Sunday Jun 07, 2026

Sunday Jun 07, 2026

Wednesday, 18 September 2019 00:00 - - {{hitsCtrl.values.hits}}

With the recent announcement of releasing credit scores of banked citizens commences a new chapter of the country’s lending industry. The General Manager of the Credit Information Bureau (CRIB) Nandi Anthony stated that the Bureau plans to release credit scores of banked citizens from August 2019  onwards (Daily Mirror, 25 July 2019). This is long overdue. The new application certainly uplifts the country to the next level as far as credit evaluation myths are concerned. According to Anthony, the facility will be further extended to all citizens by late 2020.

onwards (Daily Mirror, 25 July 2019). This is long overdue. The new application certainly uplifts the country to the next level as far as credit evaluation myths are concerned. According to Anthony, the facility will be further extended to all citizens by late 2020.

Under the circumstances, all lending institutes will have to redefine their credit disbursing calculations and approaches. It makes the duties of credit managers and officers easier but also challenging in a different way. The published article further said that the credit scores are calculated using a process which ranges from 250 to 900. When the probability of default is high, the score is low and when it is low the score is high. In layman’s terms, if you pay your dues on time you get a high credit score and if you don’t pay your dues on time you get a low credit score. When the score is high you are on a better footing to attract decent rates of interest from lending institutions. The CRIB also expects the credit scores to influence the decisions of financial institutes in offering attractive rates for creditworthy customers. They could demand lower interest rates for credit based on their positive credit scores.

Disadvantages

On the face of it, the picture looks very rosy. There are approximately 33 banks and 48 finance companies in Sri Lanka with a workforce of around 88,000. As mentioned earlier, all managers and officers who deal in credit in these financial institutions have a challenging task ahead. They would certainly be asked to consider a reasonable weightage to the solvency of their customers during the credit evaluation process based on the Individual Credit Score allocated by CRIB. The challenge starts there.

1 Third party involvement

Back in the 90s, I was working for a leading financial institute in the country which had a large customer base. With the intention of improving business volumes, the IT Department was asked to filter the customer base centred on their repayment pattern and send them letters offering enhanced and fresh credit facilities. The customers who had paid over a period of two years without a single default were selected for the implementation.

Guess who came first? The first five were customers who had obtained facilities and sold their vehicles to third parties without the consent of the company. The contracts had been serviced promptly by the new users. The system couldn’t factor in this scenario as it was a software which merely identified the finest customers from the base. No human intervention had been linked to the process. However, the credit officers concerned subsequently managed to identify them.

This why I said the credit managers and officers will have a daunting task ahead of them if they are asked to go by a system-generated credit score alone. Like the situation elaborated above, there are situations in the market where some loans are being paid by third parties. The loan is not being paid by the customer himself who obtained the facility but by a third party who operates behind the scenes, or taken on behalf of another person who doesn’t have adequate documents to obtain a financial facility. In most cases, it is done on-fee basis by the dummy applicants. In some instances, the original party makes payments for a couple of months and then transfers the asset off the record. The custody of the asset is taken over by a third party.

Another common reason in the market to service loans on third party basis is due to tax and legal complications of the new party. Hence, they mutually agree to service the loan on the original owner’s name. Given these conditions, the Individual Credit Score makes no impact on the credit officer’s credit opinion of an individual. Hence, credit officers and managers should detect such situations, inform their superiors and convince them to make better credit decisions.

2 Informal borrowings

Similarly, CRIB doesn’t have the information pertaining to informal borrowings and their monthly rental commitment of customers. CRIB is equipped with only the data of formal borrowings. However, we  shouldn’t forget the fact that there exists a vast but undisclosed money lending market in the country. It is evident in most cases that go bad that the genuine information which would have been useful in evading doubtful lending had not been surfaced during the evaluation process – particularly information concerning customers who have borrowed informally from local money lenders and institutes. Such monthly commitments create a colossal deficit in the cash flows of customers.

shouldn’t forget the fact that there exists a vast but undisclosed money lending market in the country. It is evident in most cases that go bad that the genuine information which would have been useful in evading doubtful lending had not been surfaced during the evaluation process – particularly information concerning customers who have borrowed informally from local money lenders and institutes. Such monthly commitments create a colossal deficit in the cash flows of customers.

There is a trend building in the country of settling formal borrowings with informal borrowings to clear irregular CRIB records and then reverting back to formal borrowings. The cash flow issues of such customers remain unchanged though the CRIB records are clear. The credit managers and officers should bear in mind that the intended Individual Credit Score is generated based purely on the repayments of formal borrowings available to CRIB. Hence, credit managers and officers should do their homework during the evaluation process to find out the actuality without depending on the Individual Credit Score alone.

