Monday Feb 16, 2026

Monday Feb 16, 2026

Friday, 17 June 2016 00:00 - - {{hitsCtrl.values.hits}}

On 3 June, the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with Sri Lanka.

The Sri Lankan economy has good underlying momentum but is starting to show signs of strain from a combination of an increasingly difficult external environment and challenging policy adjustments. Real GDP growth was 4.8% in 2015 (broadly unchanged from 2014), while headline inflation remains stable in the low single digits.

An increase in recurrent expenditure led to a widening of the fiscal deficit in 2015 (estimated at 6.9% of GDP), and an increase in public debt to 76% of GDP. As of end-2015 there was also an estimated Rs 1.36 trillion (11% of GDP) in additional government and state enterprise liabilities.

Despite an improvement in the terms of trade from low world oil prices, the overall balance of payments deteriorated in 2015. Negative export growth, flat inward remittance flows, and a sharp decline in net capital inflows more than offset robust growth in tourism and the windfall from lower oil and other commodity prices. As a result, gross international reserves declined from 4.3 months of imports in 2014 to 3.8 months in 2015. Financial soundness indicators are generally favourable, with banks’ capital adequacy remaining comfortably above regulatory limits.

Sri Lanka’s prospects for the medium-term appear favourable if current macro-financial imbalances can be addressed. Real GDP is projected to rise to 5% in 2016, supported by a recovery in construction and sustained momentum in services including tourism, transport, and IT.

While the Government seeks to undertake sizeable fiscal consolidation and tackle high priority structural reforms, growth momentum can be sustained with a solid commitment to reform, a clear direction on macroeconomic policies, and restoration of market confidence.

Sri Lanka’s medium-term growth prospects are generally favourable, given its strong base of human and physical capital and strategic position in a fast growing and dynamic region. The key risks to the outlook, both short- and medium-term, stem from Government inaction on key policies and a significant deterioration in the external environment.

To support their economic program over 2016–19, the authorities have requested the IMF’s financial assistance. The program seeks to: (i) implement a structural increase in revenues; (ii) reverse the decline in central bank foreign exchange reserves; (iii) reduce public debt relative to GDP and lower Sri Lanka’s risk of debt distress; (iv) enhance public financial management and improve the operations of state owned enterprises; (v) transition toward flexible inflation targeting with a flexible exchange rate regime; and (vi) promote sustainable and inclusive economic growth by enabling stronger trade and investment. The program will be supported by a three-year Extended Arrangement under the Extended Fund Facility.

Executive Board Assessment

Executive Directors noted that despite positive growth momentum, the Sri Lankan economy is facing challenges due to the difficult external environment and a period of significant political transition. Directors welcomed the authorities’ commitment to strengthen macroeconomic and financial stability by putting public finances on a more sustainable path, rebuilding foreign exchange reserves, and undertaking reforms to foster sustainable and inclusive growth. They emphasised that steadfast implementation of prudent policies under the Fund-supported program will be important to improve market confidence and encourage investment.

Directors welcomed the authorities’ commitment to reduce the fiscal deficit and underscored that well-designed growth-friendly consolidation efforts will be necessary to ensure fiscal and debt sustainability. They emphasised that priority should be given to enhancing revenues through the implementation of new tax legislation, eliminating exemptions, building capacity in revenue administration, and tightening expenditure management. They also highlighted the importance of pushing ahead with state enterprise reform, including expeditious resolution of SriLankan Airlines. Implementation of automatic pricing mechanisms for fuel and electricity prices will also help reduce fiscal risk.

Directors welcomed the current monetary policy stance and agreed that further tightening could be needed depending on credit and inflation developments. They supported the authorities’ plan to shift to an inflation targeting framework over the medium term. Directors underscored that greater exchange rate flexibility and an exit from central bank intervention in the foreign exchange market would help protect and rebuild foreign exchange reserves. They emphasised the need for a coordinated effort with fiscal policy to ensure an orderly adjustment in macroeconomic policies and a reduction in balance of payment pressures to make such an exit possible and build market confidence.

Directors noted that the financial system is well capitalised and liquid. Going forward, they saw need for continued efforts to strengthen financial sector supervision and regulation, including the legal framework for crisis preparedness and resolution. Directors also encouraged the authorities to carefully monitor loans to SOEs and growth in the credit-to-GDP ratio. They welcomed steps being taken to resolve pockets of instability in the nonbank financial sector.

