Tuesday Mar 17, 2026

Tuesday Mar 17, 2026

Wednesday, 3 June 2015 00:05 - - {{hitsCtrl.values.hits}}

CSE Head of Listing and Corporate Affairs Priyana Gunesekera, CSE Chief Operating Officer Renuka Wijayawardhana, Moderator Daily FT Editor Nisthar Cassim, SLAASMB Director General Gamini Wijesinghe, Tokyo Cement Chairman Dr. Harsha Cabral and BDO Partners Partner Technical and Human Capital Tishan Subasinghe at the head table

By Radhi de Silva

A seminar was organised by BDO Partners, Chartered Accountants, based on the title ‘Demystifying the Complexity of Related Party Transactions,’ and a panel discussion was held to allow the participants to raise their questions to the panellists with regard to RPT.

The panellist consisted of eminent persons who are well conversant in relation to RPT such as Dr. Harsha Cabral, President’s Counsel and Chairman of Tokyo Cement PLC; Gamini Wijesinghe, Director General of Sri Lanka Accounting and Auditing Standards Monitoring Board (SLAASMB) and former Senior Commissioner of Department of Inland Revenue; Renuka Wijayawardhana, Chief Operating Officer of the Colombo Stock Exchange (CSE); Tishan Subasinghe, Partner Technical and Human Capital – BDO Partners; and Priyana Gunesekera, Head of Listings and Corporate Affairs of the CSE. The panel discussion was moderated by Daily FT Editor Nisthar Cassim.

the Colombo Stock Exchange (CSE); Tishan Subasinghe, Partner Technical and Human Capital – BDO Partners; and Priyana Gunesekera, Head of Listings and Corporate Affairs of the CSE. The panel discussion was moderated by Daily FT Editor Nisthar Cassim.

A practical viewpoint

Dr. Cabral expressed his opinion with regard to the Companies Act and the Code of Best Practices on Related Party Transactions (RPT) from a practical viewpoint. He pointed out that mechanisms like the interests register have been in place for a very long time to deal with RPT. He emphasised that the directors’ duties in relation to RPT must be read together with the general obligations of directors given in section 184, 186, 187, 188 and 189 of the Companies Act, where they must act in the best interests of the company. It was also mentioned that it is not only a company law requirement but an ethical obligation that the directors do not place themselves in situations where there can be a conflict of interests.

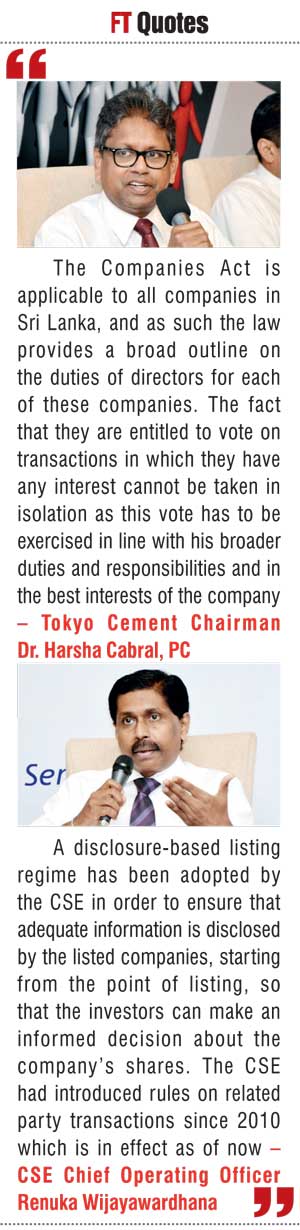

Dr. Cabral was of the opinion that the Companies Act is applicable to all companies in Sri Lanka, and as such the law provides a broad outline on the duties of directors for each of these companies. The fact that they are entitled to vote on transactions in which they have any interest cannot be taken in isolation as this vote has to be exercised in line with his broader duties and responsibilities and in the best interests of the company.

When appointed as a director of a listed company, it was mentioned by Dr. Cabral that the regulators impose a higher standard of care on the directors in order to protect the investor interests. The introduction of the Code of Best Practices on RPT and even the Code of Best Practices on Corporate Governance are examples of where the Securities and Exchange Commission (SEC) has placed more stringent requirements and put in place a regulatory framework on listed companies to ensure greater transparency and accountability of its affairs.

Difficulties in capturing RPT

As a member the Board of Directors of several listed companies Dr. Cabral also discussed the role of the RPT Review Committee which has to be set us under the Code of Best Practices on RPT. This committee is charged with the responsibility to review all RPT of the company.

He explained the difficulties in capturing RPT as one director may also be a director of another company with which the company has business dealings but such transactions may escape the notice of the director inadvertently. Dr. Cabral suggested that companies will have to invest on software which is capable of connecting the directors’ interests in transactions by entering the NIC number of the director to such computer system. There is however, a doubt as to whether such system can also be programmed to capture RPT with parties outside the country as well.

There was a request from the audience to the representatives from the CSE to consider the possibility of making such a software freely available to the public in order to ensure ease of compliance with the new regulatory requirements.