Advantages

1 Inadequate documents

However, there are many positive aspects of the Individual Credit Score. We have seen many customers who are capable of servicing rentals comfortably but don’t possess adequate documents to prove their creditworthiness. Under such circumstances, the credit score plays an important role. When they have a history to influence their credit rating, obtaining a fresh or enhanced facility is stress-free. It certainly encourages young and genuine entrepreneurs to obtain financial facilities without a tussle. Most new entrants to the industry struggle to find appropriate collateral to support their credit claim. If they are being supported by a good credit score against their name, obtaining a facility is hassle-free. The credit scoring system endorses the creditworthiness of commendable customers and firms to convince the financial institutions to extend the lending facilities without relying on collaterals.

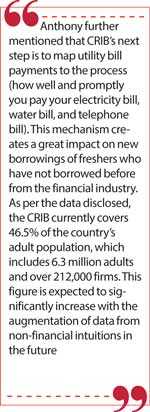

Anthony further mentioned that CRIB’s next step is to map utility bill payments to the process (how well and promptly you pay your electricity bill, water bill, and telephone bill). This mechanism creates a great impact on new borrowings of freshers who have not borrowed before from the financial industry. As per the data disclosed, the CRIB currently covers 46.5% of the country’s adult population, which includes 6.3 million adults and over 212,000 firms. This figure is expected to significantly increase with the augmentation of data from non-financial intuitions in the future.

2 Poor asset quality

In a scenario where the quality of assets are deteriorating, the Individual Credit Score plays a major role where the quality of credit and its volume are concerned. As mentioned in my article dated Wednesday, 13 February1 fraudulent documents and deeds are everywhere in the industry. Hence, the immovable asset quality is questionable at times. Similarly, the movable (vehicle) market is highly volatile. Thus, collateral dependency is not advisable all the time as a fallback option. Similarly, a lengthy litigation process which drags cases over four to five years is not prudent most of the time. It should be the last line of defence and treated as the last recourse. Recovery of the loan through agreed monthly rental is the best option available to settle a financial obligation. Such being the case, repayments are mainly determined by the character of the borrower and not by the face value of the collateral offered or the strength of the documents. Under the circumstances, the customer who believes in ethics, principles and morality has a better edge over others. He is of the view that he has a moral obligation to honour his financial obligations by servicing the monthly rentals on time. This philosophy boosts his credit score under any circumstances.

Conclusion

The CRIB also plans to enhance the accessibility of the CRIB reports and scores by enabling citizens to obtain the CRIB reports and scores online. It would be similar to obtaining a medical report from your medical laboratory in the future. Once in a while, you can check your credit score online. On your own, you can assess whether you are running a healthy credit score or not. You can take necessary  precautions to rectify your situation as you do with your health. Nevertheless, have in mind that bankers and financiers are trained to look suspiciously on those rectified situations even though you have a healthy record afterwards, and be mindful to maintain an unblemished credit record right throughout.It is also understood that retail outlets too will have access to their customers’ credit information to draw their credit limits. These moves make the lending circle of the country much stronger and healthier. The credit score upgrades Sri Lanka’s ranking on the World Bank’s Ease of Doing Business index. It reinforces the lending circle of the country. Non-Performing Advances (NPA) which are rising at an alarming level at present can be curtailed to a large extent by applying credit score to the credit evaluation process.

precautions to rectify your situation as you do with your health. Nevertheless, have in mind that bankers and financiers are trained to look suspiciously on those rectified situations even though you have a healthy record afterwards, and be mindful to maintain an unblemished credit record right throughout.It is also understood that retail outlets too will have access to their customers’ credit information to draw their credit limits. These moves make the lending circle of the country much stronger and healthier. The credit score upgrades Sri Lanka’s ranking on the World Bank’s Ease of Doing Business index. It reinforces the lending circle of the country. Non-Performing Advances (NPA) which are rising at an alarming level at present can be curtailed to a large extent by applying credit score to the credit evaluation process.

This new instrument Individual Credit Score helps curtail the deterioration trend of credit quality in the country and stabilise a healthy lending portfolio by penetrating an unknown territory in the credit evaluation process.

Nevertheless, considering Individual Credit Score in isolation is not advisable under any circumstances as explained before. In an integrated credit evaluation process, the Individual Credit Score can be considered as one of the key elements to decide the limit of credit which could be extended to an individual.

[The writer is the founder of Infornets, an organisation which formed to share credit- related information and financial knowledge to less informed people locally and internationally. He counts 35 years of experience in the non- banking financial industry of Sri Lanka and is a former CEO/General Manager of a Non-Bank Financial Institution. He is a board member of the National Science and Technology Commission (NASTEC), holds a Master Degree in Business Administration from the UK and is a member of the Institute of Management of Sri Lanka. He can be reached via [email protected] or www.infornets.com.]

Footnotes:

1 (http://www.ft.lk/columns/Bank-frauds-and-rising-NPAs--Do-we-have-the-right-people-in-the-financial-industry-/4-672730)