Thursday Feb 26, 2026

Thursday Feb 26, 2026

Wednesday, 4 December 2019 00:29 - - {{hitsCtrl.values.hits}}

In its series of Recommendations from page 911 to page 922 of its Report, the Presidential Commission to Inquire into the Bond Scam (Bond Commission) has, inter alia, recommended as follows:

“As set out earlier, there is adequate evidence before us to form the view that, there is a likelihood that some irregularities have taken place in the acceptance of Direct Placements prior to 2015.

“Therefore, we recommend that, an appropriate investigation be carried out to ascertain whether there were significant irregularities in the acceptance of Direct Placements by the Public Debt Department during the period 2008 to 2014 and, if so, to identify the officers of the Public Debt Department and the superior officers of the CBSL, the Primary Dealers and any other persons who were responsible for such irregularities. Such an investigation should also seek to compute the losses, if any, which may have been incurred by the Government as a result of any such irregularities. A Forensic Audit may be appropriate.”

A careful examination of the above Recommendations shows that what the Bond Commission Report is stating is that:

There is “adequate evidence” (evidence not specified) before the Commission to “form the view” (not a finding, just an opinion) that “there is a likelihood” (no certainty, just a possibility) that “some irregularities” (irregularities not specified) have taken place in the acceptance of Direct Placements prior to 2015.

Based on the above-mentioned tentative “likelihood”, the Bond Commission proceeded to recommend that a “Forensic Audit” be carried out to ascertain whether there were (in fact) “significant irregularities” “in the acceptance of Direct Placements by the Public Debt Department during the period 2008 to 2014”.

In this connection, it is very strange that the Bond Commission has not considered the following factual certainties and not “likelihoods”, in making their recommendation to carry out a Forensic Audit.

a. The Treasury bond issues during the period 2006 to 2014 had already been subject to the routine audits by CBSL’s Internal Audit Department, the audits of the “international” auditors of the CBSL appointed by the Auditor General as well as by the “external auditors” of the Auditor General’s Department. In addition, these Bond Issues have been closely scrutinised by the Auditor General in response to a specific request made on 19 August 2016 by the then Finance Minister Ravi Karunanayake, under Section 43 (2) of the Monetary Law Act. The Auditor General’s Report dated 16 January 2017, which reported on such specific examination, did not highlight any instances of wrongdoing that would have necessitated or demanded a forensic audit.

b. Although not available by 30 December 2017 (the date on which the Commission handed over its Report to the President), it is noted that a detailed Report dated 30 January 2018 by a CBSL Deputy Governor which provided observations on the Auditor General’s Report, had also concluded that:

In addition to the earlier stated recommendation, the Bond Commission had proceeded to make the following recommendation as well:

“In view of the observations made earlier in Chapter 16, consideration may be given to whether the operations and management of the CBSL prior to 2015 should be examined, particularly with regard to:

(a) the reasons for the Losses incurred by the CBSL in the years 2013, 2014 and 2015, and

(b) the Transactions entered into by the EPF on the Colombo Stock Exchange during the period 2010 onwards.”

The Bond Commission’s recommendation to inquire into “the reasons for the losses incurred by the CBSL”, are totally and embarrassingly misplaced, since the main note to the Financial Statements of the Central Bank, reads as follows:

“The Central Bank was established as the authority responsible for the administration, supervision and regulation of the monetary, financial and payment systems of Sri Lanka under the Monetary Law Act. In accordance with this Act, the Bank is charged with the responsibility of securing the core objectives of economic and price stability and financial system stability.

“The basis of accountability for the Central Bank and the success of its operations therefore would be the effectiveness of its policies and operations leading towards the achievement of its core objectives and not necessarily its profitability. These statutory objectives are the fundamental features that distinguish the Central Bank from any other entity, private or public.

Accordingly, profitability related approach, if adopted by the Central Bank, could result in the Bank pursuing profits while compromising its core objectives, since it has the unique ability to create its own profits through its monetary policy activities, which could influence interest rates and exchange rates. It therefore follows that the Central Bank’s objectives of economic and price stability and financial system stability need to be distinguished and detached from the pure profitability objective which should essentially be incidental or academic only.”

The economic results achieved by the CBSL in each of the years 2013 and 2014 have been highly successful in terms of the objectives of the CBSL. At the same time, in accordance with the Monetary Law Act, the CBSL had made substantial “profits” and made healthy distributions of its surpluses to its shareholder the Government, although in terms of the International Financial Reporting Standards (IFRS) the Central Bank may have recorded “losses”.