Disclosure-based listing regime

Renuke Wijayawardhane informed that a disclosure-based listing regime has been adopted by the CSE in order to ensure that adequate information is disclosed by the listed companies, starting from the point of listing, so that the investors can make an informed decision about the company’s shares.

The CSE had introduced rules on related party transactions since 2010 which is in effect as of now. There are certain disclosures required by way of immediate disclosures as well as in the annual reports. However it was subsequently felt th at the present rules were not broad enough and certain rules did not provide clarity too. For e.g., at times it was difficult for companies to define what a related party transaction was. A frequent question was having common directors would constitute a RPT.

at the present rules were not broad enough and certain rules did not provide clarity too. For e.g., at times it was difficult for companies to define what a related party transaction was. A frequent question was having common directors would constitute a RPT.

Sometimes related party relationships and transactions may be difficult to identify and report by the company. Sometimes it may have been noted that the company’s related parties may operate via an extensive and complex network of relationships due to the convoluted shareholding structures of the company which makes it difficult to unravel the RPT.

Wijayawardhane accepted that there was some confusion regarding what is a ‘recurrent’ RPT and several companies wanted to know if they needed to disclose each recurrent transaction separately or whether to disclose the cumulative amounts. The CSE subsequently issued a clarification that companies can in fact group ‘recurrent’ transactions in the ordinary course of business and disclose an estimated amount. However, the ‘non-recurrent’ transactions will have to be disclosed as and when they take place.

At times the CSE has noted that the disclosures did not specify the terms of the transaction; whether it in the ordinary course of business, concessionary rates would apply etc. Also, the rationale for the transaction was also not given, although required in the rules.

However, with the introduction of the new rules, which would be mandatory from next year, most of these confusions would arise. The new rules would ensure that there a transparent process established by the listed companies to review the related party transactions with adequate checks and balances together with certain enhanced disclosure.

Wijayawardhane expressed that certain parties may wonder as to why the CSE requires so much information but it was explained that once a company gets listed the company acquires a responsible role as the public will be investing in that company and if discrepancies in information are not avoided the public will be reluctant to invest in the company or may start discounting the true value of the company and the company’s cost of capital will increase

It was inquired as to what steps are taken by the CSE in the event of noticing any lacuna in the regulations and Wijayawardhane informed that CSE will duly inform the SEC and the SEC will take remedial action and also in the event of any irregular activities by parties, the SEC will be informed with regard to same by the CSE and the SEC will take necessary legal action against such parties.

Transfer pricing regulation

Wijesinghe, speaking through experience whilst being the Director General of SLAASMB and former Senior Commissioner of Department of Inland Revenue, addressing the attendees informed that there is no applicable threshold for transfer pricing regulation under Section 104 of the Inland Revenue Act. The threshold of Rs. 50 million and 100 million for domestic transaction and international transaction respectively are applicable only for the purpose of keep and maintain of relevant information which is required under regulation 5 of Transfer Pricing Gazette No. 1823/5 dated 12 August 2013.

It was also informed that RPT are liable to test under arm’s length price. But if both related parties are local, then if either party is not enjoying tax holiday, concessi on rate or loss incurred for the purpose of tax the section 104 is not applicable. This condition is not applicable if one party is in different jurisdiction.

on rate or loss incurred for the purpose of tax the section 104 is not applicable. This condition is not applicable if one party is in different jurisdiction.

The rate of interest to be charged for the related party was also mentioned as a controversial area in RPT. The general idea of the arm’s length pricing is the price which is charged by independent party in uncontrolled condition, in other words, the open market price for the same or similar product or services under similar condition. It was also mentioned that as far as interests are concerned, identification of similar conditions are difficult. Therefore cost of capital plus relevant profit margin may be the reasonable rate to be charged and the relevant interest rate to be adjusted considering the risk factors of the borrower.

Wijesinghe informed that transfer pricing is applicable for any transaction or group of transactions of class of transactions. He further explained that transfer pricing regime now have been established in Sri Lanka, therefore such to be complied with in relation to RPT.

It was further explained that Section 104 defines what arm’s length price means: “a price which is applied in uncontrolled conditions in a transaction between persons, other than associated undertakings”. This section is implied that the price on transactions which is take place between related parties to be treated always as non-arm’s length. Therefore if there are any transactions between related parties they have to ready to prove that there prices are arm’s length.

Accounting and auditing standards

SLAASMB is the only authorised regulator for issuing and monitoring of accounting and auditing standards in Sri Lanka, and the SLAASMB Board has given authority to The Institute of Chartered Accountants of Sri Lanka to issue relevant accounting and auditing standards. While regulating the process of issuing standards, the board annually review around 1,500 annual reports and 100 cases of audit to satisfy the application of the relevant standards.

Sri Lanka Accounting Standards (LKAS) 24 is the standard expressing the disclosure of RPT. The Board has noted that 163 entities including 54 SMEs have failed to provide information relating to the nature of the related party relationships as well as information about transactions with related parties. Wijesinghe further stated that any persons who fails to comply with provisions shall be liable to a fine.

