Sunday Feb 22, 2026

Sunday Feb 22, 2026

Monday, 19 August 2019 00:33 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

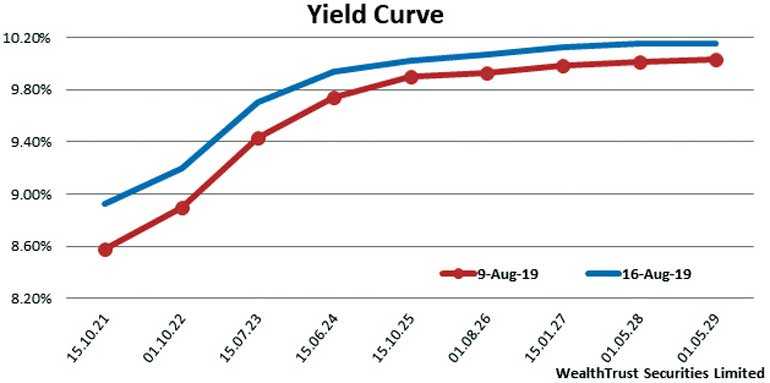

The secondary bond market witnessed renewed selling interest by both foreign and local participants during the shortened trading week ending 16 August, which led to yields increasing across the yield curve. The increase in the benchmark 364-day bill weighted average for the first time in 25 weeks at its weekly auction contributed to the upward movement in yields as well.

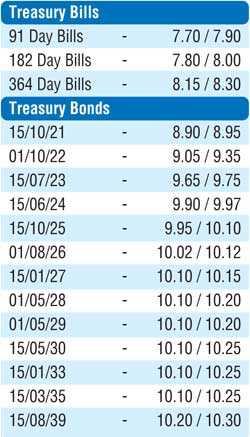

Secondary bond market activity centred on the short end to the belly end of the curve as yields of the 2021’s (i.e. 01.08.21, 15.10.21 and 15.12.21), two 2023’s (i.e. 15.03.23 and 15.07.23), two 2024’s (i.e. 15.03.24 and 15.06.24), 01.08.26 and 15.01.27 maturities were seen increasing to weekly highs of 8.78%, 8.95%, 8.90%, 9.70%, 9.70%, 9.82%, 9.93%, 10.06% and 10.14% respectively against its previous weeks closing levels of 8.45/52, 8.55/60, 8.60/65, 9.30/40, 9.40/45, 9.65/72, 9.72/75, 9.90/95 and 9.95/00.

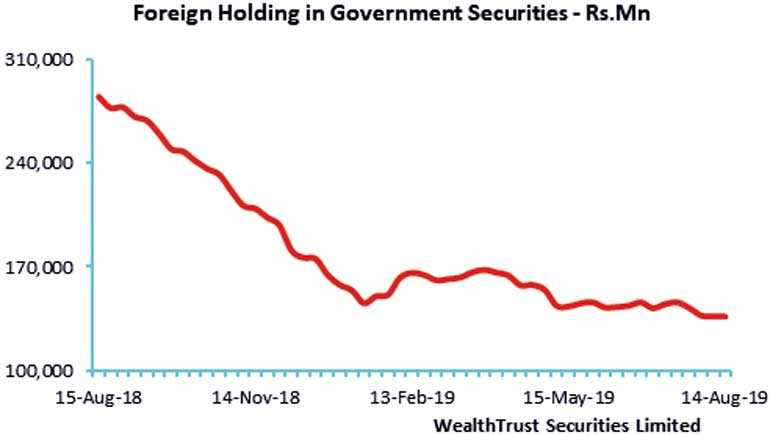

Furthermore, the 01.05.29 and 15.08.39 maturities on the longer end of the yield curve increased to highs of 10.14% and 10.28% respectively as well against its previous weeks closing levels of 9.98/08 and 10.05/25, reflecting a parallel shift upwards of the overall yield curve on a week on week basis. The foreign holding of rupee bonds recorded an inflow for the first-time in four weeks with an increase of Rs. 0.61 million for the week ending 13 August.