It is likely that this fact may have already dawned on the authorities and that is probably why they may not have pursued a “forensic audit” in this connection, given the acute embarrassment of even considering such an audit, in the surrounding circumstances.

In addition, the red herring raised by the Bond Commission regarding the transactions of the EPF during the period 2010 onwards has been the subject matter of a Fundamental Rights Petition before the Supreme Court initiated by 11 Trade Unions, which had been already summarily dismissed by the Supreme Court.

In fact, that recommendation was strangely based upon the Bond Commission being guided by the following type of un-substantiated, un-verified and un-evaluated considerations:

Further, in arriving at this recommendation, the Bond Commission has referred to a “significant” fall in the All Share Price Index (ASPI) in 2011, and attributed such fall to the EPF. In doing so, the Commission seems to have over-looked the fact that the entire world was undergoing a massive economic and banking crisis in 2011, and the main reason for the “huge drop in market value” and the reduction in the ASPI was not the “transactions by the EPF”, but the global and regional conditions. If therefore, the Commission had cared to study the behaviour of regional and global stock markets during that period, the Commission may have being spared the embarrassment of reaching this inaccurate “finding”.

As articulated by the present Governor Dr. Indrajit Coomaraswamy in the Report of the EPF for 2014, the EPF invests in a “portfolio basis”, and the salient features of such basis may be best explained by using a few extracts from the judgement of Justice Sripavan (later Chief Justice) in the Greek Bonds Case of Senasinge vs. Cabraal.

“If all investments are maintained as risk free investments the return would be negligible. The Central Bank therefore has to select a mix of low risk and risk bearing investments expecting a reasonably high return.”

“We must not forget that in complex economic policy matters every decision is necessarily empiric and therefore its validity cannot be tested on any rigid formula or strict consideration. The Court while adjudicating the constitutional validity of the decision of the Governor and Members of the Monetary Board must grant a certain measure of freedom considering the complexity of the economic activities. The Court cannot strike down a decision merely because it feels another policy decision would have been fairer or wiser or more scientific or logical. The Court is not expected to express its opinion as to whether at a particular point of time or in a particular situation any such decision should have been adopted or not. It is best left to the discretion of the authority concerned.”

When reading the dicta in that case as above, it is clear that the Commission has failed to realise the fundamental nature of a “portfolio” basis of investment. Sadly, it must also be pointed out that the Commission has also not appreciated the physical reality that when the Colombo Stock Market recovered in 2014, the EPF’s portfolio had recorded a massive unrealised Capital Gain amounting to Rs. 20.2 billion, as shown in the EPF Financial Statements for 2014. Such a Capital Gain proves that the Commission’s conclusions were completely without foundation, and were hopelessly erroneous, since the EPF portfolio had actually shown a “huge” increase in market value by 2014, and not a “huge” drop market value as stated by the Commission.

If only the Commission had cared to look into this matter further before rushing to conclusions, the Commission would have also noted that the EPF’s Annual Report for 2014 contains a statement and a Performance Review by the present Governor Dr. Indrajit Coomaraswamy which observes as follows:

“Equity Portfolio

Equity portfolio which consists of both listed and unlisted equities, increased by Rs. 23.8 million (32.7 percent) from Rs. 72.8 billion in 2013 to Rs. 96.6 billion in 2014 due to new investments both listed and unlisted equities. The equity portfolio consisted of an investment portfolio of Rs. 94.7 billion and a trading portfolio of Rs. 1.9 billion at cost as at end of 2014.

EFF continued to maintain a well-diversified Available for Sale (AFS) portfolio consisting of fundamentally sound companies, especially in the sectors of Banking and Finance and Insurance, Hotels and Travels, Diversified Holding, Manufacturing, Construction and Engineering, Power and Energy and Telecommunications sectors listed on the CSE.”

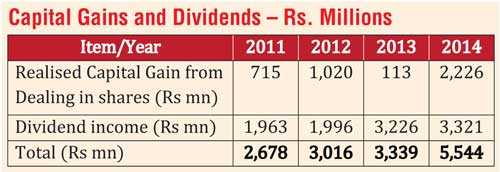

The EPF Annual Reports for the relevant years had also shown the Realised Capital Gains and Dividend Income during the several years was as follows:

The Performance Review of the EPF Annual Report 2014 further describes the challenges facing Risk Management, and in this regard, the “Overview” and the “Market Risk” paragraphs may be of particular relevance and are reproduced below:

“Overview

“EPF is a systemically important entity in the financial sector in Sri Lanka that manages long term savings of private and semi-government sector employees with the objective of maximising retirement benefits to its members. Therefore, management of risks associated with the Fund is critically important for the members as well as for the entire financial system of the country. The EPF embraces risk management, as an integral component of its investment, operations and decision-making process”.

