Friday Jun 05, 2026

Friday Jun 05, 2026

Monday, 21 September 2020 00:30 - - {{hitsCtrl.values.hits}}

Ashan Jayasinghe at work

Just one flower is enough to make an impact

‘Let thousand flowers blossom’ was the catchy slogan of China’s leader Mao Tsetung in 1950s. His intention was to create a critical pool of youngsters in China so that they could take that country from poverty to prosperity. In the last two decades, however, people like Phil Knight (Nike), Steve Jobs (Apple), Bill Gates (Microsoft), and Mark Zuckerberg  (Facebook) have proved that a country does not need a thousand flowers to make an impact.

(Facebook) have proved that a country does not need a thousand flowers to make an impact.

A few who always think new and big could do the job quite easily if they are persistent enough to pursue their goal no matter whether it is rain or sun. The COVID-19 pandemic, thought to be an irreparable disaster by many, has offered such a rare opportunity to innovative youngsters to change the world. I met such a youthful innovator who has sought to convert adversity to prosperity for all.

From invention to innovation

His name is Ashan Jayasinghe, just turned 33 years this year. His contribution? He has developed, together with another youngster filled with inventive spirit, two web platforms aiming at filling the information gap in the financial services industry. One is for banks proper, titled AnybanQ.lk. The other, titled AnyfinanZ.lk, is for all other financial institutions. I asked him why his partner’s name is not disclosed. Ashan laughs and says: “He’s shy and doesn’t want to come to limelight. But he is the brain behind technology. What I do is producing it commercially”.

The duo reminds me of the famous Apple brand creators. It was the tech mind of Stephen Wozniak that invented the first Apple Mackintosh Desktop. But he remained anonymous till recently. His partner, Steve Jobs, did the entrepreneurial part launching it commercially.

This distinction between invention and innovation was brought to the mainstream economics by Austrian-American economist Joseph Schumpeter in the first half of the last century. According to Schumpeter, inventions are done by scientists, engineers, technologists or management Gurus by coming up with a new product, service, management technique or system development. They remain prototype ideas until they are commercially produced by entrepreneurs through a process which Schumpeter called ‘innovation’. Therefore, for a product to see the light of the market, both inventors and innovators should get together. Now we have Ashan as the innovator and his partner, the inventor.

Being hyperactive is a blessing

How did Ashan get into entrepreneurship? I asked him. “I was a hyperactive child in my school days,” he began his narration. “I always wanted to do things differently. To an ordinary person, they’re daydreams. But for me, they were doable works. And they were also crazy ideas. One such thing was that I thought to solve the traffic problem, why not move the roads and pavements, instead of vehicles? Today, this’s as crazy as walking to the moon. But I entertained such thoughts in me and looked for ways to accomplish them.”

If Ashan is a crazy boy, even Sir Arthur C. Clarke should also be a crazy one. In 1946, he let out a crazy idea of shooting a satellite to the orbit of the earth and use it as a tall antenna to transmit information back and forth. 25 years later, it became a reality, and, thanks to him, we now have satellite communication. Another seemingly crazy idea which Clarke had pronounced was the building of a space elevator to other planets. History has enough examples of persecuting those rebels because they had failed to conform to the norms of society. But society progresses not because of conformists, but because of so-called rebels.

A dynamic and living society should always welcome rebellious ideas. Those ideas will challenge the existing social, political, economic or cultural order. The extant society that relies on old views may resent such challenges. But those challenges would deliver disruptions and those disruptions will deliver a new order to society.

A latecomer to higher education

Ashan is a latecomer to higher education. He says that his completing both O/L and A/L was a miracle because he was not a classroom boy. He was in the field, in the world of athletes. After A/L, it was a futile attempt at trying out all kinds of professional courses, like IT, marketing, executive management, to which youngsters are driven not with a passion but to go by the popular fashion. He had dropped out of them in the midway. What happened next? I asked him.

A failure of dozen trades

“I joined the job market at an early age,” says Ashan. “I’ve worked in many places, mobile phone companies, international banks, IT companies, to mention but a few. But I was asking myself: ‘Am I doing the correct thing?’ I realised that I cannot just continue to be employed under somebody. I must do things big and novel. For that, I must advance myself in education which I had abandoned a decade earlier. Then, I should leave employment and try out my own business.”

I reminded him that he had unsuccessfully tried out many professional courses earlier. That discouraging experience would have convinced him that he was not a good learner. Besides, he had started earning and that new money in his hands would have spoiled him. How did this change happen in his life? I asked him.

Back to school with an armoury of experiences

“It was a chance meeting with a friend of mine. He had been doing a graduate diploma in management offered by a local institution but accredited by London based educational qualification provider, Pearson Group. That diploma was recognised as equivalent to a university degree by foreign universities for entry to their MBA programs. He coaxed me to join this program. So, I started going to school again while working.” He stopped midway as if a lump had blocked his throat.

After some time, he began his narration again. “I was in the program, but I soon found that I was losing my eyesight. To my horror, I was diagnosed having been infected by a rare eye disease called Uveitis. It was the first time I even heard of the name of the disease. To save my eyesight, doctors put me on strong steroids continuously. That course of medication was effective, but it created other problems like losing immunity, infecting the liver and so on. I was losing my bone mass. It was the sportsman within me that held me out.

