Monday Jun 01, 2026

Monday Jun 01, 2026

Tuesday, 21 May 2019 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

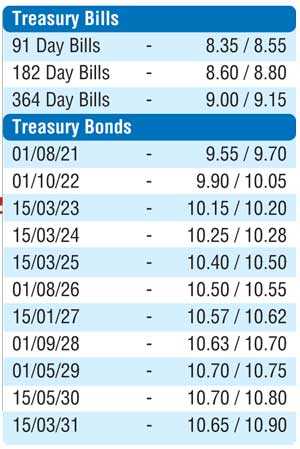

The secondary bond market ending 17 May witnessed a week of volatility, with yields increasing during the beginning of the week on the back of renewed selling interest, and thereafter decreasing towards the latter part of the week, backed by fresh local as well as foreign buying.

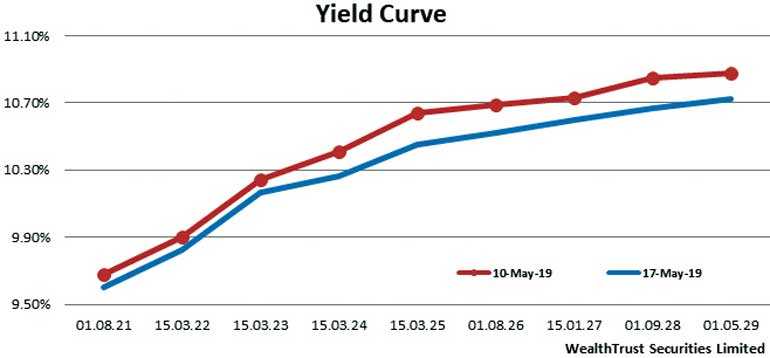

Yields of the 15.07.23, 15.03.24, 01.08.26, 15.01.27 and 01.05.29 were seen increasing to weekly highs of 10.48%, 10.60%, 10.77%, 10.80% and 10.92% respectively during the early part of the week. However, subsequent to the weekly Treasury bill auction, where the weighted average yield of the 364 day bill crashed by 26 basis points to 9.18%, considerable local as well as foreign buying interest returned to the market driving yields down once again. The said maturities were seen hitting weekly lows of 10.23%, 10.28%, 10.60%, 10.60% and 10.80% respectively, reflecting a parallel shift downward of the overall yield curve for the third consecutive week.

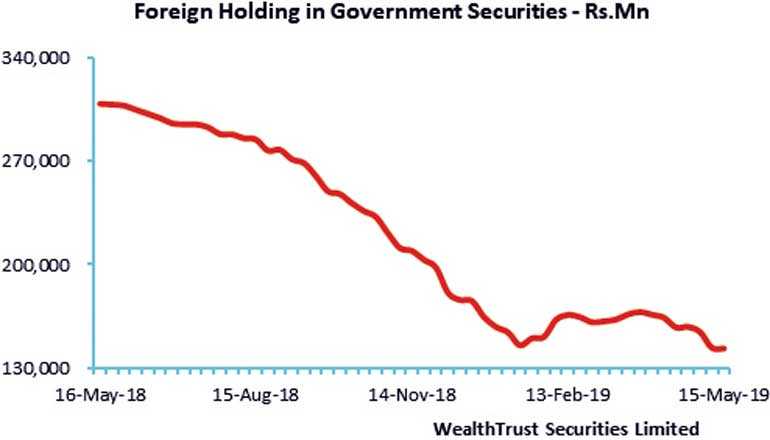

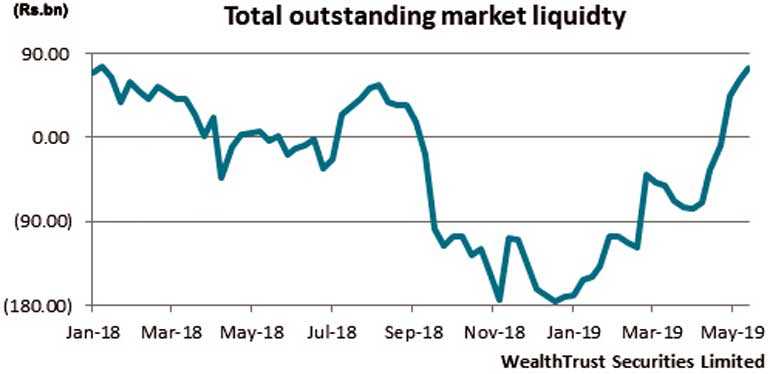

On the back of this momentum, yields were seen hitting weekly lows of 9.60%, 9.68%, 9.88% and 10.00% respectively on the two 2021 maturities (i.e. 01.08.21 and 15.12.21) and two 2022 maturities (i.e. 15.03.22 and 01.10.22) while on the long end of the yield curve the 15.06.27 and 01.09.28 maturities traded at a low of 10.65% and 10.71% respectively. The foreign holding in Sri Lankan Rupee bonds recorded an outflow for the 3rd consecutive week to the tune of Rs. 0.43 billion for the week ending 15 May, with the total money market liquidity increasing further to hit a 70 week high of Rs. 73.99 billion by the end of the week.

The daily secondary market Treasury bond/bill transacted volume for the first four days of the week averaged Rs. 11.40 billion.

In money markets, the average overnight net surplus liquidity in the system stood at Rs. 26.49 billion for the week as the Open Market Operations (OMO) Department of the Central Bank continued to drain out liquidity during the week by way of overnight, two day, three day, four day, five day, six day, seven day and ten day repo auctions at weighted averages ranging from 8.38% to 8.54%. The overnight call money and repo rates averaged 8.39% and 8.49% respectively during the week.

Rupee gains further during the week

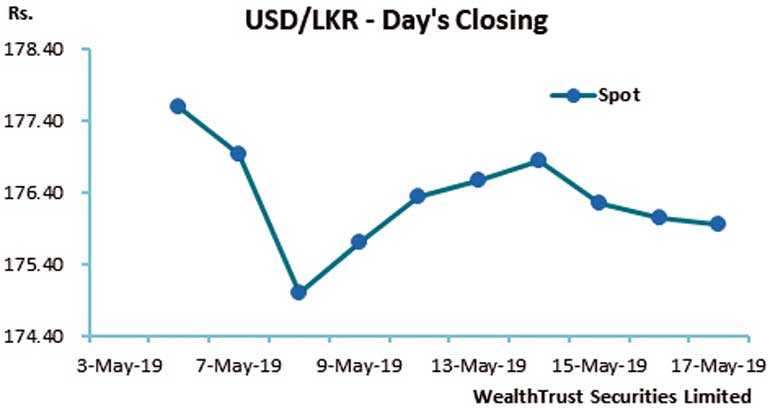

In the Forex market, the USD/LKR rate on the spot contracts were seen closing the week marginally higher at Rs. 175.90/00 in comparison to the previous weeks closing levels of Rs. 176.30/40, subsequent to trading at levels of Rs. 175.68 to Rs. 176.92.

The daily USD/LKR average traded volume for the first four days of the week stood at $ 68.19 million.

Some of the forward dollar rates that prevailed in the market were 1 month - 176.80/95; 3 months - 178.55/70 and 6 months - 181.25/45.