“Market Risk

“Market Risk is the potential of loss from changes in the market value of portfolios and financial instruments due to movements in interest rates, foreign exchange and equity prices. The market risk faced by the Fund primarily arises from interest rate risk and equity price risk.

“If the general interest rates of the economy were to increase, yields of Treasury bonds will follow, causing prices of bonds to drop and value of the trading portfolio to deteriorate. This is the interest rate risk faced by the Fund. However, this has been mitigated by selecting Treasury bonds of varying maturities, limiting the size of the trading portfolio and re-balancing the portfolio occasionally.

“The equity price risk is the reduction in the value of equity portfolio due to the decline in share prices. This is inherent risk of equity investments which has been mitigated by investing in fundamentally sound stocks with robust value. Further, the listed equity portfolio has been diversified into different sectors including Banking, Finance and Insurance, Hotels and Travels, Construction and Engineering Manufacturing and Telecommunication. Further, the market risk on the listed equity portfolio is relatively low on the overall Fund since exposure to the equity market is approximately 6 per cent of the total portfolio of the Fund as the Fund makes appropriate adjustment to its portfolio from time to time as and when necessary.”

In the background of the above, it is clear that the Commission seems to have accepted the allegation that the EPF has indulged in “pumping and dumping”, without factual evidence, despite the Supreme Court ruling of FR Case No: 587/12 which has dealt with the identical matters referred to by the Commission. Further, the Commission seems to have also ignored or missed the massive unrealised profit that the EPF portfolio had generated by end 2014, while also disregarding Justice Sripavan’s (later Chief Justice) dicta in Senasinghe vs. Cabraal (SCFR 457/2012, SC Minute 18.09.2014).

It is now well known as to how the CBSL top management was intimidated and coerced into withdrawing its objections to the series of “Footnotes” placed by several UNP MPs to the Handunnetti COPE Report on the Bond Scam, at the insistence of “Temple Trees”, the office of the Prime Minister. It has also come to light in more recent times, as to how the then Director General of the Bribery Commission and now Solicitor General Dilrukshi Dias Wickremesinghe had been coerced into instituting legal action against certain selected individuals due to pressure from “Temple Trees”.

Another Solicitor General Suhada Gamlath is also on record in recent times, as to how he too had been intimidated by certain Ministers while at “Temple Trees” to quickly indict certain politicians even when he stated that there was insufficient evidence to do so. In addition, just a few days ago, the former Chief of the FCID Senior DIG Ravi Waidyalankara revealed as to how he was coerced into carrying out investigations on selected politicians and officials of the “Pre-2015” era by a Unit that operated from “Temple Trees” which was coordinated by a “politically aligned” Senior Lawyer.

In the meantime, there are already several concerns that have been expressed re. the so-called Forensic Audits now being carried out by the Monetary Board, where suspicions have been raised that the concept of the “Forensic Audit” had been skilfully planted upon the Bond Commission via a suggestion by the former Prime Minister without any data and information, so that such an Audit can (hopefully) distract attention from the massive Scams of 2015 and 2016, to shift blame to others, and to “buy time” for the Mastermind.

A Forensic Audit is an investigation of fraud, corruption and/or other economic crime, particularly where the integrity of senior management has been called into question. Such an Audit requires a thorough, professional and independent approach, since the affected organisation’s stakeholders and possibly regulators will require the reassurance of an effective and independent response, should an issue arises that poses regulatory, financial or reputational risk.

Accordingly, the independence and professional basis of the effort is absolutely vital. Even in error, what the Bond Commission has recommended is a Forensic Audit pertaining to the CBSL. On that basis, if such a Forensic Audit is to be carried out, it must be carried out under the supervision and authority of an “independent” body or agency, and certainly not by any person connected to the CBSL or under the authority of the CBSL. It is only then that the integrity of a Forensic Audit could be ensured.

In keeping with that pre-requisite, the Monetary Board of the Central Bank or any of its officers must not be involved in any manner whatsoever in drawing up the Terms of Reference, or calling for bids, or short-listing of possible Forensic Auditors, or the planning and execution of such Forensic Audits, or providing logistical support for that effort. This is particularly so, since it is the Monetary Board that has been accused by the Bond Commission as being one of the possible “guilty” parties pertaining to the scam, and/or any other misdemeanour.

