Sunday Apr 19, 2026

Sunday Apr 19, 2026

Monday, 28 November 2016 00:01 - - {{hitsCtrl.values.hits}}

This is part II of a revised version of the paper published in the annual publication of the Association of Professional Bankers or APB under the title ‘Thriving in a Digital World’ in conjunction with its 28th anniversary convention held in Colombo in November 2016.

In part I (available at: http://www.ft.lk/article/581122/Thriving-in-a-Digital-Age--Digital-currencies-pose-the-biggest-challenge-for-banks-%E2%80%93-Part-I ), the onset of the digital age in the financial services industry and its implications were discussed. It was pointed out that embracing digital systems by financial services institutions has helped financial firms to deliver and customers to receive a better and more efficient service.

That part also discussed the development of paper money systems in modern economies and how that system was abused by governments for their own benefits. Hence, there was a demand for the development of alternative currencies in the form of digital currencies or cryptocurrencies by modern nations. One such currency so developed has been the Bitcoin introduced into the financial systems of the world a few years ago.

The Story of Bitcoins

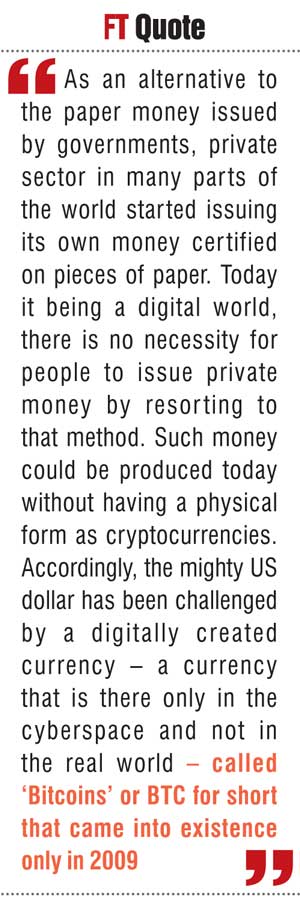

As an alternative to the paper money issued by governments, private sector in many parts of the world started issuing its own money certified on pieces of paper. Today it being a digital world, there is no necessity for people to issue private money by resorting to that method. Such money could be produced today without having a physical form as cryptocurrencies. Accordingly, the mighty US dollar has been challenged by a digitally created currency – a currency that is there only in the cyberspace and not in the real world – called ‘Bitcoins’ or BTC for short that came into existence only in 2009.

The creation of BTC is considered a technological marvel by many because it was the first time a money substitute had been created by using digital apps. A detailed analysis of Bitcoins was presented in a previous article in this series under the title ‘Bitcoins: Can it challenge the mighty dollar?’ (available at: http://www.ft.lk/article/148322/Bitcoins--Can-it-challenge-the-mighty-dollar?).

Pseudonymous Satoshi Nakamoto: Father of Bitcoins

Bitcoins were created by an anonymous developer who took the pseudonym ‘Satoshi Nakamoto’ and has chosen to remain in that way up to date. Therefore, the real people behind Bitcoins are still a mystery.

Bitcoins were created by an anonymous developer who took the pseudonym ‘Satoshi Nakamoto’ and has chosen to remain in that way up to date. Therefore, the real people behind Bitcoins are still a mystery.

Nakamoto expressed his desire to create the new digital currency in a paper he published in a website called listserv in 2008 under the title ‘Bitcoin: A Peer to Peer Electronic Cash System’ without going through a financial institution and without relying on trust to make it acceptable (available at: https://bitcoin.org/bitcoin.pdf). Hence, all the problems involved in real money – the erosion of value due to inflation, frauds in the form of theft, multiple payments and dishonour of obligations and safe and costless delivery – are to be sorted through a foolproof computer program that cannot be changed at will by those who participate in the system.

Digital coins: A chain of digital signatures

This appears to be a pipedream of some weird person but it became a reality within months of his publishing the paper, the first 50 Bitcoins being produced – called being ‘mined’ in Bitcoin terminology – by Nakamoto himself. He has defined in his paper an electronic coin as a chain of digital signatures where each party digitally signs a computer message called an electronic coin and passes it to the next owner so that there is a chain of signatures which can be verified again electronically. In this sense it is like a cheque of which ownership is transferred from person to person by endorsement and delivery showing on the reverse a list of endorsements indicating the passing on of the ownership at every stage.

