Sunday Feb 22, 2026

Sunday Feb 22, 2026

Monday, 20 January 2020 03:13 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

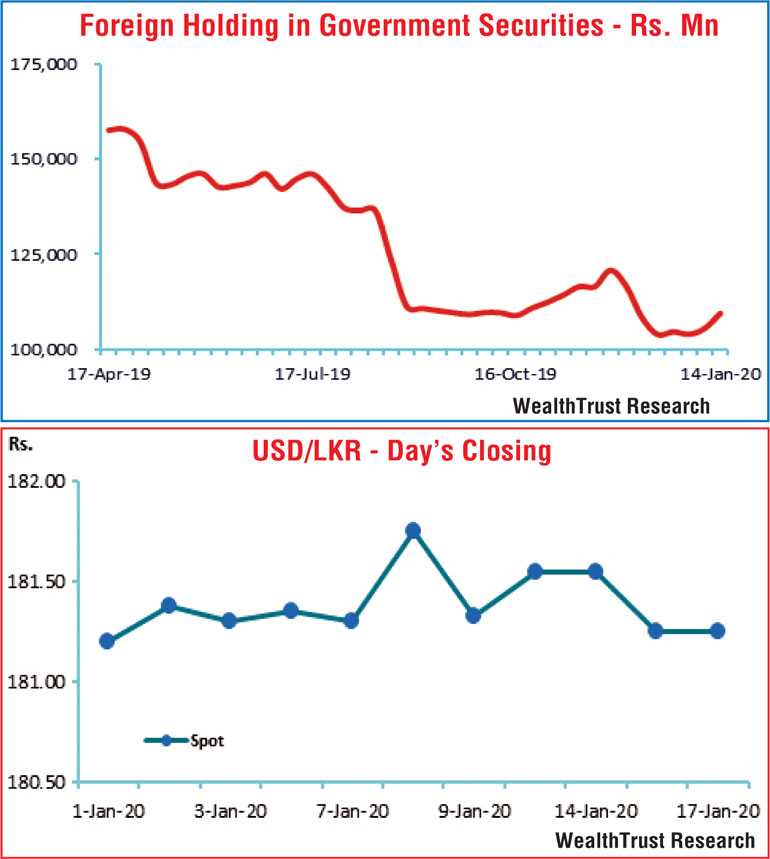

The positive momentum in the secondary bond market continued during the week ending 17 January driven by the impressive outcomes at the primary bond auctions along with the increase in the foreign holding in rupee bonds for a second consecutive week. This resulted in a marginal shift downwards of the overall yields curve.

At the bond auctions, the total offered amount of Rs. 30 billion was successfully subscribed with the two maturities recording impressive weighed average yields while the foreign holding in rupee bonds nudged up by a further by Rs. 3.98 billion for the week ending 14 January.

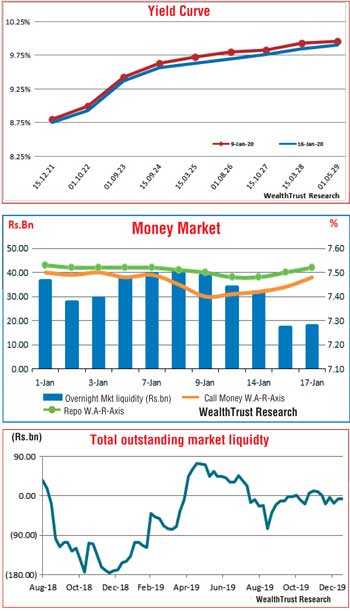

However, contrary to the bond market, the weighted average on the 364-day bill was seen increasing for a second consecutive week, recording a jump of six basis points to 8.58% while the weighted average on the 182-day bill held steady at 8.13%.

Activity in the secondary bond market took place within a narrow range during the week as the liquid maturities of 2023’s (i.e. 15.07.23 and 01.09.23) and 2024’s (i.e. 15.06.24 and 15.09.24) traded within the levels of 9.23% to 9.25%, 9.30% to 9.40%, 9.52% to 9.60% and 9.52% to 9.61% respectively.

Activity was also witnessed on the maturities of 2027’s (i.e. 15.06.27 & 15.10.27), 01.05.29, 15.05.30, 15.01.33, 15.09.34 and 15.05.35 within the range of 9.75% to 9.77%, 9.72% to 9.78%, 9.91% to 9.97%, 9.91% to 10.00%, 10.05% to 10.09%, 10.05% to 10.12% and 10.08% to 10.10% respectively.

The daily secondary market Treasury bond/bills transacted volume for the first three days of the week averaged Rs. 16.76 billion.

In money markets, due to the high overnight liquidity surplus in the system during the early part of the week, the Domestic Operations Department (DOD) of Central Bank was seen draining out liquidity on an overnight basis at weighted average yields ranging from 7.45% to 7.46%. Nevertheless, it injected liquidity on Friday on an overnight basis at a weighted average rate 7.52%.

The overall liquidity in the system decreased further to record a net deficit of Rs. 7.23 billion against its previous weeks of Rs. 6.24 billion. The overnight call money and repo rates averaged 7.44% and 7.50% respectively for the week.

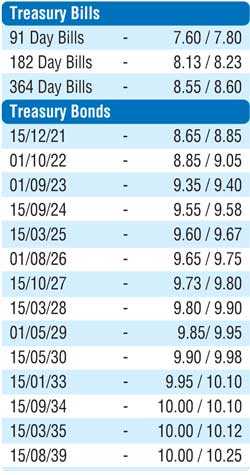

Rupee appreciates marginally

The USD/LKR rate on spot contracts was seen closing the week marginally higher at Rs. 181.20/30 in comparison to its previous weeks closing of Rs. 181.30/35, subsequent to trading within a high of Rs. 181.08 and a low of Rs. 181.63 during the week.

The daily USD/LKR average traded volume for the first three days of the week stood at $ 97.10 million.

Some of the forward dollar rates that prevailed in the market were 1 month – 181.75/90; 3 months – 182.70/90 and 6 months – 184.25/55.