negotiation process with Sri Lanka.

-

Moreover, since ~35-40% of EU exports were accounted for by the UK, the loss of UK from the EU trade bloc will have a notable impact on Sri Lankan exports. Sri Lanka will have to re-negotiate trade agreements with the UK, but there could be significant delays in these also given the political and economic flux that the UK is currently experiencing.

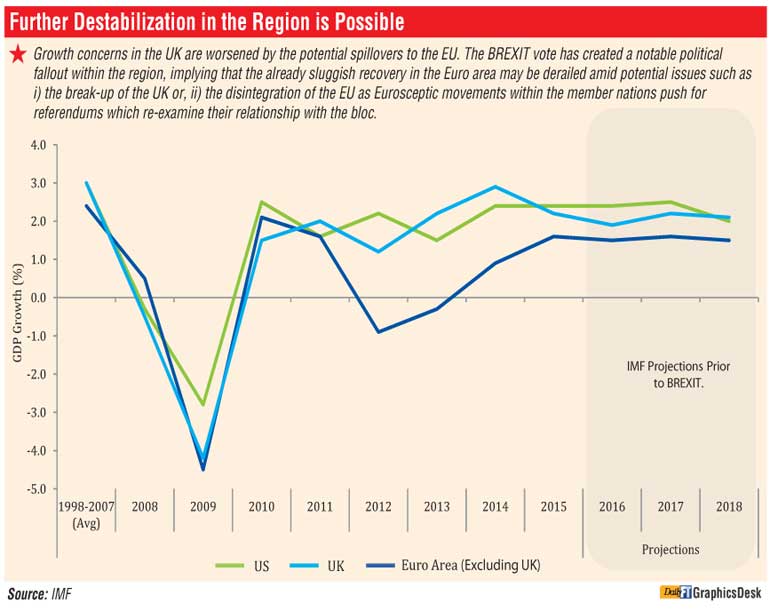

Further destabilisation in the region is possible

-

Growth concerns in the UK are worsened by the potential spillovers to the EU. The Brexit vote has created a notable political fallout within the region, implying that the already sluggish recovery in the Euro area may be derailed amid potential issues such as i) the break-up of the UK or, ii) the disintegration of the EU as Eurosceptic movements within the member nations push for referendums which re-examine their relationship with the bloc.

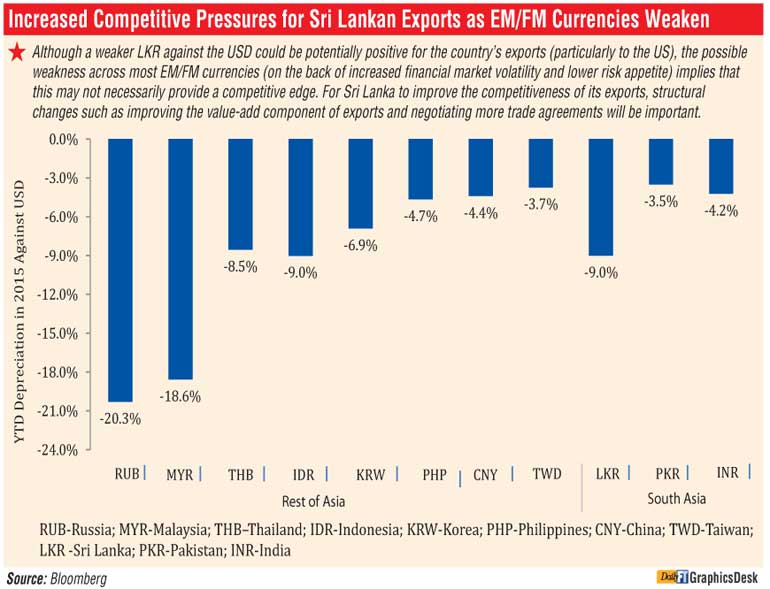

Increased competitive pressures for Sri Lankan exports as EM/FM currencies weaken

-

Although a weaker LKR against the USD could be potentially positive for the country’s exports (particularly to the US), the possible weakness across most EM/FM currencies (on the back of increased financial market volatility and lower risk appetite) implies that this may not necessarily provide a competitive edge. For Sri Lanka to improve the competitiveness of its exports, structural changes such as improving the value-add component of exports and negotiating more trade agreements will be important.

Potential impact from Brexit | Actions by Sri Lankan authorities

Initial actions undertaken by the Sri Lankan authorities

-

While the impact/outcome from Brexit is still too recent to gauge the Sri Lankan Authorities counteractive policy measures, local media has highlighted the following as initial measures/policy proposals:

-

The Finance Ministry is expected to enter an agreement with the World Bank for an IDA loan of 71.3 m SDR (equivalent to $ 100 m). The loan (which is a Special Drawing Rights (SDR) loan from the International Development Association) will be on a fixed rate and have a 27-year tenor.

-

Based on comments by the Minister of Industry and Commerce, Sri Lanka has enlisted the WTO to negotiate new trade pacts with the UK.

-

The Prime Minister outlined long term plans to foster stronger ties with Asia in the aftermath of Brexit. Plans to counter the impact from BREXIT include fast-tracking negotiations with India on the Economic Technology Cooperation Agreement (ETCA) and implementing four Free Trade Agreements (FTAs) with key regional economies.

-

The CBSL submitted an Action Plan to the President and Prime Minister on Saturday, detailing strategies and steps Sri Lankan authorities should undertake to counteract the changes stemming from Brexit.

The document is expected to be submitted to the cabinet sub-committee on economic affairs later this week.