Priyana Gunesekera informed that currently there are two sets of rules applicable for RPT namely the rules that came into effect in September 2010 and the rules that came into effect from 1 January 2014 which are currently on a voluntary basis and would become mandatory with effect from 1 January 2016.

It was also informed that based on the sample of annual reports reviewed by CSE none of those listed companies have adopted the new rules and continue to make disclosures based on the rules introduced in September 2010 which are currently mandatory.

During the review process by CSE, it has been noted that when complying with the 2010 RPT Rules, the listed companies have issues in tracking down related parties and having them in a system in a retrievable manner, and even though market announcements are made by certain companies the announcements do not contain the required disclosures, e.g. the rationale, the terms whether in the ordinary course of business or on special terms at concessionary rates, etc.

It was mentioned that the requirement under the applicable rules is to make an initial announcement on an estimated basis of recurrent RPT initially and thereafter make an announcement when the actual aggregate exceeds 5% of the estimate.

The new rules that are currently adoptable on a voluntary basis do not require immediate disclosure of recurrent transactions and whether non-recurrent RPT is to be disclosed per transaction or on a cumulative basis. The requirement is for each transaction to be disclosed if it exceeds the threshold and thereafter all material transactions, prior to the concerned parties being informed by a third party.

CSE also have identified certain RPT from the annual reports which have not been duly disclosed as per rules and non-disclosure of RPT separately for each related party.

Challenges under the new rules

Gunesekera explained that some of the challenges to be faced under the new rules for example are prior to the board approving the RPT to obtain shareholder approval when required in a well-planned manner when entering into RPT and, the RPT Review Committee having to review the transaction prior to or before completion of a transaction since transactions entered into for which approval will be obtained before completion of a transaction may pose issues if not accepted and having to track down related parties of the entity prior to six months of a transaction, which can be a very challenging task.

It was also mentioned that when a company does not inform the CSE regarding a RPT that requires immediate disclosure, the CSE could be made aware via a complaint or a media release. The other method would be at the time of reviewing the annual report of the company, where the CSE would identify certain RPT based on annual report information, which however may very well happen within five to eight months after the year end.

In such instances the CSE would include the observation in the observations letter and compel the company to comply with the rules and require the company to make an immediate disclosure. In a worst case scenario the CSE may take certain action in line with those provided in the listing rules.

The panel was raised with the question as to what would the role of the auditor be with regard to the rules and how effective would they be in complying with the rules.

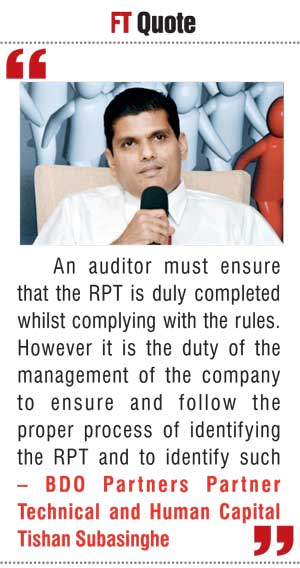

Subasinghe informed that an auditor must ensure that the RPT is duly completed whilst complying with the rules. However it is the duty of the management of the company to ensure and follow the proper process of identifying the RPT and to identify such.

It was further informed that the management may use specific software to capture such or an independent audit committee to ensure that the rules are fulfilled but the management to ensure that the right people are selected to the committee. Furthermore, the Sri Lanka Auditing Standards (SLAuS) 250 ‘Consideration of Laws and Regulations in an Audit of Financial Statements’. The auditor has to ensure compliance with any laws or regulations which would have a material impact on financial statements. This includes any laws and regulations on Related Party Transactions. And also as per the SLAuS 550 ‘Related Parties,’ the auditor has to ensure proper audit procedures been carried out in covering Related Party Transaction.

Furthermore, the auditor has to ensure compliance with LKAS 24, the according standard on ‘Related Party Disclosures,’ which has mainly focused on making adequate disclosures on Related Party Transactions.

When asked what steps have been taken by the Department of Inland Revenue regarding the new rules, the invitees from the Department of Inland Revenue informed that the department is ready to follow the new rules and the department intends to organise workshops to train the department officials in order to be prepared to handle transfer pricing issues.

Role of directors

It was suggested to the panel that the directors are not aware of the rules with regard to RPT, and Dr. Cabral informed that as per the Companies Act there are no specific requirements to be a director but it is the duty of the shareholders of the company to appoint those who are suitable to be in the board especially independent director as they are required to bring in a wealth of knowledge, and proper training to be provided to the directors to carry out their duties.

Dr. Cabral further added that the Golden Key Credit Company would not have collapsed if proper disclosures too place and directors were provided with training and followed their duties accordingly.

When inquired from the Department of Inland Revenue whether irregular RPT are detected, Wijesinghe informed that they have detected and losses of revenue to the Government has been reduced because of the detections. The department has also taken steps to gazette information regarding transfer pricing and the requirement of disclosure has been emphasised.

Pix by Upul Abayasekara

BDO experts share insights

Prior to the panel discussion, the BDO seminar featured an expert presentation by its senior executives. |