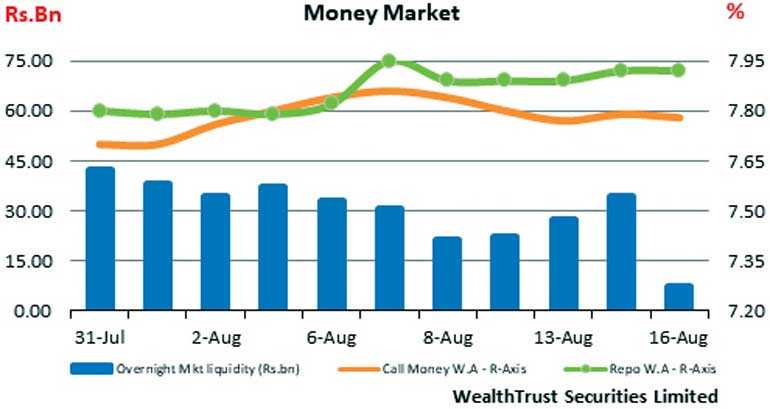

The daily secondary market Treasury bond/bills transacted volume for the first two days of the week averaged Rs. 6.86 billion. In money markets, the overnight call money and repo rates averaged at 7.80% and 7.90% respectively for the week as the average overnight net liquidity surplus in the system stood at Rs. 22.59 billion for the week.

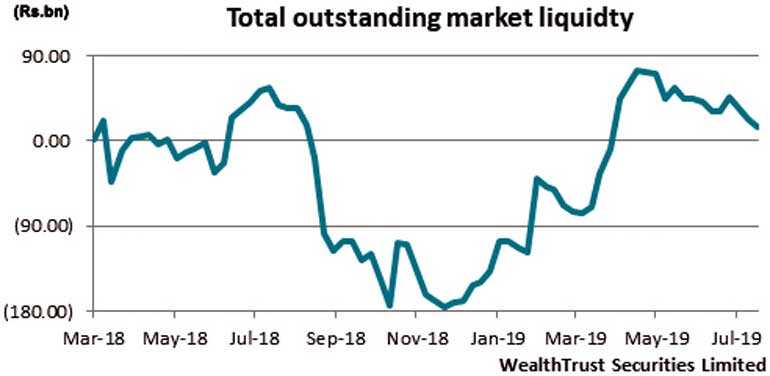

The Central Banks OMO department was seen infusing liquidity throughout the week by way of overnight and term (i.e. seven and fourteen days) reverse repo auctions at weighted averages of 7.70% to 7.89%. In addition, a total of Rs. 2.85 billion was injected by way of outright purchases of Treasury Bills for durations ranging from 256 to 287 days at weighted averages ranging from 7.85% to 7.89% as the total liquidity in the system decreased to a deficit of Rs. 15 billion against its previous week’s surplus of Rs. 22.42 billion.

Rupee dips during the week

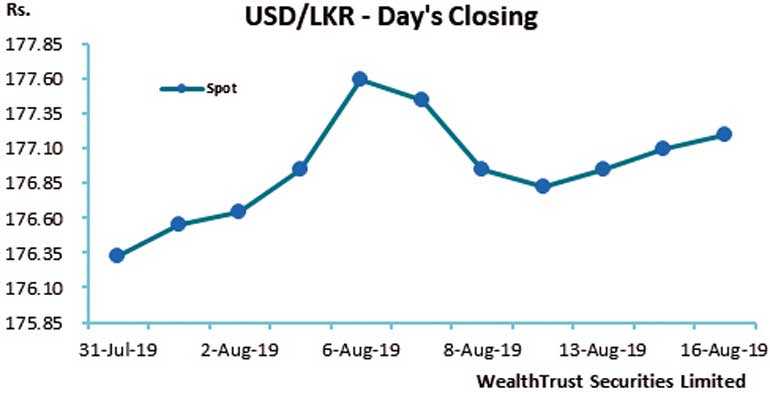

The value of the rupee was seen decreasing during the week to levels of Rs. 177.15/25 on the back of buying interest by banks and importer demand against its previous weeks closing of Rs. 176.80/85.

The daily USD/LKR average traded volume for the first two days of the week stood at $ 104.26 million.

Some of the forward dollar rates that prevailed in the market were 1 month – 177.55/70; 3 months – 178.50/70 and 6 months – 180.20/40.