The difference between a Bitcoin and a cheque is that in the case of a cheque the transfer takes place on trust and there is a bank that guarantees its payment if it is a good cheque. Any dispute can be resolved by resorting to the judicial system which is guided by laws passed by legislatures and case laws established by the judicial systems themselves. There is no such redress in Bitcoins and one has to rely on “the work of proof”, as Nakamoto called it, established by the computer program governing its issue. But the computer program is virtual, anonymous and unreachable in the event of a dispute. This should surely worry the users of Bitcoins.

Zero tolerance of errors

As Nakamoto has argued in his paper several foolproof safety measures with zero tolerance of errors have been incorporated into the computer program. Here, zero tolerance is important because in the case of normal real currencies, there is always room for errors inflicting costs on some and the system’s goal is to maintain such errors at a minimum level.

Safety features of Bitcoins

First, though it is an open source program which can be used by everyone freely, it is based on a difficult cryptographic protocol – a system where security based functions are performed through the use of advanced algorithmic calculations to generate results. Thus, not everyone with a computer can mine Bitcoins but only those with sufficient computational capacity and knowledge.

Second, there is a built in mechanism in the program to make it harder for subsequent participants called miners to mine Bitcoins by gradually reducing the number of coins that could be mined over time. Accordingly, in every four-year period the number they could mine halves and by 2140, the total number of Bitcoins that could have been mined by all is set at its peak level of 21 million. When plotted against time, this is similar to the total utility curve that increases at a decreasing rate or with diminishing marginal utility familiar to students of economics. So, coins cannot be produced at will by miners and there will not be an excess supply that leads to the erosion of its value through inflation like the real currencies of the world. Third, double or multiple payments have been prevented by publicly announcing the chain of ownership change of each Bitcoin so that it is recognised by the system as paid conclusively. So, once an owner has placed his digital signature to a coin, even if he tries to sell it for a second time, the system does not authorise it thereby putting an effective stop to such attempts.

Thus, Bitcoins can pass on from hand to hand indefinitely settling payments in the process without the need for recalling and destroying if they have become unserviceable as in the case of real currencies. Thus, Bitcoins have a virtually zero maintenance and replacement cost.

The details of how Bitcoins are mined and used have been posted to a web portal which can be accessed at www.bitcoin.org. Similar to Wikipedia which provides cyberspace information freely, there is a ‘Bitcoin Wiki’ too that provides information on coins to interested readers.

Mining of Bitcoins

A producer of a Bitcoin is called a miner and anyone with a sufficient computer capacity to crunch through the difficult algorithms set in the program can be a miner by acquiring the open-source software. The system has been set to produce blocks of Bitcoins at intervals of 10 minutes and miners like those prospecting gold can hit the Bitcoins that are being thrown out by the system. Since doing it alone gives only a very slim chance of success because the computer capacity may not be sufficient, many have developed mining pools combining the processing power and sharing the profits among them as previously agreed.

At the beginning, a block contained 50 Bitcoins and as the system has been set, at the production of each set of 21000 Bitcoins, the production is halved; accordingly, today, a block contains only 25 Bitcoins and has become more difficult to mine.

A new user has to acquire a Bitcoin wallet which is simply a computer facility like the email account of a person. He has three  choices to maintain his wallet containing Bitcoins: his mobile phone, his desktop or with a centralised service provider in the cloud. Non-miners can acquire Bitcoins by buying from the market at the prevailing market prices which are variable and subject to fluctuation.

choices to maintain his wallet containing Bitcoins: his mobile phone, his desktop or with a centralised service provider in the cloud. Non-miners can acquire Bitcoins by buying from the market at the prevailing market prices which are variable and subject to fluctuation.

For instance, when the first block of 50 Bitcoins was mined in January 2009, a Bitcoin was prices at 10 US cents. By June 2011, it went up to $ 32 but fell again to $ 7 in January 2012. It recovered to $ 15 again in August same year moving further to $ 49 in March 2013. In early April 2013, it boomed to $ 266 and then crashed to $ 140 by the middle of the month. The value of Bitcoins has increased to $ 600.79 in September 2016, indicating that its value has increased 6,000 times over its original value in 2009.

Thus, there are Bitcoin miners who are decentralised and make profits if they are lucky enough to mine sufficient quantities that are available in the original software package. But, their job is becoming increasingly difficult with a fewer Bitcoins are being thrown out by the system as time passes.

Then, there are others who acquire Bitcoins by paying in real currencies on the exchanges that function again in the cyberspace. Both parties can use Bitcoins for making payments to others who accept them in payment or sell them on the exchange and make capital gains or losses.