In fact, the Members of the “Post-2015” Monetary Board are likely to be requested to account for the staggering losses and damages from 27 February 2015 to 27 July 2017 due to the voluntary abrogation of the time-tested “auction cum direct placement” method of issuing Bonds from 27 February 2015 onwards, the very poor performance in Foreign Reserve Management since 2015, and the massive reduction of value of the EPF Equity Portfolio since 2015.

Hence, in the interest of “good governance” and avoidance of “conflict of interest”, the members of the Monetary Board and the staff of the CBSL should not have been involved in any matters connected to the Forensic Audits.

However, just the opposite seems to have taken place, and according to information available, it appears that it is the Monetary Board itself that has commissioned the forensic audit/investigation, which is totally in conflict with the fundamentals of a proper Forensic Audit. In Sinhala, there is a pithy saying, “like inquiring about a theft from the thief’s mother!” In like manner, if the Monetary Board has been in charge of the “Forensic Audit”, it would surely be a similar situation since the suspect is placed in charge of the investigation.

When an external auditor to audit according to International Financial Reporting Standards (IFRS) is appointed for the CBSL, such appointment is done by the Auditor General. It is not the Monetary Board or the CBSL which makes such appointment or selection. In fact, there is an extensive, transparent process which the Auditor General follows in selecting a private sector Auditor and awarding such a contract, even in the case of a routine audit.

Not only has this fundamental requirement been recklessly and arbitrarily abandoned, suspicions have also mounted that certain officials of the CBSL who are known to be politically aligned towards former Prime Minister Ranil Wickremesinghe and his political party, are the persons who have been entrusted with the task of liaising with the Forensic Auditors. In fact, there is information that such persons are already making use of this new opportunity to shift the focus away from the real culprits and to implicate others via these Forensic Audits

The CBSL has already suffered serious reputational damage by the partisan actions of former Deputy Governor P. Samarasiri who was arbitrarily appointed as the Senior Deputy Governor and entrusted with the responsibility of “covering-up” the first bond scam by Governor Mahendran. There is also evidence that the former Prime Minister and the former Minister of Finance attempted to absorb P. Samarasiri into the Ministry of Finance when he retired even though it was publicly known that Samarasiri was involved in the bond scam. In a similar manner, there is a legitimate fear that the certain current CBSL officials may also be carrying out certain dubious “services” on behalf of vested interests.

Considering the recent revelations of the roles played by other key officials as is now being revealed by two Solicitor Generals, as well as by the former FCID Chief, the Monetary Board would do well to review their own role, as well as review the selection of the person who had been “coordinating” the “Forensic Audit” from its own end, even though the Forensic Audit itself is a totally faulty decision.

On numerous occasions, the Monetary Board has directly and/or indirectly defended the bond scam. It had got the CBSL Senior staff to withdraw the challenge to the COPE Report Footnotes. It supported the stance of Governor Mahendran on numerous instances when it was known he was on a mischievous adventure. It restored the old method of bond issues, but deliberately misled people to think it’s a new method.

In particular, the role of the former Treasury Secretary, Dr. R.H.S. Samaratunga has been highly suspicious, since he was a Member of the Monetary Board from the day the first bond scam took place. In fact, Samaratunga has been serving on the Monetary Board when the second Scam took place, as well. In addition, several other current Appointed Members have been in the Monetary Board when the second bond scam was carried out, while Governor Dr. Indrajit Coomaraswamy took more than 13 months to restore the time-tested method of issuing Bonds via the “auction cum direct placement” method.

Accordingly, in the interest of ensuring independence, present Governor Coomaraswamy and the Monetary Board cannot and should not have authority to carry out or lead the Forensic Audit, because it is the Monetary Board that has been named as being directly responsible for the bond scam and closely associated with its cover-up.

In these circumstances, almost all current Monetary Board Members are significantly compromised and may soon be even accused of being involved with the bond scams and/or at least involved in the “cover-up”. Therefore, they cannot, in any way be placed in charge of a Forensic Audit which is supposed to be an independent investigation.

Finally, it must be re-iterated that any Forensic Audit, if ultimately considered desirable, should be placed in charge of the Auditor General, and no one else. The payment for the Forensic Audit should be made to the Auditor General by the Government on a special vote, and not by the CBSL. The entire process should be handled by the Auditor General if the time honoured legal principle that “justice must not only be done, but must also be seen to be done” is to be followed.

(The writer is former Governor, Central Bank of Sri Lanka.)