“One day, just before a crucial examination, I blacked out several time in the night. I thought that was the end of my academic career. But in that paper, I got a distinction and it boosted my morale to a new height. I completed the graduate diploma in management, enrolled myself in an MBA degree program offered by UK’s Edinburg Napier University and completed it with flying colours. My results were so good that I was asked to deliver the graduation speech on behalf of all MBA holders at the convocation (available at: https://www.youtube.com/watch?v=bbUNnha_q7w&feature=youtu.be).

“This graduate diploma in management and Edinburg Napier MBA were instrumental in rekindling the entrepreneurial spirit that had been there in me throughout. So, I left the job and started my own business in providing IT services to customers.”

A digital financial product

That was quite a journey for a young man who had been resolved not to undertake any formal education anymore. It shows that the blossoming of a flower could happen at any time, provided the right conditions are there. He is doing well in his new start-up business, Fintech Digital Ltd., providing tech services to financial institutions. But what prompted him  to go into a digital financial product of a wider dimension? True that there are thousands and thousands of potential banking customers there. True that there are hundreds of financial institutions there. But trying to connect them together is a suicidal job. It is more prone to be a failure than to be a success. I asked him why he chose such a fintech product?

to go into a digital financial product of a wider dimension? True that there are thousands and thousands of potential banking customers there. True that there are hundreds of financial institutions there. But trying to connect them together is a suicidal job. It is more prone to be a failure than to be a success. I asked him why he chose such a fintech product?

Learning from experiences

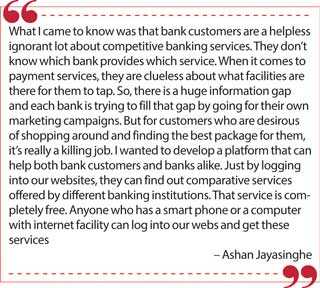

“I had about 10 years’ experience in customer and relationship management in an international bank. One to two years of experience in mobile phone and IT companies. What I came to know was that bank customers are a helpless ignorant lot about competitive banking services. They don’t know which bank provides which service. When it comes to payment services, they are clueless about what facilities are there for them to tap. So, there is a huge information gap and each bank is trying to fill that gap by going for their own marketing campaigns. But for customers who are desirous of shopping around and finding the best package for them, it’s really a killing job. I wanted to develop a platform that can help both bank customers and banks alike. Just by logging into our websites, they can find out comparative services offered by different banking institutions. That service is completely free. Anyone who has a smart phone or a computer with internet facility can log into our webs and get these services.”

Inclusive financial services via technology

Financial services are normally available only to the rich and affordable customers. But economic growth requires everyone, irrespective of income or educational levels, to have access to them. Central banks in emerging countries, including our own central bank, have been trying to develop strategies to make financial services accessible to all, a project dubbed as inclusive banking. But the lack of credible information at the tip of potential customers has been a hindrance to this enterprise embarked on by central banks. Ashan’s web platforms seek to fill this gap in information.

COVID-19 is an opportunity

“Why do you think that your platforms are the way forward for Sri Lanka?” I asked him.

“This has become essential under the new normal that we have to go through in the post-COVID-19 era,” he says. “Since the return to normalcy is postponed day by day, there’s a barrier created between the banker and the customer. I’ve witnessed that when a customer visits a bank, he is kept about a meter away from the bank official. The closeness which should be there between the two parties is not adhered to in this so-called new normal. It’s an embarrassment to both. My platforms break that barrier. A potential customer can learn everything he has to know about all the banks without stepping out of his house.

“Making that information available in a single platform is convenient to him on many counts. One is that he doesn’t have to incur any search cost now. In the previous model, he had to visit a number of banks to get that information. Time is costly and if you can help him to keep it at a minimum, you are in fact doing a good service to him. This’s beneficial to the banks too. They can ensure that customers won’t keep a distance from them because of the inconvenience to visit banks in person. It will cut down their advertising budgets too. It’s also beneficial to the nation. When individual banks engage themselves in cut-throat competition by undertaking their own advertising campaigns, there’s a lot of resources being wasted for nothing. If this advertising can be done from a single place for all banks together, it saves the nation’s scarce resources too.”

Supporting Central Bank’s initiative to go for fintech

An IT platform is not a static one. It has to change all the time meeting new demands and requirements. That’s why App developers are releasing updates from time to time. I asked Ashan about his plans to update the present platforms. “At present, the Central Bank has revolutionised the country’s retail payment system by introducing payments through QR codes. The challenge before the Central Bank as well as commercial banks is to expand the network of participating merchants and willing customers. Each bank is required to do its own marketing for this. My platforms will be updated soon to accommodate QR payments. When it is completed, a customer who can log into our web through his smart phone would be able to use the QR code to make payments out of his bank account. Through this update, we’ll help the central bank to make our physical currency a true digital currency.”

Next step is to go live

‘What is the next step?’ I asked Ashan. “We’re ready to go live as soon as possible once the country’s financial institutions have come on board. We’re at present in negotiation with them. We hope to finalise it soon.” He spoke exuding confidence from every word he uttered.

Starting small and making it big

Ashan is a young start-up entrepreneur. All entrepreneurs who have now become giants did start their businesses very small. For instance, Phil Knight of Nike Sports Shoes fame began his business just by borrowing $ 50 from his father. Steve Jobs built up his Apple empire by working from the backyard carpentry shop of his adoptive father. Facebook got its birth in a student dormitory of a few dropout students from the university. Ashan also has started from a very small base. But he thinks big. This is one of the prime qualities of a successful entrepreneur, as Nepal’s first billionaire Binod Chaudhary revealed in his autobiography ‘Making it Big’.

(The writer, a former Deputy Governor of the Central Bank of Sri Lanka, can be reached at [email protected].)