Directors emphasised the importance of structural reforms, especially with respect to trade and investment. They agreed that priority needs to be given to improving competitiveness, attracting foreign direct investment, eliminating barriers to trade and investment, and boosting exports, including through greater integration into regional and global supply chains.

The IMF approved on 3 June a three-year, $1.5 billion loan for Sri Lanka under the Extended Fund Facility (EFF) to support the country’s economic reform agenda.

Sri Lanka has gone through a significant political transition against the backdrop of an increasingly difficult external environment. Two major elections in 2015 brought a new Government to the helm, major constitutional changes (trimming the power of the presidency) and a reorganisation of ministerial agency portfolios. At the same time, surging imports, falling exports, slowing remittances, tepid foreign direct investment, and a steady outward march of capital from Government securities markets gave rise to macroeconomic imbalances.

Real GDP growth was 4.8% in 2015 (broadly unchanged from 2014), thanks to strong growth in services and agriculture, as well as a positive, albeit declining, contribution from manufacturing. Similarly, the negative growth in construction and weaker growth in manufacturing were indicative of a slowdown in public and private investment, as well as the negative effects of slowing world trade.

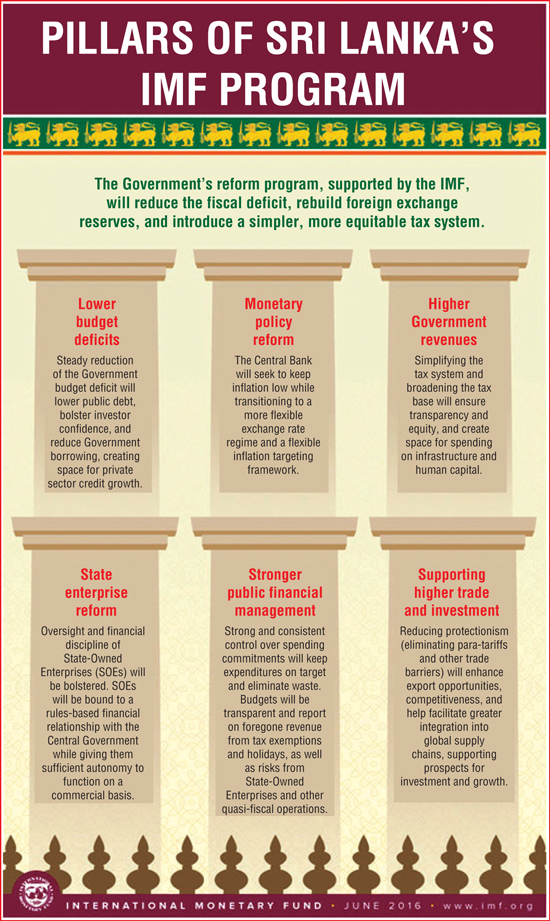

Policies to support adjustment and reform

The Government’s strategy to address short-term imbalances and medium-term challenges rests on six pillars:

Capacity development will be a key element in ensuring a successful reform program. Technical assistance from the IMF will focus on tax policy, revenue administration, public financial management, foreign exchange, capital market, and financial sector oversight, as well as Government financial and economic statistics.

Strong potential

Tapping into Sri Lanka’s considerable potential will require a mix of sound macroeconomic policies—applied consistently over time—together with efforts to boost economic resilience and move toward greater integration with regional and global markets.

Sri Lanka’s economic potential is considerable. The country has a strong base of human capital and reliable infrastructure. It also occupies a strategic position in Asia, the fastest growing region in the world, and investments over the last decade (particularly in ports and other transport-related facilities) can take advantage of this opportunity.

Some features of a new economic landscape for Sri Lanka at the end of the medium-term program would be:

Support from development partners

The IMF’s assistance also serves as a catalyst to mobilise additional support from other bilateral and multilateral institutions. Sri Lanka expects some $650 million in new development and policy loans from such institutions as the World Bank, the Asian Development Bank, the Japan International Cooperation Agency, and others over the next three years, along with a steady pipeline of technical assistance in key reform areas.