Paul Krugman: Mining of Bitcoins is a waste of resources

There are several criticisms against Bitcoins. On economic grounds, Nobel Laureate Paul Krugman has commented in his New York Times regular column that even the use of computer time and energy to mine Bitcoins is a waste of resources because they do not serve any economic purpose like a real currency (available at: http://krugman.blogs.nytimes.com/2013/12/28/bitcoin-is-evil/?_r=0). Krugman has a point here because real currencies facilitate trade and exchange in increasing volumes, provide international liquidity to conclude international transactions, serve as reserve currencies so that nations could maintain their excess wealth in those currencies and help develop financial and capital markets by creating new and smart financial instruments.

Bitcoins are nothing of these. Krugman has even gone to the extent that even Adam Smith about whom he has no particular liking would have scorned Bitcoins because the celebrated economist had as far back as 1776 downgraded both silver and gold currencies on account of the wastage of real resources tied up with money when the same money could have been produced cheaply with paper money.

Bitcoins are not environmentally costless

Some have criticised Bitcoins on the ground of the environmental costs they have inflicted. For instance, Mark Gimein writing to the Bloomberg.com has argued that mining Bitcoins requires huge computing power and the electricity consumed in mining in a single day has been around 982 megawatts hours sufficient to provide power to 31,000 homes a day. Thus, though it is a virtual currency that does not use paper, ink, printing machines, energy, packing and transport materials and storage, it also involves a huge amount of power that has to be produced by emitting greenhouse gases that contribute to global warming.

Though this claim is a little exaggerated as argued by Tim Worstall, a Fellow of the Adam Smith Institute in London, what Mark has tried to present is that creating virtual coins is not totally environmentally friendly as some people have been claiming.

Bitcoins and Ponzi schemes

Then there is the criticism that it resembles the features of a pyramid scheme, better known as Ponzi schemes. A Ponzi scheme is a financial scam where those who first join the scheme stand to gain at the expense of those who join it later. Similarly, those who have first joined the Bitcoin system have mined the coins easily and have acquired the coins relatively at a cheaper price. But since its supply is restricted, the latecomers have to spend more resources to mine coins and have to acquire them at high prices. Their ability to make cash out of their investments depends on whether there are willing buyers of Bitcoins after them. If there are no such buyers, they have to lose the value of their investments whereas the early joiners have already made money and quitted the system.

Invitation to hackers

There is the possibility to lose Bitcoins held by people due to hacking and deliberately infected viruses. It already happened on several occasions in 2011 and 2012 and on one occasion in 2013.

The worst incident in this connection was the hacking of the largest exchange on Bitcoins, namely, Mt Gox in June 2011 by a hacker and reducing the price of Bitcoins from $ 13 a coin to pennies. If the possibility of security breach is high then there is a high risk which the participants have to take. There are numerous instances where the Bitcoin security has been compromised by hackers or thieves.

Financial bubbles in Bitcoins

The most damaging criticism against the Bitcoin system is the possibility of developing financial bubbles and their bursting eventually. Bitcoins have no intrinsic value and are not protected by national economies as in the case of real currencies. Since there is no regulatory authority, there is no one to protect the interests of innocent participants in the event of the bursting of the bubble. In September 2016, Bitcoins priced at $ 600.79 level is a bubble because it has no intrinsic value to push the price to that high level.

The proliferation of blockchain technology

Bitcoins have also introduced other technological innovations which can be used by other digital currency developers as well. One such innovation is the introduction of blockchain technology – a system of public ledger for recording Bitcoin transactions. Each transaction involving a Bitcoin is called a ‘block’ and once the transactions are completed, they are added to a ‘chain’ making it a permanent database of all transactions by using Bitcoins. Thus, a blockchain is similar to the full history of banking transactions; a block is similar to the individual bank statement. However, an issue relating to blockchain is the continuous growth of the chain raising problems of storage and synchronisation.

The blockchain technology will combine three aspects of a financial transaction which banks have been doing at great costs. They are the recording of transactions, establishing identity and establishing contracts. Thus, it is expected to take over from banks the person to person transactions reducing costs and generating efficiencies. With the huge potential it is expected to have, leading ICT developers such as IBM, Infosys and Microsoft have ventured into developing alternative blockchain technology and support those who plan to introduce digital currencies. Since both Bitcoins and blockchain technology are a disruption to traditional financial services industry, it has become necessary for banks to develop measures to get out of the disruption successfully. In the next part, we will discuss how banks could resolve the challenges faced by them by the introduction of digital currencies to financial systems.

(W.A. Wijewardena, a former Deputy Governor of the Central Bank of Sri Lanka, can be reached at [email protected]).